If you own a free standing home in Booie, QLD 4610, you're likely wondering whether you're paying a fair price for home and contents insurance — or leaving money on the table. This article breaks down a real insurance quote for a 3-bedroom, 1-bathroom weatherboard home in Booie, compares it against local, state, and national benchmarks, and highlights the property features that are likely driving the premium up or down.

---

Is This Quote Fair?

The annual premium for this quote comes in at $1,452 per year (or $137/month), covering both building (sum insured: $491,000) and contents ($50,000), each with a $2,000 excess.

Our price rating for this quote is CHEAP — below average — and the numbers back that up convincingly.

The suburb average for Booie sits at $2,638/year, meaning this quote is roughly 45% cheaper than what most homeowners in the area are paying. Even compared to the suburb's 25th percentile — the cheapest end of the local market — this quote at $1,452 undercuts the $1,819 mark. In other words, this is among the most competitive premiums available for this postcode.

At the state level, the picture is even more striking. The Queensland average for home insurance is $4,547/year, more than three times this quote. Queensland is one of the most expensive states in the country for home insurance, largely driven by cyclone-prone coastal regions and flood-risk areas in the north and south-east. This Booie property benefits from being in a non-cyclone risk zone, which is a significant factor.

By national standards, the average premium is $2,965/year — still more than double this quote. Any way you slice it, $1,452 is a genuinely competitive result for a home and contents policy in regional Queensland.

---

How Booie Compares

Here's a quick snapshot of how this quote stacks up across different benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,452 |

| Booie Suburb Average | $2,638 |

| Booie Suburb Median | $2,734 |

| Booie 25th Percentile | $1,819 |

| Booie 75th Percentile | $3,187 |

| South Burnett LGA Average | $3,467 |

| QLD State Average | $4,547 |

| National Average | $2,965 |

| National Median | $2,716 |

It's worth noting that the suburb sample size for Booie is relatively small (10 quotes), so averages can shift as more data comes in. That said, the consistent gap between this quote and every comparison point tells a clear story — this is a well-priced policy.

The South Burnett LGA average of $3,467 is particularly interesting. Booie sits within South Burnett, yet this quote comes in at less than half the LGA average, suggesting that property-specific characteristics are playing a meaningful role in keeping the premium low.

---

Property Features That Affect Your Premium

Several features of this property work in its favour — and a couple introduce modest risk factors worth understanding.

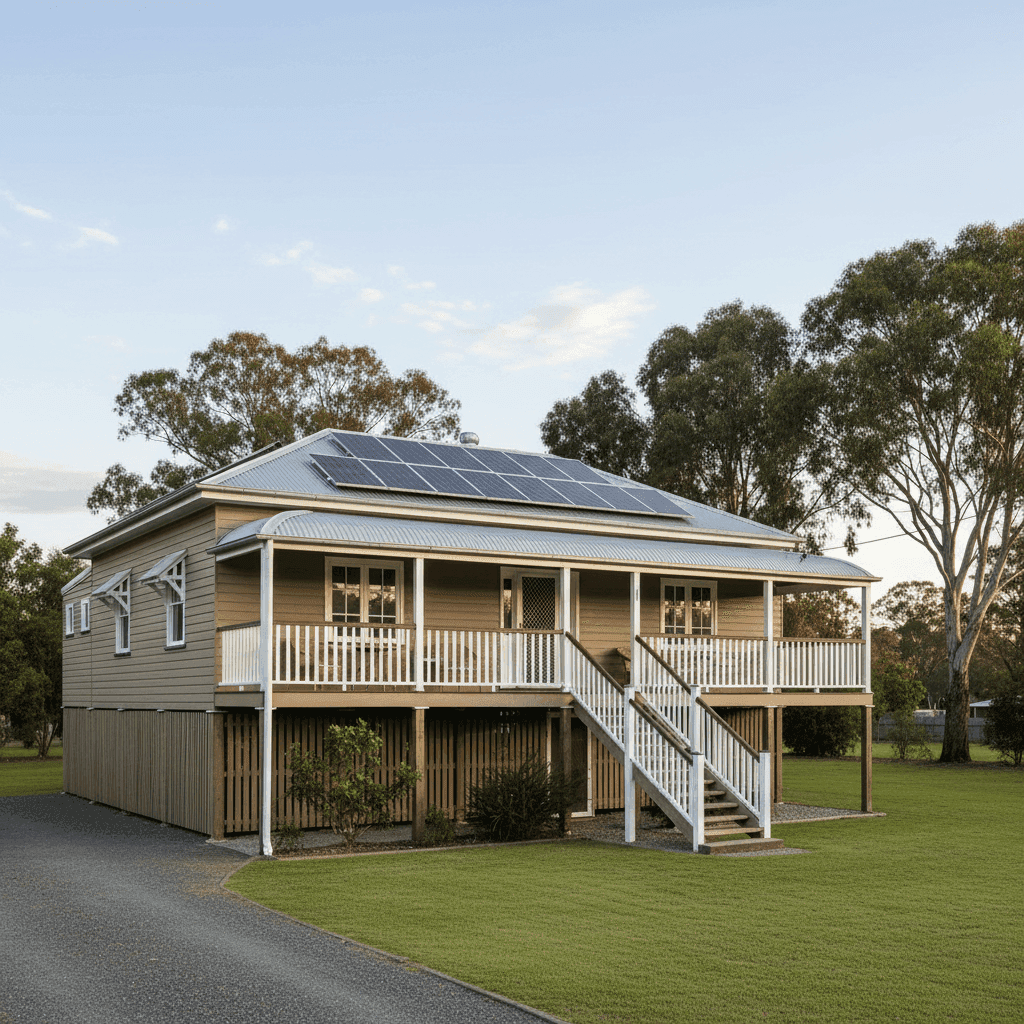

Weatherboard Timber Walls

Weatherboard construction is common in older Queensland homes and is generally considered a moderate-risk material by insurers. Timber can be more susceptible to fire and pest damage compared to brick veneer or double brick, which can nudge premiums upward. However, a well-maintained weatherboard home in a low-risk area can still attract competitive pricing.

Steel / Colorbond Roof

Colorbond roofing is viewed favourably by insurers. It's durable, low-maintenance, and performs well in storms — a major consideration in Queensland. This roof type is likely contributing positively to the premium outcome.

Elevated on Stumps (At Least 1m)

This is arguably the most premium-friendly feature of this property. Being elevated by at least one metre on stumps — classic Queenslander style — significantly reduces flood and inundation risk. In a region where heavy rainfall events are not uncommon, this construction style can make a substantial difference to what insurers charge.

Timber / Laminate Flooring

Flooring type can influence contents and building replacement costs. Timber and laminate are mid-range in terms of replacement value, consistent with the standard fittings quality noted for this property.

Solar Panels

The property has solar panels installed, which adds a small amount to the insured building value and can slightly increase premiums. However, the impact is generally modest for a standard residential system.

No Pool, No Ducted Climate Control

The absence of a pool removes a liability and maintenance risk factor that insurers price in. Similarly, no ducted climate control system means fewer complex mechanical components to cover — both contribute to a cleaner, lower-risk risk profile.

Construction Year: 1994

At around 30 years old, this home is mature but not ancient. Homes from this era are generally well-understood by insurers — old enough to have settled, but not so old as to raise significant concerns about outdated wiring or plumbing (assuming standard maintenance).

---

Tips for Homeowners in Booie

Whether you're reviewing your current policy or shopping for the first time, here are some practical steps to make sure you're getting the best value.

- Review your sum insured regularly. Building costs in regional Queensland have risen sharply in recent years. Make sure your $491,000 building sum insured reflects current construction costs — not what it cost to build in 1994. Underinsurance is one of the most common and costly mistakes homeowners make.

- Don't over-insure your contents. A $50,000 contents value is reasonable for a 3-bedroom home with standard fittings, but it's worth doing a proper home inventory every year or two. Overestimating contents means you're paying for cover you don't need; underestimating means you could be left short after a claim.

- Maintain your home's elevated foundation. The stumped foundation is a genuine asset when it comes to flood and moisture risk. Keep the subfloor well-ventilated, check for termite activity regularly, and ensure the stumps are in good condition — this protects both your home and your insurability.

- Compare quotes at renewal time. Even if you're happy with your current insurer, premiums can shift significantly year to year. With Booie suburb premiums ranging from $1,819 at the 25th percentile all the way to $3,187 at the 75th percentile, there's clearly a wide spread in the market. Shopping around at renewal is one of the simplest ways to avoid paying more than you need to.

---

Compare Your Home Insurance Quote Today

Whether you're a Booie local or buying in the South Burnett region, it pays to know what the market looks like before you commit to a policy. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can see exactly where your premium sits relative to your neighbours.

Get a quote at CoverClub and find out if you're paying a fair price — or if there's a better deal waiting for you.