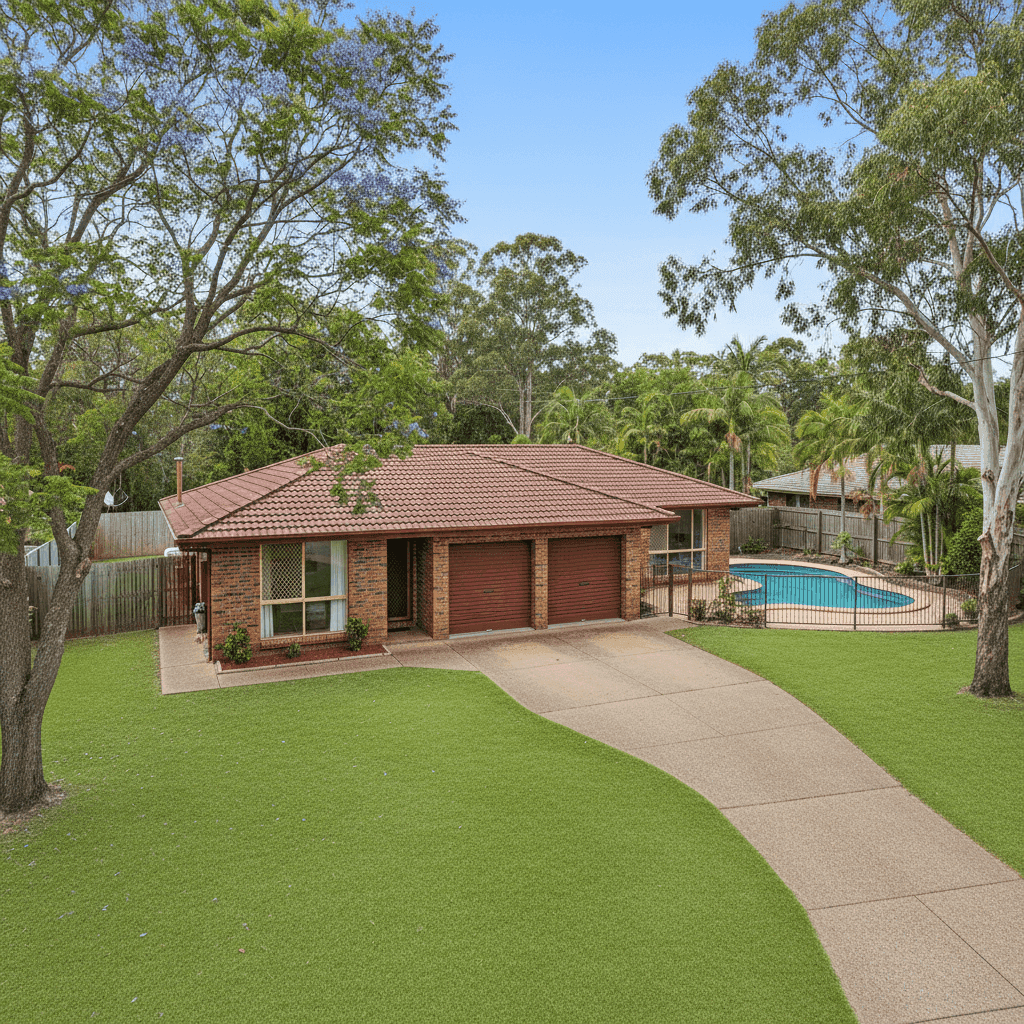

If you own a free standing home in Boondall, QLD 4034, you're probably curious about whether you're paying a fair price for home and contents insurance. This article breaks down a real quote for a four-bedroom, two-bathroom brick veneer home in the suburb, comparing it against local, state, and national benchmarks so you can make a more informed decision at renewal time.

---

Is This Quote Fair?

The quote in question comes in at $1,605 per year (or roughly $157 per month) for combined home and contents cover, with a building sum insured of $300,000 and contents valued at $30,000. Both the building and contents excess are set at $500.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up when you look at the numbers. The suburb average premium for Boondall sits at $1,670 per year, meaning this quote is actually sitting a touch below the local average — a modest but welcome saving of about $65 annually. It's nudging above the suburb median of $1,490, which tells us that while it's not the cheapest deal on the market, it's comfortably within the normal range for this area.

In short: you're not overpaying, but there's likely room to do better if you shop around.

---

How Boondall Compares

To put this quote in proper context, it helps to zoom out and look at the broader insurance landscape. Here's how Boondall stacks up:

| Benchmark | Premium |

|---|---|

| This Quote | $1,605/yr |

| Boondall Suburb Average | $1,670/yr |

| Boondall Suburb Median | $1,490/yr |

| Brisbane LGA Average | $16,277/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

The contrast with Queensland's state average is striking. At $9,129 per year, the QLD average is more than five times the cost of this Boondall quote — a reflection of the enormous variability across the state, driven largely by high-risk areas in Far North Queensland where cyclone and flood exposure pushes premiums sky-high.

Similarly, the Brisbane LGA average of $16,277 may look alarming at first glance, but this figure is heavily skewed by premium properties in flood-prone or high-value suburbs across Greater Brisbane. Boondall, sitting in the northern suburbs, benefits from comparatively lower risk exposure.

Even against the national average of $5,347, this quote looks very reasonable. Australia-wide, insurers are pricing in significant natural hazard risk — from cyclones in the north to bushfires in the south and east. Boondall's position keeps it out of the most expensive risk tiers.

You can explore more local data on the Boondall suburb stats page, or compare against the broader QLD insurance landscape and national averages.

> Note: The suburb comparison is based on a sample of 12 quotes, so averages should be treated as indicative rather than definitive.

---

Property Features That Affect Your Premium

Every property has a unique risk profile, and insurers assess a range of characteristics when calculating your premium. Here's how the features of this particular home come into play:

Brick Veneer Walls Brick veneer is generally well-regarded by insurers. It offers solid fire resistance and durability compared to timber or weatherboard construction, which can translate into lower premiums. It's a common and well-understood building type, so insurers can price it with confidence.

Tiled Roof Terracotta or concrete tile roofs are considered a low-to-moderate risk by most insurers. They're durable, fire-resistant, and less susceptible to wind damage than corrugated iron in many scenarios. However, tiles can crack or dislodge in severe storms, so it's worth ensuring your policy covers storm damage adequately.

Slab Foundation A concrete slab foundation is a neutral-to-positive factor for insurers. It reduces the risk of subsidence and pest-related structural damage compared to older pier-and-beam or suspended timber floors.

Swimming Pool Having a pool on the property adds a layer of liability and can nudge premiums upward slightly. Pools also represent an insurable asset in their own right — damage from storms, ground movement, or mechanical failure can be costly to repair.

Ducted Climate Control Ducted air conditioning is a significant fixed asset. If the system is damaged by a storm, electrical surge, or fire, replacement costs can run into the tens of thousands. Ensuring your building sum insured adequately accounts for this is important.

Construction Year: 1991 A home built in 1991 is over 30 years old. While it's not ancient, it may have ageing plumbing, electrical wiring, or roofing components that could increase the likelihood of a claim. Some insurers apply age-related loading; others don't — so it's worth comparing policies carefully.

Building Size: 214 sqm At 214 square metres, this is a comfortably sized family home. The building sum insured of $300,000 equates to roughly $1,402 per square metre — a figure that's worth double-checking against current construction costs in Brisbane, which have risen sharply in recent years.

---

Tips for Homeowners in Boondall

1. Review Your Sum Insured Annually Construction costs in South East Queensland have surged since 2020. If your building sum insured hasn't kept pace, you could find yourself underinsured in the event of a total loss. Use a building cost calculator or speak with a quantity surveyor to validate your coverage amount.

2. Don't Overlook Contents Cover $30,000 in contents cover is relatively modest for a four-bedroom home. Take the time to do a proper contents inventory — furniture, appliances, electronics, clothing, and valuables can add up quickly. Underinsuring your contents is one of the most common mistakes homeowners make.

3. Ask About Pool and System Discounts Some insurers offer discounts or more competitive pricing if your pool has compliant fencing and safety features. Similarly, if your ducted system is regularly serviced, it may reduce the likelihood of a mechanical breakdown claim — worth mentioning when comparing quotes.

4. Compare at Renewal, Every Time The insurance market moves constantly. A policy that was competitive two years ago may no longer be the best deal today. Use a comparison platform like CoverClub to benchmark your renewal quote before you accept it — it takes minutes and could save you hundreds.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for cover for the first time, comparing quotes is the single most effective way to make sure you're getting value. Get a home insurance quote at CoverClub and see how your premium stacks up against the market — no obligation, no hassle.