Booval is a well-established suburb in the City of Ipswich, sitting about 40 kilometres west of the Brisbane CBD. It's a predominantly residential area with a mix of older character homes and more recent renovations — exactly the kind of neighbourhood where understanding your home insurance costs can make a real difference to your household budget. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free-standing home in Booval, and puts that number into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $1,526 per year (or roughly $154 per month), covering both building (sum insured: $568,000) and contents ($50,000). Our price rating for this quote is CHEAP — below average — which is genuinely good news for the homeowner.

To put that in perspective: the average home insurance premium across Queensland sits at a staggering $9,129 per year, with a state median of $3,903. Nationally, the average is $5,347, with a median of $2,764. This quote comes in well beneath every one of those benchmarks, suggesting the homeowner is getting solid value for their cover.

It's worth noting that Queensland is one of the most expensive states in Australia for home insurance, largely due to flood exposure, cyclone risk in northern regions, and a higher frequency of severe weather events. The fact that this Booval property is sitting so far below the state average is a meaningful result — though it's always worth reviewing what's actually covered before assuming cheaper means better.

You can explore broader Queensland insurance trends at the QLD state stats page, or compare against national averages here.

---

How Booval Compares

While suburb-level data isn't available for Booval (postcode 4304) at this stage, the broader Ipswich LGA context is telling. The average premium across the Ipswich LGA is $8,901 per year — almost six times higher than this particular quote. That's a significant gap, and it reflects the wide variance in risk profiles across the LGA, which includes flood-prone areas along the Bremer and Brisbane rivers.

Here's a quick snapshot of how this quote stacks up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,526 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

| Ipswich LGA Average | $8,901 |

The takeaway is clear: at $1,526, this is a genuinely competitive result. Whether that reflects the specific insurer's pricing model, the property's characteristics, or a combination of both, it's well worth benchmarking against other providers to ensure the cover itself is comprehensive.

Check out the Booval suburb stats page for more localised data as it becomes available.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium — some favourably, others less so. Here's what stands out:

Construction Era and Materials

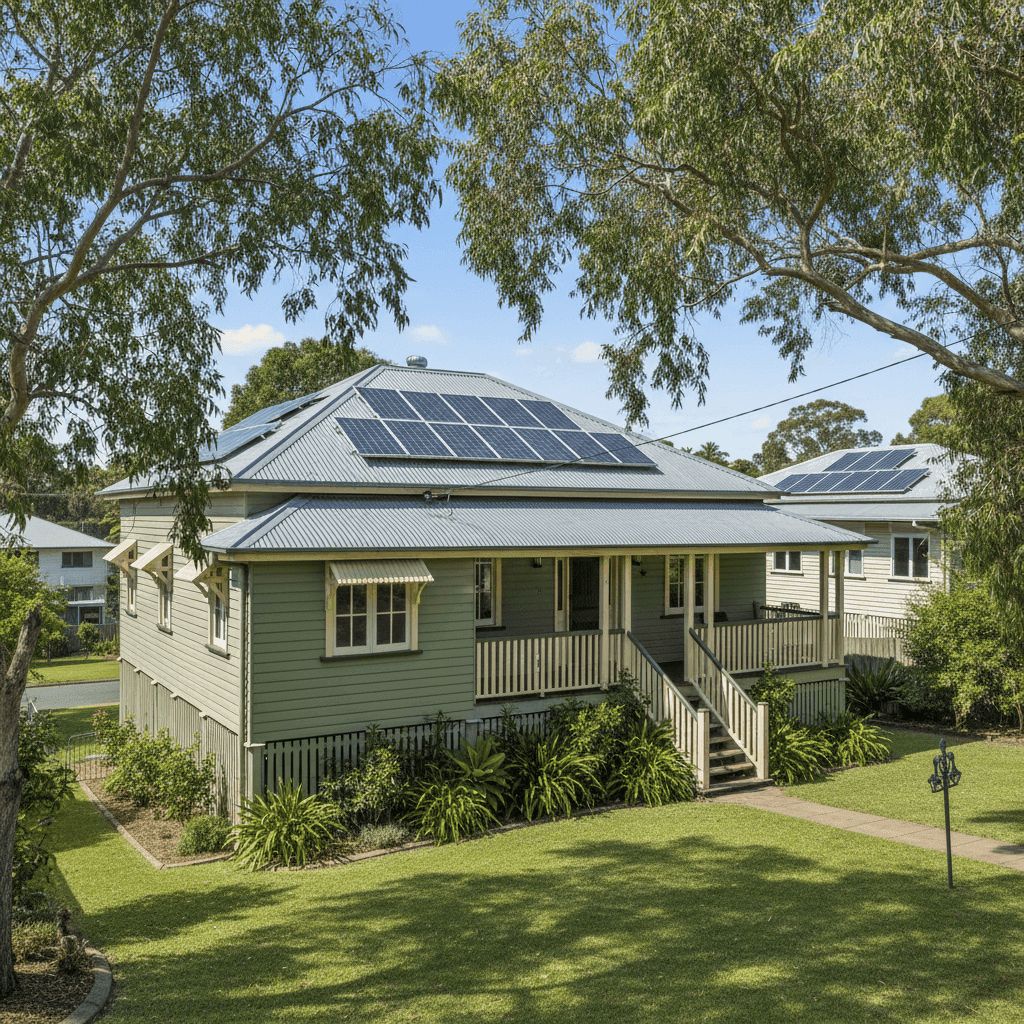

Built in 1960, this is an older home, which can cut both ways with insurers. On one hand, older properties may have ageing plumbing, wiring, or structural elements that increase risk. On the other, a well-maintained home of this era can be perfectly sound. The weatherboard timber exterior walls are a notable factor — timber is more susceptible to fire and rot than brick veneer or double brick, which can push premiums higher with some insurers.

Roof Type

The steel/Colorbond roof is a positive from an insurance perspective. Colorbond is durable, lightweight, and performs well in high-wind and hail events compared to older tile roofs. It's a common upgrade on homes of this age and is generally viewed favourably by underwriters.

Foundation

The property sits on stumps, which is typical for Queensland homes of this era. Stump foundations allow airflow beneath the house (important in Queensland's climate) and can make repairs more accessible. However, they can also be a risk factor in flood-prone areas, as floodwater can more easily affect the subfloor structure.

Solar Panels

The presence of solar panels adds a layer of complexity to insurance. Panels represent a significant asset that should be covered under the building sum insured. It's important to confirm with your insurer that solar panels are explicitly included in your policy — not all standard policies cover them as a default.

No Pool, No Ducted Climate Control

The absence of a pool removes one common liability risk, and no ducted climate control system means fewer mechanical components that could fail or cause damage. Both factors can contribute to a cleaner risk profile.

Flooring

Timber and laminate flooring throughout is worth noting for contents claims — water damage can be particularly costly with these materials, so ensuring your contents and building cover adequately addresses water-related events is important.

---

Tips for Homeowners in Booval

1. Check Your Flood Cover Carefully Ipswich has a well-documented history of flooding, particularly along the Bremer River corridor. Even if your specific street hasn't flooded, it's critical to confirm whether your policy includes flood cover — and to understand how your insurer defines "flood" versus "storm surge" or "rainwater runoff." These distinctions matter enormously at claim time.

2. Review Your Building Sum Insured Annually Construction costs in Queensland have risen sharply in recent years. A sum insured of $568,000 for a 214 sqm home may be appropriate today, but it's worth recalculating your rebuild cost each year. Underinsurance is one of the most common — and costly — mistakes homeowners make.

3. Confirm Solar Panel Coverage As mentioned above, solar panels should be explicitly covered under your building policy. Ask your insurer directly: are the panels, inverter, and mounting hardware included in the sum insured? If not, you may need to adjust your coverage or seek an endorsement.

4. Compare Quotes Before Renewal The insurance market in Queensland is competitive, and premiums can vary enormously between providers for the same property. Don't simply auto-renew — use a comparison tool to benchmark your renewal quote against the market each year. Even a policy rated "cheap" today may not be the best value next year.

---

Ready to Compare Home Insurance in Booval?

Whether you're a first-time buyer or a long-time Booval resident, getting the right home and contents cover at the right price takes a bit of research. CoverClub makes it easy to compare quotes from multiple insurers in one place, so you can see exactly where your premium sits relative to the market.

Get a home insurance quote for your Booval property today and find out if you're paying a fair price — or if there's a better deal waiting for you.