If you own a free standing home in Bossley Park, NSW 2176, you're probably curious about what a fair home insurance premium looks like — and whether you're overpaying or getting a genuine bargain. This article breaks down a real home and contents insurance quote for a four-bedroom brick veneer property in the suburb, comparing it against local, state, and national benchmarks so you can make a truly informed decision.

---

Is This Quote Fair?

The short answer: yes — and then some.

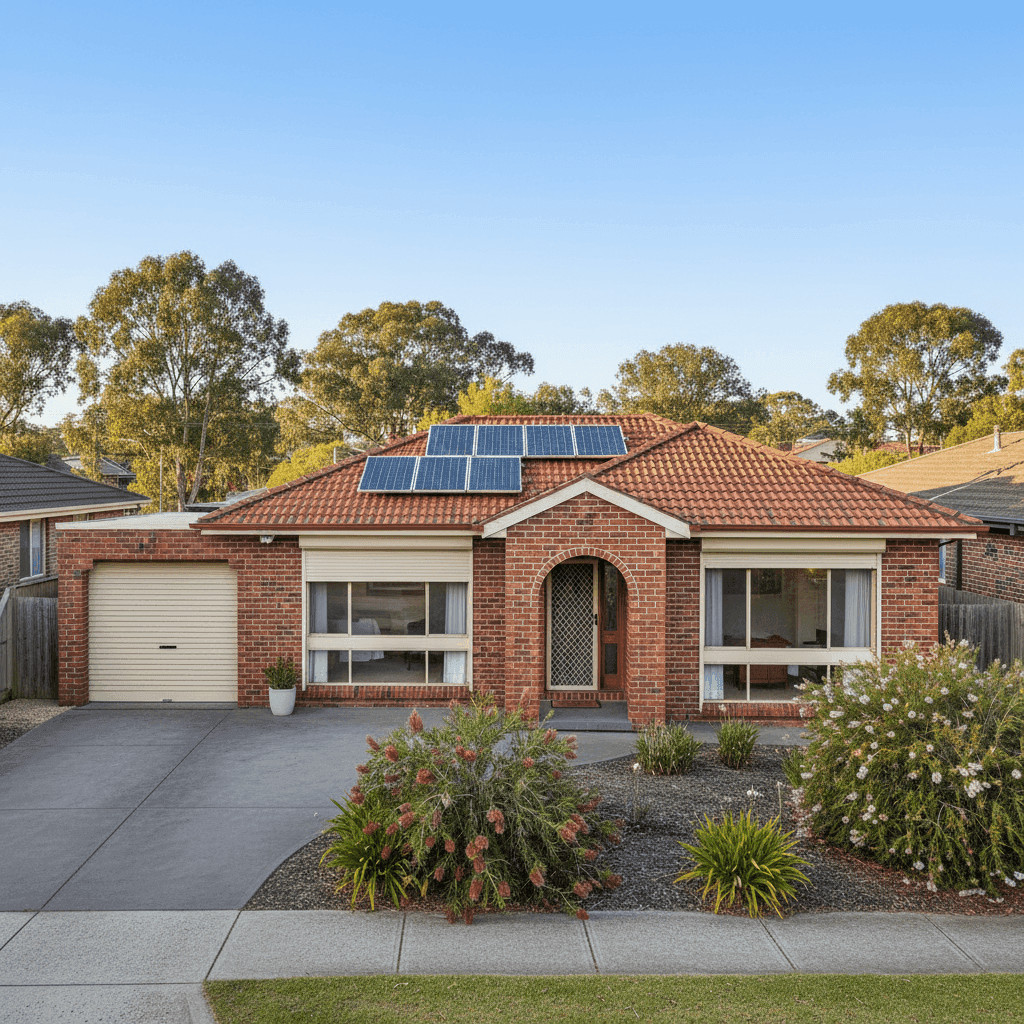

This quote came in at $1,320 per year (or around $131 per month) for combined home and contents cover, with a building sum insured of $651,000 and contents valued at $50,000. Our price rating for this quote is CHEAP, meaning it sits meaningfully below the average for the area.

To put that in perspective, the suburb average premium in Bossley Park is $4,572 per year, and the median sits at $2,154 per year. Even the 25th percentile — representing the cheaper end of quotes in the suburb — comes in at $1,711 per year. This quote undercuts even that figure, landing it firmly in below-average territory in the best possible way.

For a homeowner covering a 214 sqm property with a solid building sum insured and a reasonable contents value, this represents excellent value. That said, it's worth noting the building excess is set at $3,000 — higher than typical — which is likely one of the levers bringing the annual premium down. The contents excess of $500 is more standard.

---

How Bossley Park Compares

Understanding where Bossley Park sits relative to broader benchmarks helps frame just how competitive this quote is. Here's a snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Bossley Park (suburb) | $4,572/yr | $2,154/yr |

| Fairfield LGA | $3,071/yr | — |

| NSW (state) | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. Bossley Park's suburb average of $4,572 is notably higher than both the NSW state average ($3,801) and the national average ($2,965), suggesting that insurers price this area with some caution — possibly due to localised risk factors such as storm exposure or claims history in the postcode. You can explore the full breakdown of Bossley Park insurance statistics on CoverClub.

By comparison, the NSW state average of $3,801 per year reflects a wide range of properties across the state, from coastal flood zones to inland rural areas. The national average of $2,965 per year is lower still, partly because it includes lower-risk regions that pull the figure down.

Against all of these benchmarks, the $1,320 quote analysed here is a standout result — roughly 71% below the suburb average and 55% below the national average.

It's worth noting that this analysis is based on a sample of 16 quotes in the suburb, so results can vary. Premiums depend heavily on individual property characteristics, insurer appetite, and the specific cover options selected.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour when it comes to pricing:

Brick veneer construction is generally well-regarded by insurers. It offers solid weather resistance and performs reasonably well in fire scenarios compared to timber-framed or clad exteriors. Combined with a tiled roof, this home presents a lower-risk profile than properties with metal roofing or older fibrous cement cladding.

Slab foundation is the standard for many Sydney suburban homes built in the 1980s, and insurers typically view it as stable and low-risk — particularly in areas without significant subsidence or expansive clay soil concerns.

The 1984 construction year is worth a mention. Homes of this era are mature enough that some components (roofing, plumbing, electrical) may be approaching the end of their serviceable life, which can occasionally nudge premiums slightly higher. However, a well-maintained home of this age shouldn't attract significant loading.

The presence of solar panels is increasingly common in suburban Sydney and is generally factored into the building sum insured. It's important to ensure your policy explicitly covers solar panels as part of the building, as some policies treat them differently.

The timber and laminate flooring throughout the home is a contents-adjacent consideration — if flooring is fixed and integral to the structure, it's typically covered under building insurance. However, it's worth confirming with your insurer how they classify your specific flooring type.

With no pool and no ducted climate control, two common sources of additional premium loading are absent here, keeping costs lean.

---

Tips for Homeowners in Bossley Park

1. Review your building sum insured regularly. At $651,000, this home's building sum insured reflects the cost to rebuild — not the market value. Construction costs have risen sharply in recent years, so it's worth reassessing this figure annually to avoid being underinsured. Use a building cost calculator or speak with a quantity surveyor if you're unsure.

2. Understand your excess trade-off. The $3,000 building excess on this policy is on the higher side. While it helps reduce your annual premium, it means you'll need to cover a larger portion of any claim out of pocket. Make sure you have that buffer available, and consider whether a lower excess (at a slightly higher premium) might suit your financial situation better.

3. Confirm solar panel coverage. With solar panels installed, double-check that your policy covers them for damage caused by storms, hail, or electrical faults. Some insurers include them automatically under building cover; others require you to list them separately or may apply sub-limits.

4. Compare quotes at renewal — every year. Even a great premium today doesn't guarantee competitive pricing next year. Insurers adjust their rates based on claims data, reinsurance costs, and risk modelling. Running a fresh comparison at renewal is one of the simplest ways to ensure you're not gradually drifting into overpriced territory. The Bossley Park suburb average of $4,572 is a reminder of how wide the spread can be.

---

Ready to Compare Your Own Quote?

Whether you're a Bossley Park local or just researching home insurance options across greater Sydney, CoverClub makes it easy to see how your current premium stacks up. Get a home insurance quote today and find out if you're paying a fair price — or if there's a better deal waiting for you.