Boyne Island, nestled along the coast of Central Queensland near Gladstone, is a sought-after suburb for families and retirees alike — and like much of regional Queensland, home insurance here can vary dramatically depending on your property. This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom free-standing home in Boyne Island (QLD 4680), and puts it in context against local, state, and national benchmarks so you know exactly where you stand.

---

Is This Quote Fair?

The short answer: yes — and then some. This quote came in at $1,572 per year (or $159/month) for combined home and contents cover, with a building sum insured of $511,000 and contents valued at $26,000. Our pricing engine rates this as CHEAP — below the suburb average — which is a strong result for any homeowner in this part of Queensland.

To put it bluntly, a premium under $1,600 per year for a brick veneer home in Boyne Island is genuinely competitive. The building excess sits at $4,000, which is on the higher side and is likely one of the levers helping keep the annual premium low. The contents excess of $500 is fairly standard. If you're comfortable with a larger out-of-pocket cost in the event of a major building claim, this trade-off makes solid financial sense — especially if you're claim-free year after year.

---

How Boyne Island Compares

The numbers tell a compelling story. Based on 56 quotes collected for the Boyne Island area, the pricing landscape looks like this:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,572 |

| Suburb 25th Percentile | $3,273 |

| Suburb Median | $4,691 |

| Suburb Average | $5,215 |

| Suburb 75th Percentile | $7,344 |

| QLD State Average | $4,547 |

| QLD State Median | $3,931 |

| National Average | $2,965 |

| National Median | $2,716 |

This quote sits well below even the national median of $2,716 — which is remarkable given that Queensland properties typically attract higher premiums than the national average due to elevated weather and flood risks. At $1,572, this homeowner is paying less than half the suburb median, and roughly one-third of what the most expensive quartile of Boyne Island properties are paying.

You can explore Queensland-wide insurance pricing data and national home insurance benchmarks to see how other regions compare.

---

Property Features That Affect Your Premium

Several characteristics of this particular property work in the homeowner's favour when it comes to insurance pricing:

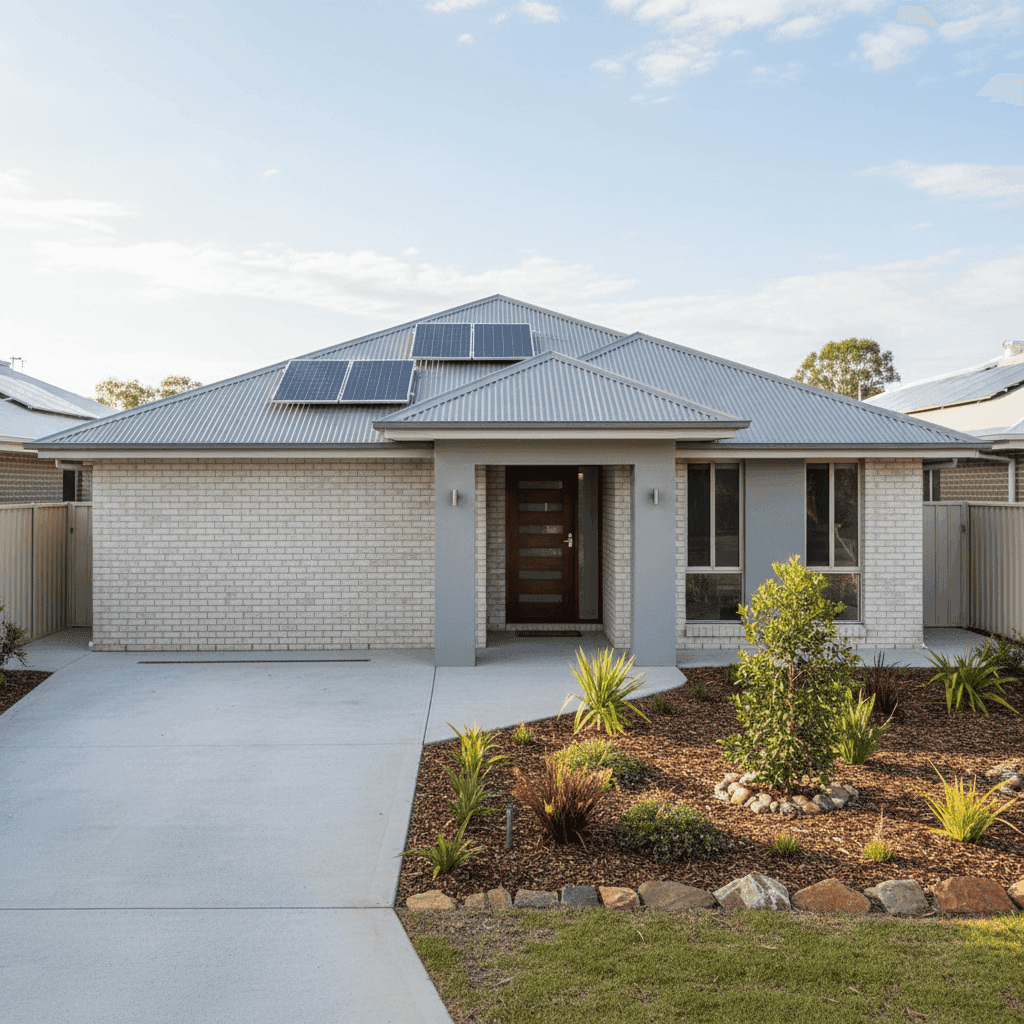

Brick Veneer Walls & Colorbond Roof

Brick veneer is generally viewed favourably by insurers — it's durable, fire-resistant, and holds up well structurally. Paired with a steel Colorbond roof, this combination is considered low-maintenance and resilient. Colorbond roofing in particular is highly regarded in Queensland for its ability to handle heat, UV exposure, and moderate weather events.

Slab Foundation

A concrete slab foundation reduces the risk of subsidence and pest-related structural damage compared to older timber stumps or pier-and-beam constructions. Insurers typically view slab homes as lower risk, which can contribute to more competitive premiums.

Timber & Laminate Flooring

While timber and laminate floors can be more susceptible to water damage than tiles, they're generally straightforward to repair or replace. Contents cover for flooring is often included under building policies, so it's worth confirming exactly what's covered under this policy.

Solar Panels

This property has solar panels installed, which adds some value to the insured asset. It's worth confirming with the insurer that the solar system is explicitly included in the building sum insured of $511,000, as some policies treat solar panels as a separate item or exclude them by default.

No Pool, No Ducted Climate Control

The absence of a swimming pool removes a common liability concern for insurers. No ducted climate control also means fewer complex mechanical systems that could fail or cause water damage — both factors that can quietly reduce your risk profile.

Not in a Cyclone Risk Zone

This is significant. Much of coastal and far-north Queensland attracts cyclone-specific loading on insurance premiums, which can push annual costs into the thousands. Boyne Island's classification as outside a designated cyclone risk area is a meaningful advantage for homeowners here.

---

Tips for Homeowners in Boyne Island

Even with a competitive quote in hand, there are always ways to protect your coverage and manage costs over time.

1. Review your building sum insured regularly. Construction costs across Queensland have risen sharply in recent years. A sum insured of $511,000 for a 139 sqm home built in 2000 may be appropriate today, but it's worth reassessing annually — ideally using a quantity surveyor's estimate or your insurer's rebuild calculator — to avoid being underinsured when it matters most.

2. Confirm solar panels are covered. Ask your insurer directly: are the solar panels included in the building sum insured, and are they covered for storm damage, power surge, and accidental breakage? Some standard policies have gaps here that can catch homeowners off guard.

3. Reconsider your contents value. $26,000 in contents cover is on the lower end for a 3-bedroom, 2-bathroom home. Take the time to do a room-by-room contents inventory — furniture, appliances, electronics, clothing, tools, and outdoor items all add up quickly. Being underinsured on contents is one of the most common mistakes Australian homeowners make.

4. Shop the market at renewal time. A below-average premium today doesn't guarantee the same result next year. Insurers adjust their pricing models frequently, and loyalty doesn't always pay. Set a reminder to compare quotes at renewal — even a 15-minute comparison could save you hundreds.

---

Ready to Compare?

Whether you're a Boyne Island local or researching insurance for a property purchase, CoverClub makes it easy to benchmark your premium against real data. Get a home insurance quote today and see how your property stacks up against suburb, state, and national averages — all in one place.