If you own a free standing home in Bridgeman Downs, QLD 4035, you've probably wondered whether your home insurance premium is competitive — or whether you're quietly paying more than you need to. This article breaks down a real home and contents insurance quote for a five-bedroom property in the suburb, and benchmarks it against local, state, and national data to give you a clearer picture of where you stand.

---

Is This Quote Fair?

The quote in question comes to $3,208 per year (or around $307 per month) for combined home and contents cover, with a building sum insured of $1,050,000 and contents valued at $370,500. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as Fair — Around Average.

That assessment holds up when you look at the numbers in context. The suburb average for Bridgeman Downs sits at $2,948/yr, with a median of $2,811/yr. This quote lands above both of those figures, but it's well within the upper half of the local range — the 75th percentile for the suburb is $3,540/yr, meaning roughly a quarter of comparable quotes come in even higher.

In other words, this isn't a bargain-basement premium, but it's also far from the most expensive outcome for a property of this type in the area. Given the size of the home (235 sqm, five bedrooms, three bathrooms), the relatively high building sum insured, and the inclusion of features like solar panels and ducted climate control, a premium in this range is broadly reasonable.

---

How Bridgeman Downs Compares

To put this quote into proper perspective, it helps to zoom out and look at how Bridgeman Downs insurance costs stack up against broader benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Bridgeman Downs (suburb) | $2,948/yr | $2,811/yr |

| Brisbane LGA | $16,277/yr avg | — |

| Queensland (state) | $9,129/yr avg | $3,903/yr |

| National | $5,347/yr avg | $2,764/yr |

A few things stand out here. The Queensland state average of $9,129/yr looks alarming at first glance, but that figure is heavily skewed by high-risk coastal and cyclone-prone postcodes in Far North Queensland, where premiums can be extraordinary. The state median of $3,903/yr is a far more representative figure for most Queensland homeowners — and this quote sits comfortably below it.

Similarly, the national average of $5,347/yr is pulled upward by extreme premiums in disaster-prone regions. The national median of $2,764/yr is actually slightly below this quote, which again reflects that this is a solidly mid-range outcome rather than an outlier in either direction.

The Brisbane LGA average of $16,277/yr deserves special mention — it's an extraordinary number that reflects the enormous diversity of properties and risk profiles across Greater Brisbane, from flood-prone lowlands to elevated suburban streets. Bridgeman Downs, sitting on higher ground in the city's north, benefits from a more favourable risk profile than many parts of the LGA.

Based on a sample of 59 quotes in the 4035 postcode, this quote sits between the suburb's 25th percentile ($2,118/yr) and 75th percentile ($3,540/yr) — placing it squarely in the middle of the pack for the local market.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Understanding them can help you make sense of your premium — and identify where there may be room to negotiate.

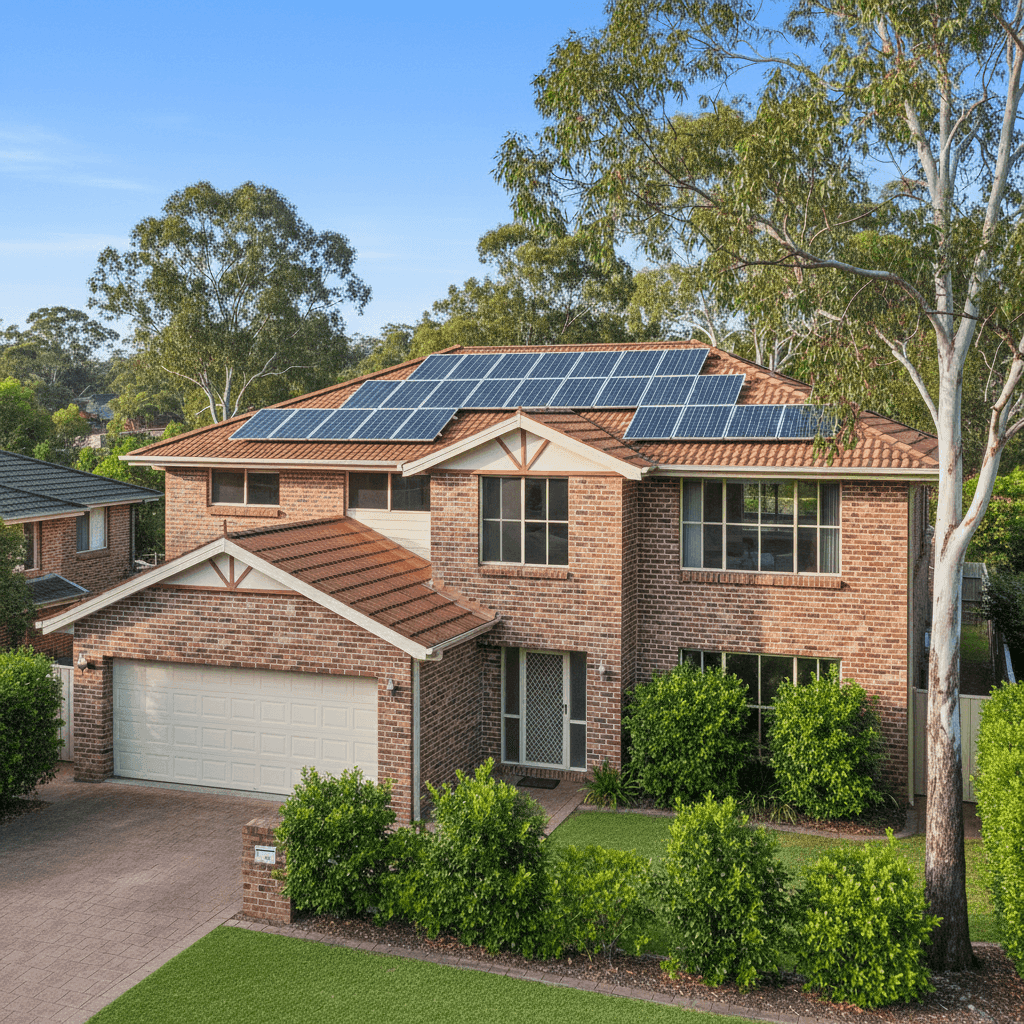

Construction era and materials Built in 1970, this home is over 50 years old. Older properties can attract slightly higher premiums because ageing infrastructure — plumbing, wiring, roofing — carries a greater likelihood of claims. That said, brick veneer construction is viewed favourably by most insurers. It's durable, fire-resistant, and holds up well over time compared to timber or clad alternatives.

Tiled roof Terracotta or concrete tile roofs are generally well-regarded by insurers for their longevity and weather resistance. Unlike metal roofing, tiles can crack under significant hail impact, but they perform well in most Queensland weather conditions outside of cyclone zones — which this property is not in, a meaningful advantage.

Slab foundation A concrete slab is a stable foundation type that tends to be assessed neutrally by insurers. It eliminates some of the subsidence and pest-related risks associated with suspended timber floors.

Solar panels Solar panels add replacement value to the property and can increase the building sum insured. Insurers treat them as a fixed building fixture, so they're typically covered under the building policy — but it's worth confirming this with your insurer and ensuring your sum insured accounts for their current replacement cost.

Ducted climate control Like solar panels, ducted air conditioning systems are a significant fixed asset. They contribute to the overall replacement cost of the home and are one reason a higher building sum insured may be appropriate for a property like this.

High building sum insured At $1,050,000, the building sum insured is substantial — and rightly so for a 235 sqm, five-bedroom home with quality inclusions. Underinsuring to save on premiums is a false economy; if you need to rebuild, a shortfall in cover can be financially devastating.

---

Tips for Homeowners in Bridgeman Downs

1. Review your sum insured regularly Construction costs have risen sharply in recent years. The cost to rebuild your home today may be significantly higher than it was even two or three years ago. Use a building cost calculator or speak with a quantity surveyor to make sure your sum insured reflects current rebuild costs — not what you paid for the property.

2. Check what's included for solar panels Not all policies automatically cover solar panels under the building component, and coverage limits can vary. Confirm with your insurer that your system is fully covered, including inverters and mounting hardware, and that the sum insured accounts for replacement at today's prices.

3. Consider your excess strategically Both the building and contents excess on this policy are set at $1,000. Increasing your excess can meaningfully reduce your annual premium — but only do this if you're confident you could comfortably cover that amount out of pocket in the event of a claim. A higher excess on contents cover in particular can yield good savings.

4. Compare quotes at renewal time Insurance loyalty rarely pays off. Insurers often offer their best rates to new customers, meaning long-standing policyholders can quietly drift into overpaying. Even if your current premium feels reasonable, it's worth running a comparison at each renewal to see what else is available for your specific property profile.

---

Ready to Compare?

Whether this quote is your current premium or one you've received recently, it's always worth seeing what else the market has to offer. CoverClub makes it easy to compare home and contents insurance options for your specific property in Bridgeman Downs. Get a quote today and find out whether you could be paying less — or whether you're already in good shape.