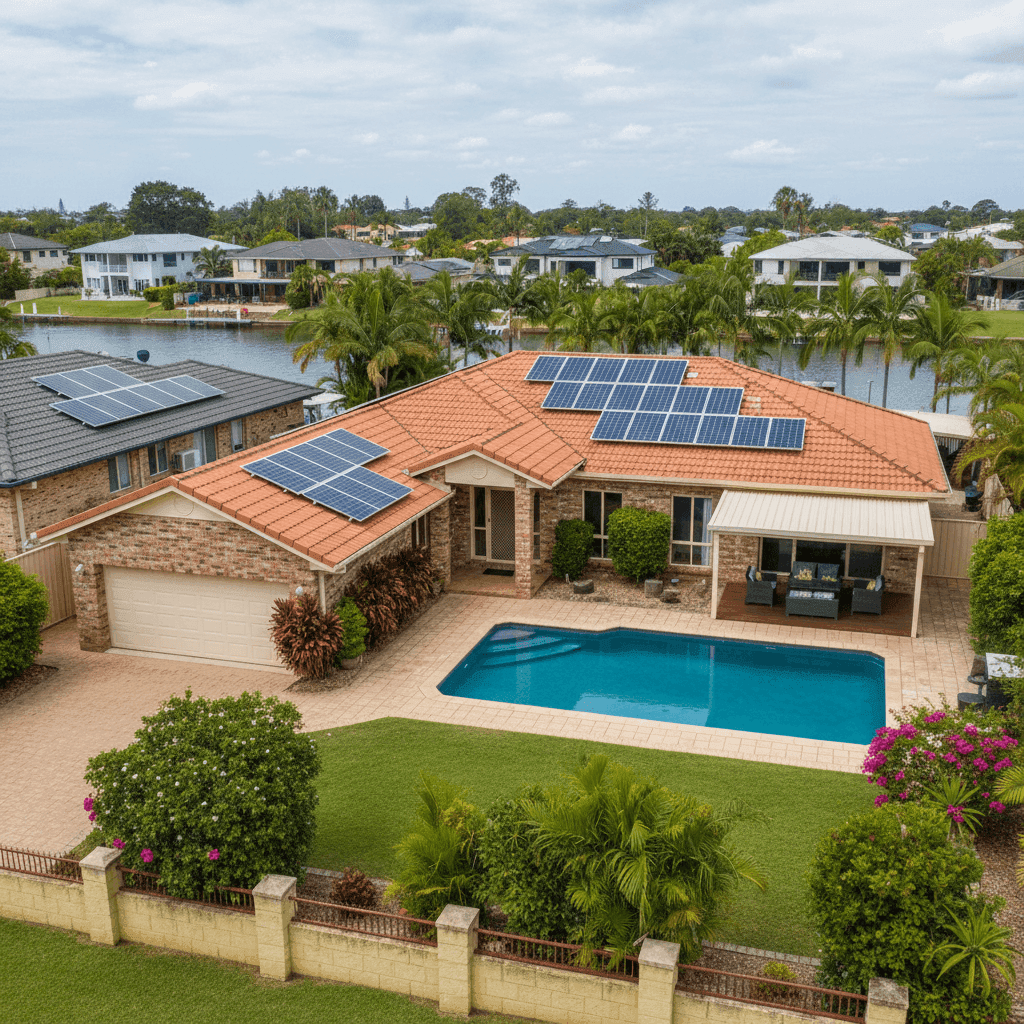

Broadbeach Waters is one of the Gold Coast's most sought-after residential pockets — a leafy canal-side suburb that blends suburban comfort with waterfront lifestyle. For owners of free standing homes here, protecting that investment with the right insurance cover is essential. This article breaks down a real home and contents insurance quote for a four-bedroom property in Broadbeach Waters (QLD 4218), comparing it against local, state, and national benchmarks to help you understand what you're paying — and why.

---

Is This Quote Fair?

The quote in question comes in at $11,239 per year (or $1,124/month) for combined home and contents cover, with a building sum insured of $1,500,000 and contents valued at $90,000. The building excess is set at $2,000 and the contents excess at $1,000.

Our price rating for this quote is EXPENSIVE — above average for the suburb.

To put that in context: the average home and contents premium in Broadbeach Waters sits at $8,167 per year, with a median of $7,098. This quote lands above the 75th percentile threshold of $10,819, meaning it's pricier than at least three-quarters of comparable quotes we've seen in the area (based on a sample of 267 quotes).

That said, "expensive" doesn't automatically mean "wrong." A $1,500,000 building sum insured is on the higher end, and the property includes several features — a pool, solar panels, and ducted climate control — that meaningfully increase replacement costs and, by extension, the premium. If the sum insured accurately reflects what it would cost to rebuild the home from scratch, the higher premium may well be justified.

---

How Broadbeach Waters Compares

When you zoom out beyond the suburb, the premium gap becomes even more pronounced. Here's how this quote stacks up across different geographic benchmarks:

| Benchmark | Average Premium |

|---|---|

| Broadbeach Waters (4218) | $8,167/yr |

| Gold Coast LGA | $5,494/yr |

| Queensland (QLD) | $4,547/yr |

| National Average | $2,965/yr |

Even the suburb average of $8,167 is nearly double the Queensland state average of $4,547, and almost triple the national average of $2,965. This reflects a well-known reality: insuring property on the Gold Coast — and in South East Queensland more broadly — carries a premium loading that homeowners in other parts of Australia simply don't face to the same degree.

Flood risk, storm surge, severe weather events, and high property values all contribute to elevated premiums across the region. You can explore the full breakdown of Broadbeach Waters insurance statistics, compare them against Queensland-wide data, or see how the state sits relative to national averages.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the quoted premium. Understanding them can help you assess whether the price is reasonable — or whether there's room to adjust.

Building Size & Sum Insured

At 214 sqm, this is a well-sized family home. The building sum insured of $1,500,000 is notably high — even for a four-bedroom property with three bathrooms. While it's critical to be adequately insured, it's worth periodically reviewing your sum insured against current rebuild cost estimates. Over-insuring can quietly inflate your premium year after year.

Construction: Brick Veneer & Tiled Roof

Brick veneer walls and a tiled roof are generally viewed favourably by insurers. Both materials offer solid fire resistance and durability, which can help moderate premiums compared to, say, weatherboard cladding or corrugated iron roofing. The concrete slab foundation is similarly low-risk from an insurer's perspective.

Pool

A swimming pool adds both value and liability to a property. Insurers factor in the cost of pool repairs or replacement following storm or structural damage, and in some policies, public liability considerations also come into play. Pools are a common feature on the Gold Coast, but they do nudge premiums upward.

Solar Panels

Solar panels are an increasingly common addition to Queensland homes, but they're not cheap to replace. A full rooftop system can cost $10,000–$20,000 or more, and that replacement cost needs to be reflected in your sum insured. Make sure your policy explicitly covers solar panels — not all do by default.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset in any home. Like solar panels, it needs to be captured within your building sum insured, as it's considered part of the structure rather than a contents item. Its inclusion here is another contributor to the higher-than-average sum insured.

Flooring: Tiles Throughout

Tiled flooring is practical in Queensland's climate and is generally more resilient to moisture damage than carpet or timber. From an insurance standpoint, tiles are a relatively low-risk flooring choice — though full replacement after a major event can still be costly.

---

Tips for Homeowners in Broadbeach Waters

1. Review your sum insured annually Building costs in South East Queensland have risen sharply in recent years due to labour shortages and material price increases. An outdated sum insured could leave you underinsured — but an inflated one means you're paying more premium than necessary. Use a qualified quantity surveyor or an online rebuild cost calculator to keep your figure accurate.

2. Check what's covered for your pool and solar system Not all home insurance policies automatically include pools and solar panels under the building cover. Read your Product Disclosure Statement (PDS) carefully, or ask your insurer directly. If these assets aren't explicitly covered, you could face a nasty gap at claim time.

3. Compare quotes before renewal Loyalty doesn't always pay in the insurance market. Insurers frequently offer better rates to new customers than they do on automatic renewals. Before your policy renews each year, take 10 minutes to compare quotes on CoverClub — the savings can be significant.

4. Consider your excess settings The building excess on this policy is $2,000 and the contents excess is $1,000. Opting for a higher voluntary excess is one of the most straightforward ways to reduce your annual premium. If you're financially comfortable absorbing a larger out-of-pocket cost at claim time, this trade-off can make good sense.

---

Find a Better Deal on CoverClub

Whether you're renewing an existing policy or shopping for cover on a new purchase, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see what multiple insurers would charge for your specific property — in minutes, not hours. Get a home insurance quote today and find out if you can do better than the market average in Broadbeach Waters.