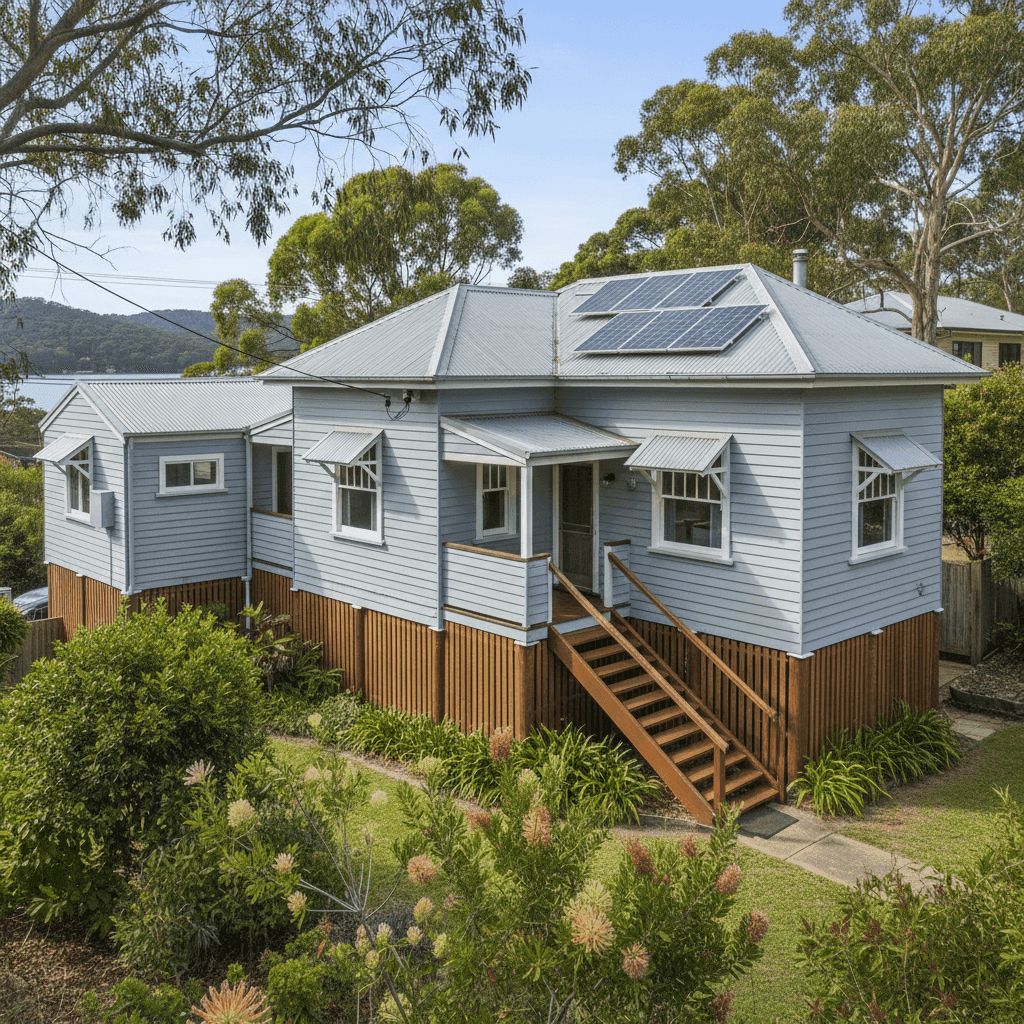

Brooklyn, nestled along the Hawkesbury River in NSW's 2083 postcode, is a scenic and somewhat remote riverside community — and its unique character comes with equally unique insurance considerations. This article breaks down a real home and contents insurance quote for a two-bedroom, two-bathroom free-standing weatherboard home in the area, and examines whether the price stacks up against what other homeowners are paying locally, across NSW, and nationally.

---

Is This Quote Fair?

The annual premium for this property came in at $26,138 per year (or $2,505/month), covering a building sum insured of $600,000 and contents valued at $165,000, each with a $1,000 excess.

Our price rating for this quote is Expensive — Above Average, and the numbers back that up clearly.

The suburb average for Brooklyn sits at just $6,064 per year, with a median of $5,366. That means this quote is more than four times the local median — a significant gap that warrants a closer look. Even the 75th percentile for the suburb (meaning 75% of quotes are cheaper) is only $7,159/year, so this premium is well above what most Brooklyn homeowners are paying.

That said, context matters. The building sum insured here is $600,000, which may be higher than what comparable properties in the suburb are insured for. A higher replacement value will naturally drive up premiums. Still, even accounting for that, the gap is substantial and suggests this homeowner should absolutely shop around.

---

How Brooklyn Compares

To understand where this quote sits in the broader market, here's a quick snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Brooklyn (NSW 2083) | $6,064/yr | $5,366/yr |

| LGA – Central Coast (NSW) | $8,387/yr | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Brooklyn's suburb average of $6,064 is actually below both the NSW state average and the LGA average, suggesting that on the whole, Brooklyn is a reasonably affordable area to insure — at least compared to the broader Central Coast region and NSW overall. You can explore the full NSW insurance data here and national benchmarks here.

Second, the large gap between NSW's average ($9,528) and its median ($3,770) signals that a relatively small number of very expensive quotes are pulling the average up significantly — a pattern common in states with diverse geography, from flood plains to bushfire-prone regions.

For Brooklyn specifically, the sample size of 15 quotes is relatively small, so averages should be interpreted with some caution. More quotes would give a more reliable picture of what's typical in the area.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to its higher-than-average premium. Understanding these factors can help homeowners make more informed decisions.

Age and Construction (1953, Weatherboard)

Built in 1953, this home is over 70 years old. Older homes often attract higher premiums because they can be more expensive to repair or rebuild — materials may no longer be standard, and compliance with modern building codes adds cost. Weatherboard timber construction, while charming and common in riverside NSW communities, is also considered higher risk by insurers due to its susceptibility to fire, moisture, and pest damage compared to brick or rendered construction.

Stumped Foundation

A home on stumps (timber or concrete piers) introduces additional risk factors — particularly around subsidence, movement, and flood vulnerability. In a riverside location like Brooklyn, where the Hawkesbury River is a defining feature of the landscape, this is especially relevant. Insurers typically price this risk into the premium.

Timber and Laminate Flooring

Timber flooring in an older home on stumps can be costly to repair or replace following water ingress or flooding events — another factor that may push premiums upward.

Solar Panels and Ducted Climate Control

Both of these inclusions add to the replacement value of the home. Solar panels are a meaningful asset, and ducted climate control systems are expensive to reinstall. Ensuring these are adequately covered is important, but they do contribute to a higher sum insured and therefore a higher premium.

Granny Flat

The presence of a granny flat increases the overall footprint and replacement cost of the property. Depending on the policy, a granny flat may or may not be automatically included in the building cover — it's worth confirming this with your insurer.

No Pool, No Cyclone Risk

On the positive side, the absence of a pool removes a common liability risk, and Brooklyn falls outside designated cyclone risk zones, which keeps that particular loading off the table.

---

Tips for Homeowners in Brooklyn

1. Review your sum insured carefully A $600,000 building sum insured is significant for a 105 sqm home. While it's important not to underinsure, it's equally worth ensuring the figure reflects realistic rebuild costs rather than market value. Consider getting a building replacement cost estimate from a quantity surveyor to make sure your cover is calibrated correctly.

2. Ask about flood and water damage exclusions Brooklyn's position on the Hawkesbury River means flooding is a genuine risk. Some policies exclude flood cover by default or charge a significant loading for it. Read the Product Disclosure Statement (PDS) carefully and confirm whether flood, storm surge, and riverine flooding are all covered under your policy.

3. Shop around — seriously Given this quote is more than four times the suburb median, there is real money to be saved by comparing insurers. Premiums for the same property can vary enormously between providers. Use CoverClub's free quote comparison tool to see what other insurers are offering for your specific property.

4. Consider your excess settings Both the building and contents excess are set at $1,000 here, which is fairly standard. Opting for a higher voluntary excess (say, $2,500 or $5,000) can meaningfully reduce your annual premium — particularly useful if you're primarily seeking cover for major events rather than minor claims.

---

Compare Your Options with CoverClub

Whether you're a long-time Brooklyn local or new to the area, it always pays to compare. Home insurance premiums can vary dramatically between providers for the exact same property — and as this quote illustrates, there can be significant room to find better value. Head to CoverClub to get a personalised comparison for your home and see what's available in the market today. It's free, fast, and could save you thousands.