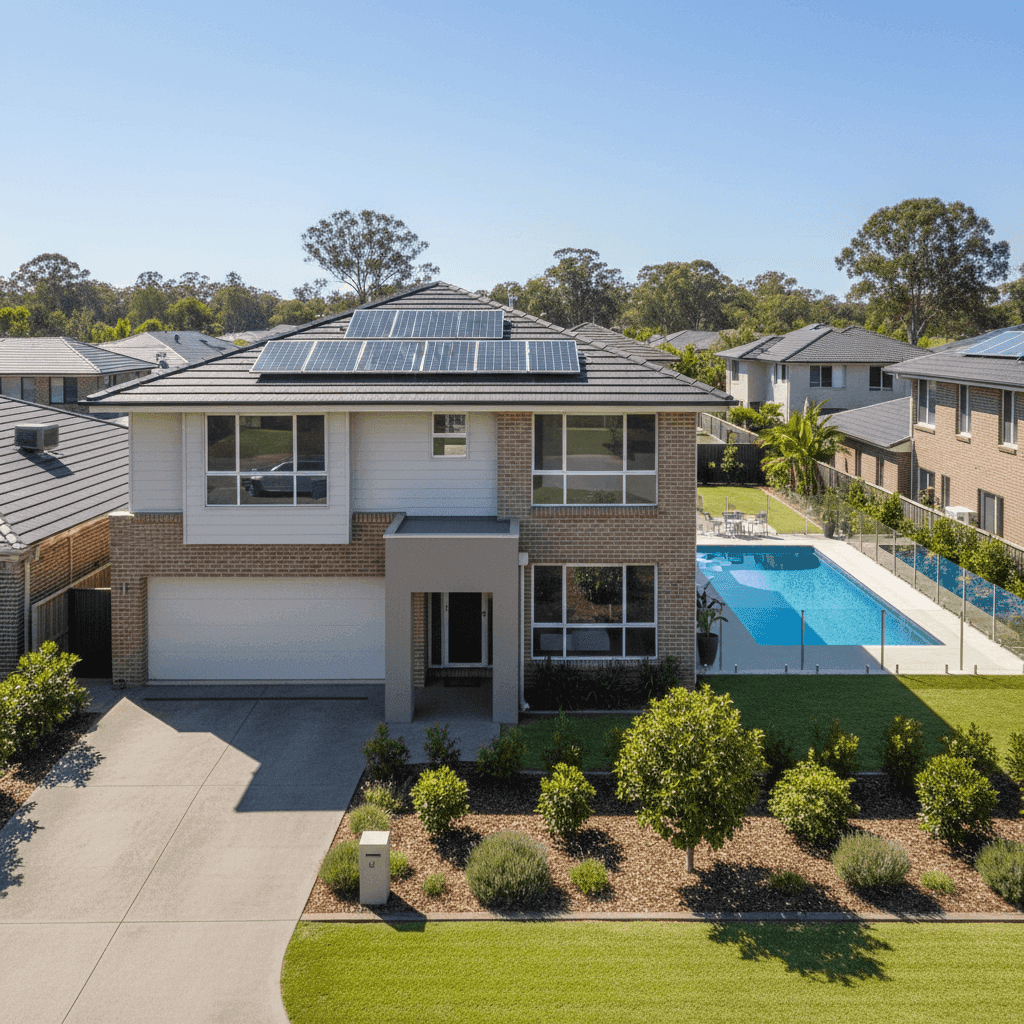

Brookwater is one of South-East Queensland's most sought-after master-planned communities, sitting within the City of Ipswich and known for its golf course, leafy streetscapes, and modern housing stock. If you own a free-standing home here, you already know the area commands premium property values — and, as this quote analysis shows, home insurance premiums can reflect that too.

This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom free-standing home in Brookwater (postcode 4300), helping you understand what's driving the cost and whether there's room to save.

---

Is This Quote Fair?

The quote in question comes in at $3,912 per year (or $364/month) for combined home and contents cover, with a building sum insured of $1,730,000 and contents valued at $82,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive (Above Average).

To put that in context, the suburb average for Brookwater sits at $3,030/year, and the median is $2,800/year. This quote lands well above the 75th percentile for the suburb ($3,387/year), meaning it's pricier than at least three-quarters of comparable quotes we've seen in the area.

That said, "expensive" doesn't automatically mean "wrong." The building sum insured of $1,730,000 is notably high — reflecting the above-average fittings quality and the 235 sqm footprint of this home. A higher replacement value will always push premiums upward, and insurers price accordingly. The question worth asking is whether that sum insured is accurately calibrated to the true rebuild cost, or whether it may be set slightly higher than necessary.

---

How Brookwater Compares

Understanding where Brookwater sits relative to broader benchmarks is useful when evaluating any quote. Here's a snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Brookwater (suburb) | $3,030/yr | $2,800/yr |

| Ipswich LGA | $8,901/yr avg | — |

| Queensland (state) | $9,129/yr avg | $3,903/yr |

| National | $5,347/yr avg | $2,764/yr |

A few things stand out here. The Queensland state average of $9,129/year looks alarming at first glance, but that figure is heavily skewed by high-risk coastal and cyclone-prone regions in North Queensland. The state median of $3,903/year is a far more representative number for most South-East Queensland homeowners — and this quote, at $3,912/year, sits almost exactly at that median.

Compared to the national average of $5,347/year, this quote is actually below average. And relative to the broader Ipswich LGA average of $8,901/year, Brookwater homeowners are faring considerably better — a reflection of the suburb's newer housing stock, lower flood risk in many parts, and well-maintained infrastructure.

You can explore localised premium data for Brookwater directly on the Brookwater suburb stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on what insurers charge. Here's how each one plays a role:

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is generally viewed favourably by insurers. It's durable, fire-resistant, and less susceptible to wind damage compared to lightweight cladding or metal roofing. This combination typically attracts more competitive premiums.

Slab Foundation A concrete slab foundation is standard for modern Queensland builds and presents minimal risk from an insurer's perspective. It's structurally sound and less prone to subsidence or pest-related damage than older pier-and-beam foundations.

Construction Year: 2017 A relatively recent build means the property was constructed under modern Australian building codes, which include improved cyclone strapping, waterproofing standards, and energy efficiency requirements. Newer homes generally attract lower premiums than ageing properties.

Above-Average Fittings Quality This is a significant premium driver. Above-average fittings — think stone benchtops, quality cabinetry, premium fixtures, and high-end flooring — substantially increase the cost to rebuild or repair. Insurers factor this into the sum insured calculation, which is likely a key reason this quote sits above the suburb average.

Swimming Pool Pools add liability exposure and increase the replacement cost of the property. Most insurers include pool cover within the building policy, but it does contribute to a higher overall premium.

Solar Panels Solar panels are increasingly common in Queensland, and most modern home insurance policies cover them as part of the building. However, their replacement cost (panels, inverter, and installation) adds to the total sum insured, nudging premiums slightly higher.

Ducted Climate Control A ducted air conditioning system is a high-value fixed asset. Like solar panels, it's typically covered under the building policy and contributes to the overall replacement value of the home.

No Cyclone Risk Brookwater is not classified as a cyclone risk area, which is a meaningful saving compared to properties in North Queensland or coastal Far North QLD. Cyclone-rated premiums can be multiples higher, so this is a genuine advantage for Brookwater homeowners.

---

Tips for Homeowners in Brookwater

1. Review your sum insured carefully At $1,730,000, the building sum insured is substantial. It's worth getting an independent building replacement cost estimate — not the market value of the property, but the actual cost to demolish and rebuild from scratch, including professional fees and site costs. Over-insuring inflates your premium without providing additional benefit at claim time.

2. Compare at least three quotes before renewing Insurers price risk differently, and the gap between the cheapest and most expensive quote for the same property can be significant. Using a comparison platform like CoverClub makes it easy to see multiple options side by side without having to ring around.

3. Consider your excess settings Both excesses on this policy are set at $1,000, which is fairly standard. However, if you're comfortable covering smaller claims out of pocket, increasing your excess to $2,000 or more can reduce your annual premium noticeably. Just make sure the saving justifies the higher out-of-pocket cost in a claim scenario.

4. Bundle building and contents — but check the maths This quote covers both building and contents under a single policy, which is often (but not always) more cost-effective than two separate policies. It's worth occasionally pricing them separately to confirm you're getting the best combined deal.

---

Ready to Compare?

Whether you're renewing an existing policy or shopping for cover on a new purchase, it pays to compare. CoverClub makes it simple to benchmark your premium against real data from your suburb and find cover that suits your home and budget. Get a quote today and see how your current premium stacks up.