Buderim is one of the Sunshine Coast's most sought-after suburbs — a leafy, elevated community known for its heritage village feel, strong school catchments, and easy access to the coast. It's also a suburb where homeowners are increasingly asking a very reasonable question: am I paying too much for home insurance? This article breaks down a real home and contents insurance quote for a five-bedroom, free-standing home in Buderim (postcode 4556) and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $3,249 per year (or $319 per month) for combined home and contents cover, with a building sum insured of $900,000 and contents valued at $157,000. Both the building and contents excess sit at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Based on 145 quotes collected for Buderim properties, the suburb average premium is $3,047 per year, with a median of $2,913. This quote sits modestly above both figures — roughly 7% above the suburb average and about 11% above the median.

That said, "average" doesn't mean overpriced. This property carries a relatively high building sum insured ($900,000 for a 277 sqm home built in 2000), which will naturally push the premium higher than a comparable property insured for less. The contents value of $157,000 is also meaningful. When you factor in those coverage levels, a premium landing in the upper-middle portion of the suburb range is entirely reasonable.

---

How Buderim Compares

To properly assess this quote, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This Quote | $3,249/yr |

| Buderim Suburb Average | $3,047/yr |

| Buderim Suburb Median | $2,913/yr |

| Buderim 25th Percentile | $2,162/yr |

| Buderim 75th Percentile | $3,545/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| Sunshine Coast LGA Average | $7,249/yr |

A few things jump out immediately. The Queensland state average of $9,129 per year is extraordinarily high — a reflection of the significant number of high-risk properties across the state, including those in flood-prone, cyclone-affected, and coastal areas. Buderim, sitting on elevated ground and outside designated cyclone risk zones, benefits considerably from its geography. Homeowners here are paying a fraction of what many other Queenslanders face.

Compared to the national average of $5,347, this quote also looks competitive. Even the Sunshine Coast LGA average of $7,249 is well above what Buderim homeowners typically pay — again, largely because the LGA encompasses lower-lying, more flood- and storm-exposed areas that drag the average upward.

For this property, landing between the suburb's 25th and 75th percentiles ($2,162–$3,545) confirms the "fair" rating. You're not getting a bargain, but you're not being gouged either.

---

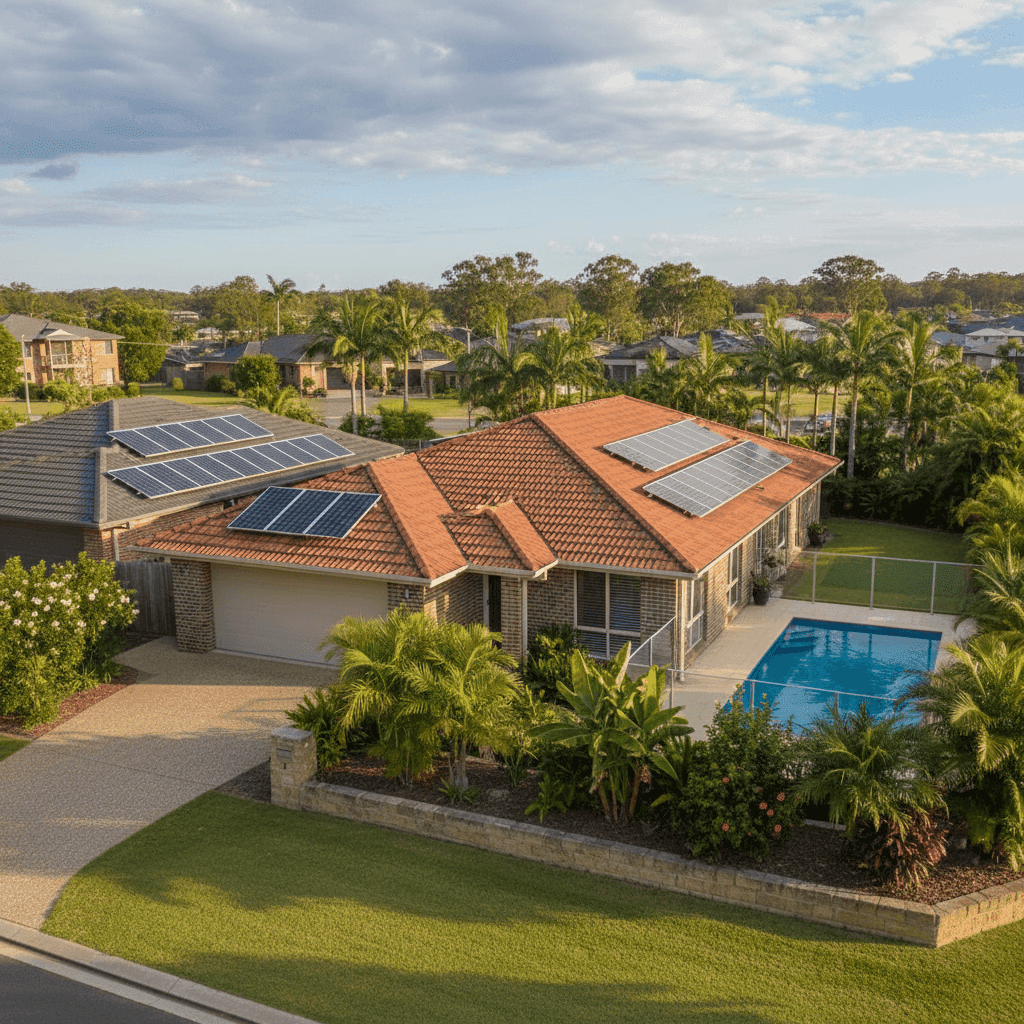

Property Features That Affect Your Premium

Several characteristics of this home have a direct bearing on the premium calculated.

Brick veneer construction and tiled roof are generally viewed favourably by insurers. Both materials offer solid resistance to fire and are considered durable, which can help moderate premiums compared to properties with timber cladding or metal roofing in some risk scenarios.

Slab foundation is the standard for Queensland homes of this era and presents no particular risk flag for insurers. Combined with tiled flooring throughout, the property profile is straightforward and well-understood by underwriters.

The swimming pool adds to the insured value and introduces some liability considerations — pool-related incidents are a real factor in home insurance claims. Insurers typically factor this into their pricing, so it's worth ensuring your policy explicitly covers pool structures and any associated liability.

Solar panels are an increasingly common feature on Sunshine Coast homes, and they do add to the replacement cost of the building. A 277 sqm home with a solar system could easily add $10,000–$20,000 or more to rebuild costs, which should be reflected in the building sum insured. At $900,000, this quote appears to account for a thorough rebuild estimate.

Standard fittings quality keeps things straightforward. Homes with high-end or custom finishes typically attract higher premiums due to the increased cost of like-for-like replacement. Standard fittings mean fewer surprises in the claims process.

The absence of ducted climate control is a minor point, but it does mean one less expensive system to insure or replace — a small factor in the overall equation.

---

Tips for Homeowners in Buderim

1. Review your building sum insured annually. Construction costs have risen significantly in recent years across South-East Queensland. A sum insured of $900,000 for a 277 sqm brick veneer home is substantial, but it's worth running a rebuild cost estimate each year — particularly given ongoing labour and materials inflation. Underinsurance remains one of the most common and costly mistakes homeowners make.

2. Don't overlook your pool and solar in your contents and building schedules. Make sure your policy clearly covers the pool structure (including fencing, pumps, and filtration equipment) under the building component, and that your solar panel system is listed explicitly. Some policies treat solar panels as a separate item or apply specific sub-limits.

3. Consider your excess strategically. Both excesses on this policy are set at $1,000. If you have the financial buffer to absorb a higher out-of-pocket cost in the event of a claim, increasing your excess to $1,500 or $2,000 can meaningfully reduce your annual premium. Conversely, if cash flow is tight, the current level provides reasonable protection.

4. Compare quotes at renewal — every year. Even a "fair" quote can become uncompetitive over time as insurers adjust their pricing models. The 145-quote dataset for Buderim shows a wide spread between the 25th and 75th percentiles ($2,162 to $3,545), which means there's genuine variation in what insurers will charge for similar properties. Shopping around at renewal is one of the simplest ways to keep your premium in check.

---

Ready to Compare?

Whether you're renewing an existing policy or insuring a new property, it pays to see what's available across multiple insurers. Get a home insurance quote at CoverClub and compare your options side by side — it only takes a few minutes, and you might be surprised at the range of premiums on offer for your Buderim home. You can also explore detailed suburb-level insurance statistics for Buderim to benchmark any quote you receive.