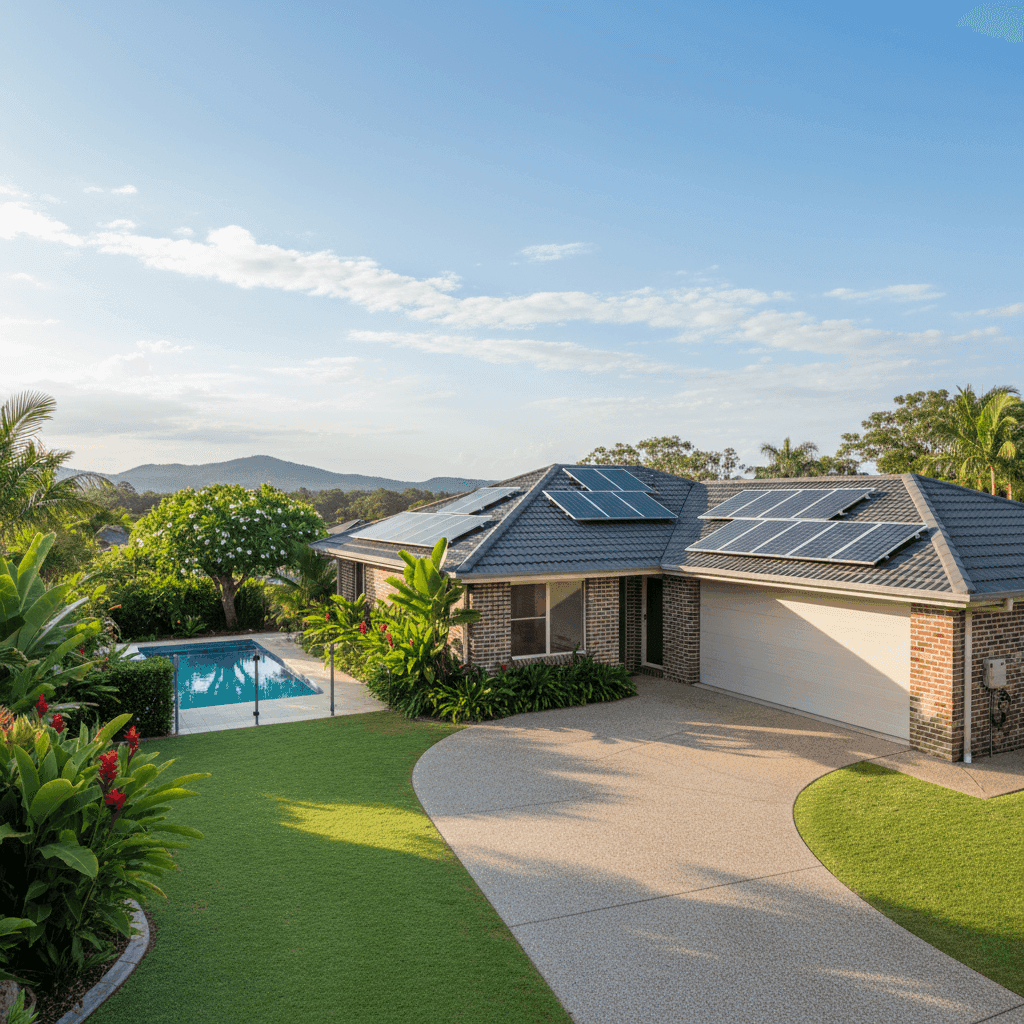

Buderim is one of the Sunshine Coast's most sought-after suburbs — a leafy, elevated enclave known for its character homes, strong community feel, and easy access to beaches, schools, and the Bruce Highway. It's also a suburb where home insurance costs can vary significantly depending on your property's age, construction, and the insurer you choose. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Buderim (postcode 4556), and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: yes — and then some. This quote came in at $2,583 per year (or $253/month) for combined home and contents cover, with a building sum insured of $798,000 and contents valued at $200,000. Our pricing model rates this as CHEAP — below the suburb average — and the data backs that up clearly.

The suburb average for Buderim sits at $4,210/year, meaning this policy is roughly $1,627 cheaper than what most homeowners in the area are paying. Even compared to the 25th percentile — the cheapest quarter of quotes in the suburb — this policy at $2,583 still comes in well below the $2,938 threshold. That's a genuinely strong result.

It's worth noting that the building excess is $3,000 and the contents excess is $1,000, which are on the higher end. A higher excess typically reduces the annual premium, so part of the savings here may reflect that trade-off. Whether that's the right balance depends on your financial position — if you'd struggle to cover a $3,000 excess in the event of a claim, it may be worth reviewing whether a lower-excess option is available, even at a slightly higher premium.

---

How Buderim Compares

To understand just how competitive this quote is, it helps to zoom out and look at the broader pricing landscape. Based on data from CoverClub's Buderim suburb stats, here's how premiums stack up across 37 quotes collected for the area:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,583 |

| Buderim 25th Percentile | $2,938 |

| Buderim Median | $4,074 |

| Buderim Average | $4,210 |

| Buderim 75th Percentile | $5,181 |

| Sunshine Coast LGA Average | $4,608 |

| QLD State Average | $4,547 |

| QLD State Median | $3,931 |

| National Average | $2,965 |

| National Median | $2,716 |

A few things stand out here. First, Buderim's average premium of $4,210 is notably higher than the national average of $2,965 — a gap of over $1,200. This reflects the elevated risk profile of South East Queensland more broadly, where storm activity, flooding, and hail events drive insurer costs upward.

Second, the Queensland state average of $4,547 is among the highest in the country, and the Sunshine Coast LGA average of $4,608 is even higher still. Buderim's elevation (it sits atop a ridge) does offer some protection from flooding compared to lower-lying coastal areas, but insurers still price QLD properties at a premium relative to southern states.

This quote, at $2,583, actually sits below even the national average — a remarkable outcome for a Queensland property with a pool, solar panels, and a building insured for nearly $800,000.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining through an insurance lens:

Brick Veneer Construction (1988) Brick veneer homes are generally viewed favourably by insurers. The brick outer layer provides good fire resistance and structural durability, while the timber frame interior is standard for the era. A 1988 build sits in a middle ground — old enough that some components (roofing, plumbing, electrical) may be approaching end-of-life, but not so old as to attract the heavy surcharges sometimes applied to pre-1970s homes.

Tiled Roof Terracotta or concrete tile roofs are a common feature of Queensland homes and are generally considered durable. They perform well in high-wind conditions compared to corrugated iron, though individual tiles can crack or dislodge in severe storms. Insurers typically view tiled roofs as a moderate-to-low risk factor.

Concrete Slab Foundation Slab foundations are standard across Queensland and are associated with good structural stability. Unlike homes with raised timber floors or stumps, slab homes have limited subfloor exposure, which can reduce certain moisture-related risks.

Swimming Pool A pool adds to the replacement cost of the property and is factored into the building sum insured. It also introduces a liability consideration — most home and contents policies include legal liability cover, which is relevant for pool owners given Queensland's strict pool fencing laws.

Solar Panels Solar panels are increasingly common on Queensland homes, and most insurers now include them under building cover. It's worth confirming with your insurer that your panels and inverter are explicitly covered, including for storm damage and power surge events.

---

Tips for Homeowners in Buderim

1. Review your building sum insured annually Construction costs have risen sharply in recent years. A building insured for $798,000 today may not reflect full replacement cost in two or three years' time. Use a building cost calculator or ask your insurer to reassess the sum insured at renewal to avoid being underinsured.

2. Check your pool and solar panel coverage explicitly Don't assume these are automatically included in your policy. Ask your insurer to confirm that your pool equipment (pump, filtration, heating) and solar system (panels, inverter, wiring) are covered under the building section, and understand any sublimits that may apply.

3. Consider the excess trade-off carefully This policy carries a $3,000 building excess. While it helps keep the premium down, it means you'd need to fund the first $3,000 of any building claim yourself. If your emergency fund is solid, this is a reasonable trade-off. If not, it's worth getting comparison quotes with a lower excess to see the premium difference.

4. Compare quotes at renewal — every year The insurance market in Queensland is competitive and pricing can shift significantly between insurers year to year. Even if you're happy with your current policy, running a comparison before renewal takes minutes and could save you hundreds. Get a quote at CoverClub to see what's available for your specific property.

---

Find the Right Cover for Your Buderim Home

Whether you're a first-time buyer or a long-term Buderim resident, getting the right home insurance at a fair price matters. The quote analysed here is a strong example of what's possible when you shop around — well below the suburb and state averages, with solid cover in place for building and contents.

CoverClub makes it easy to compare home and contents insurance quotes tailored to your property. Enter your address at CoverClub to see how your current premium stacks up and whether there's a better deal available for your home.