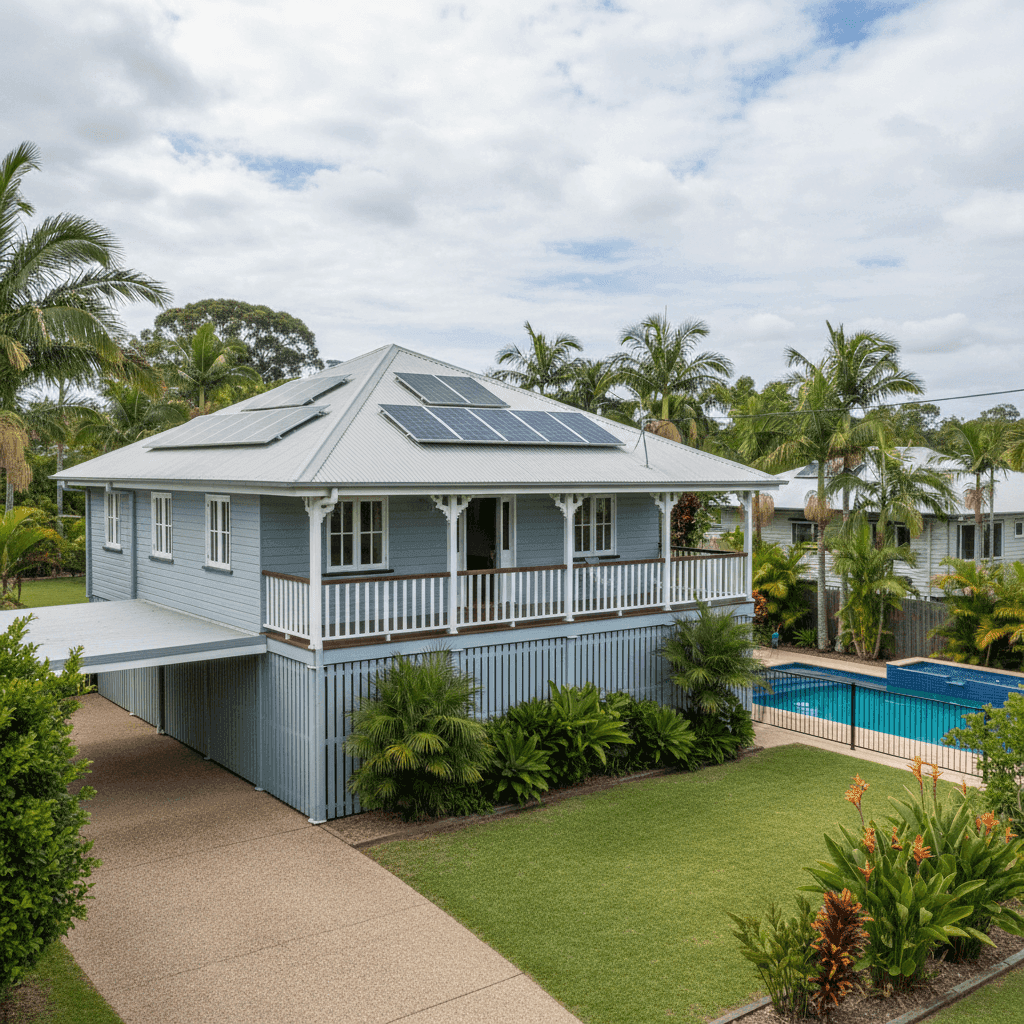

Buderim is one of the Sunshine Coast's most sought-after suburbs — a leafy, elevated ridge community that blends relaxed hinterland living with easy access to the coast. But for homeowners here, understanding the true cost of insuring a free standing home can be just as important as finding the right property in the first place. This article breaks down a real home and contents insurance quote for a 4-bedroom, 2-bathroom weatherboard home in Buderim, and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $4,173 per year (or $400/month), covering both building (sum insured: $865,000) and contents ($50,000 insured value), with a $1,000 excess on each.

Our pricing analysis rates this quote as Expensive — Above Average for the area. Based on a sample of 145 quotes from the Buderim area (postcode 4556), the suburb average sits at $3,047/yr and the median at $2,913/yr. That means this quote is running roughly $1,126 above the suburb average — a meaningful gap worth investigating.

That said, it's not entirely surprising. Several features of this property — including its elevated construction, weatherboard timber walls, timber/laminate flooring, and the presence of a pool, solar panels, and ducted climate control — all contribute to a higher-than-typical replacement cost and risk profile. The building sum insured of $865,000 is also on the higher end for a 235 sqm home, which will directly influence the premium.

If you're in a similar position, the key question isn't just whether the quote seems high — it's whether the coverage and sum insured accurately reflect your property, and whether you've shopped around enough to know you're getting a competitive rate.

---

How Buderim Compares

To understand whether this quote is genuinely expensive or simply reflective of a pricier property, it helps to zoom out and look at the broader landscape.

| Benchmark | Premium |

|---|---|

| This Quote | $4,173/yr |

| Buderim suburb average | $3,047/yr |

| Buderim suburb median | $2,913/yr |

| Buderim 25th percentile | $2,162/yr |

| Buderim 75th percentile | $3,545/yr |

| Sunshine Coast LGA average | $7,249/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, while this quote is above the Buderim suburb average, it sits well below the Sunshine Coast LGA average of $7,249/yr and even further below the Queensland state average of $9,129/yr. That state figure is heavily skewed by high-risk coastal and flood-prone areas across Queensland where premiums can be extraordinarily high.

Compared to the national average of $5,347/yr, this quote actually comes in below — which is a more meaningful comparison for a property of this type and value.

So while the "Expensive" rating is accurate in a local Buderim context, this quote is not out of step with what Queenslanders and Australians broadly pay for home and contents cover. The local suburb median of $2,913/yr likely reflects a mix of smaller homes, lower sum insured amounts, and properties without the additional features (pool, solar, elevated construction) that this property carries.

---

Property Features That Affect Your Premium

Several characteristics of this home have a direct bearing on what insurers charge. Here's how they stack up:

Weatherboard timber walls are among the more expensive wall types to insure. Timber is more susceptible to fire, rot, and pest damage than brick or rendered masonry, and is generally more costly to repair or replace. This is a notable premium driver.

Elevated construction (at least 1 metre) is a double-edged sword. On the positive side, elevation reduces flood risk — a major concern in Queensland. However, elevated homes can be more expensive to rebuild due to the additional structural complexity, and they may be more exposed to wind damage.

Steel/Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant, and performs well in storms compared to older roofing materials. This may offer a slight moderating effect on the premium.

Swimming pool adds to the replacement cost of the property and introduces liability considerations, both of which push premiums upward.

Solar panels represent a significant asset on the roof. Most policies cover solar panels under the building sum insured, but their replacement cost — particularly for a full system on a 235 sqm home — can be substantial. Ensuring your sum insured accounts for this is critical.

Ducted climate control is another high-value fixture that increases the cost to rebuild or replace the home to its current standard. It's the right call to include it in your building sum insured, but it does add to the overall premium.

Slab foundation and timber/laminate flooring round out a home that, while not in a cyclone risk zone, has a premium material profile throughout.

---

Tips for Homeowners in Buderim

1. Review your sum insured annually At $865,000 for a 235 sqm weatherboard home with a pool, solar, and ducted air conditioning, the building sum insured here is substantial. Construction costs have risen sharply in recent years — make sure your figure reflects current rebuild costs, not what you paid or what the home is worth on the market. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Shop around — and do it every year The gap between the 25th percentile ($2,162/yr) and the 75th percentile ($3,545/yr) in Buderim is over $1,300. That's a significant spread, and it reflects how differently insurers price the same suburb. Use a comparison tool like CoverClub to see multiple quotes side by side before renewing.

3. Check what's covered for your pool and solar panels Not all policies treat pools and solar panels the same way. Some require you to specify them separately, others include them automatically under the building definition. Confirm with your insurer that both are fully covered for accidental damage, storm damage, and liability (particularly for the pool).

4. Consider your excess carefully Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess — say $2,500 — can meaningfully reduce your annual premium. If you're a low-claims household, this trade-off often makes financial sense. Just ensure you could comfortably cover that excess in the event of a claim.

---

Compare Home Insurance Quotes in Buderim

Whether this quote reflects your own situation or you're simply trying to understand what's fair for your Buderim home, the best way to know is to compare. CoverClub makes it easy to see how your premium stacks up against real data from your suburb and beyond — and to get competing quotes in minutes. Start your comparison today and make sure you're not paying more than you need to for the cover your home deserves.