Bulimba is one of Brisbane's most sought-after riverside suburbs — a leafy, character-filled pocket of the inner east where Queenslander-style architecture sits alongside modern builds. If you own a free standing home here, protecting it with the right building insurance is essential. This article breaks down a real building-only insurance quote for a 3-bedroom, 4-bathroom free standing home in Bulimba (QLD 4171), and puts the numbers in context so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The annual premium on this quote comes in at $2,663 per year (or $248 per month), covering a building sum insured of $884,000 with a $2,000 building excess. Our pricing analysis rates this as CHEAP — below average for the area.

That's a significant finding. Bulimba sits in a suburb where insurance costs can be substantial, so landing a quote well below the local going rate is genuinely noteworthy. For homeowners who've been stung by renewal increases in recent years, this kind of result is a reminder that shopping around still pays off.

To put it plainly: this quote is not just cheap relative to the suburb — it's also below the Queensland state average and only slightly below the national median. In a market where premiums have climbed sharply post-floods and post-COVID, that's a strong outcome.

---

How Bulimba Compares

The numbers tell a compelling story when you line them up side by side:

| Benchmark | Premium |

|---|---|

| This quote | $2,663/yr |

| Bulimba suburb average | $10,418/yr |

| Bulimba suburb median | $10,925/yr |

| Bulimba 25th percentile | $9,374/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Brisbane LGA average | $16,277/yr |

The Bulimba suburb average sits at $10,418 per year — nearly four times the cost of this particular quote. Even the suburb's 25th percentile (meaning the cheapest quarter of quotes) comes in at $9,374 — still more than three times higher. The Brisbane LGA average of $16,277 per year underscores just how expensive home insurance can get in this part of Queensland.

It's worth noting that the QLD state median of $3,903 is considerably lower than the state average of $9,129 — a gap that reflects how a handful of very high-risk properties (flood-prone, cyclone-exposed, or on difficult terrain) can skew averages upward. This quote, at $2,663, sits comfortably below even the state median, which is an excellent result.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the final premium — some favourably, others less so.

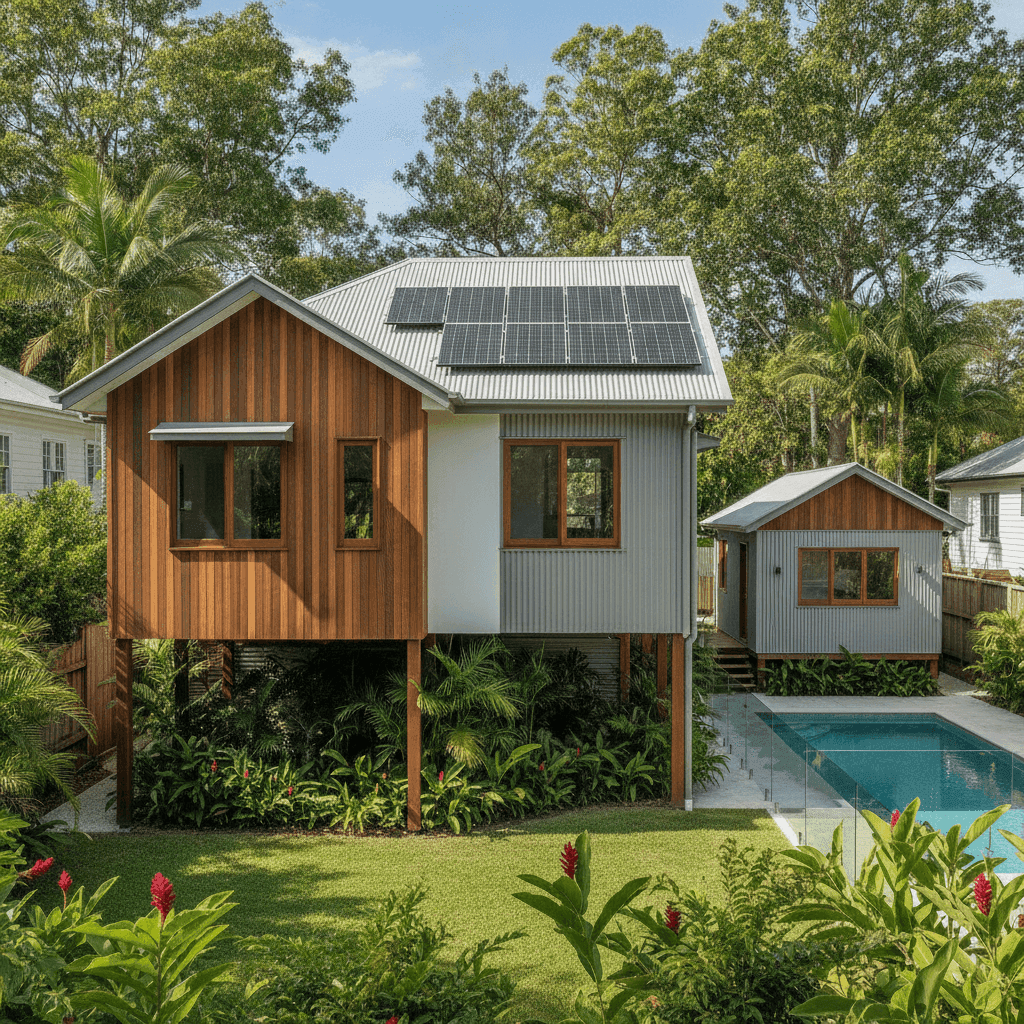

Pole Foundation

This home is built on poles, which is extremely common in Queensland and particularly in riverside suburbs like Bulimba. Pole homes can be viewed favourably by insurers in flood-prone areas because the elevated design reduces the risk of inundation reaching the living areas. This may be contributing to the competitive premium on this quote.

Steel/Colorbond Roof

A Colorbond steel roof is generally well-regarded by insurers. It's durable, fire-resistant, and performs well in severe weather — all factors that can reduce risk and, by extension, premiums.

Timber and Laminate Flooring

Timber and laminate floors are common in Queensland homes and are generally straightforward to insure. However, they can be more susceptible to water damage than tiles, which is worth keeping in mind if you're ever assessing your level of cover.

Above-Average Fittings

The property features above-average quality fittings, which is reflected in the $884,000 sum insured. Higher-quality finishes cost more to repair or replace, so it's important that your sum insured accurately reflects full rebuild costs — not just the market value of the property.

Pool, Solar Panels, and Granny Flat

The combination of a swimming pool, rooftop solar panels, and a granny flat adds complexity to a building policy. Each of these features represents an additional asset that needs to be covered under the building sum insured. Confirm with your insurer that all three are explicitly included in your policy — particularly the granny flat, which some standard policies treat as a separate structure requiring specific mention.

No Cyclone Risk

Bulimba falls outside designated cyclone risk zones, which removes one of the most significant premium loading factors for Queensland properties. Homeowners further north in QLD can pay dramatically more due to cyclone exposure — so this is a meaningful cost advantage for Bulimba residents.

---

Tips for Homeowners in Bulimba

1. Verify your granny flat is covered Don't assume your building policy automatically extends to a granny flat or secondary dwelling. Review your Product Disclosure Statement (PDS) carefully and contact your insurer to confirm the granny flat is included in your sum insured. If it's not, you may need to declare it separately.

2. Review your sum insured annually Construction costs in Queensland have risen sharply in recent years. A sum insured of $884,000 may be appropriate today, but it's worth reassessing each year at renewal. Underinsurance — where your cover falls short of actual rebuild costs — remains one of the most common and costly mistakes homeowners make.

3. Check your flood cover status Even though this property's elevated pole design reduces flood risk, Bulimba sits near the Brisbane River and has experienced significant flooding events historically. Confirm whether your policy includes flood cover (not just storm or rainwater damage) and understand the difference — they're not the same thing.

4. Don't auto-renew without comparing Given that this quote came in well below the suburb average, it's clear that premiums vary enormously between insurers for the same property. Make it a habit to compare quotes at renewal rather than accepting whatever figure lands in your inbox. A few minutes of comparison could save you thousands.

---

Ready to Compare Your Home Insurance?

Whether you're a Bulimba local or a Queensland homeowner looking to benchmark your current premium, CoverClub makes it easy to compare building and contents insurance quotes in one place. Get a quote today and see how your current cover stacks up — you might be surprised by what you find.

For more localised data on insurance costs in your area, explore the Bulimba suburb stats, browse Queensland-wide averages, or check out national benchmarks to get the full picture.