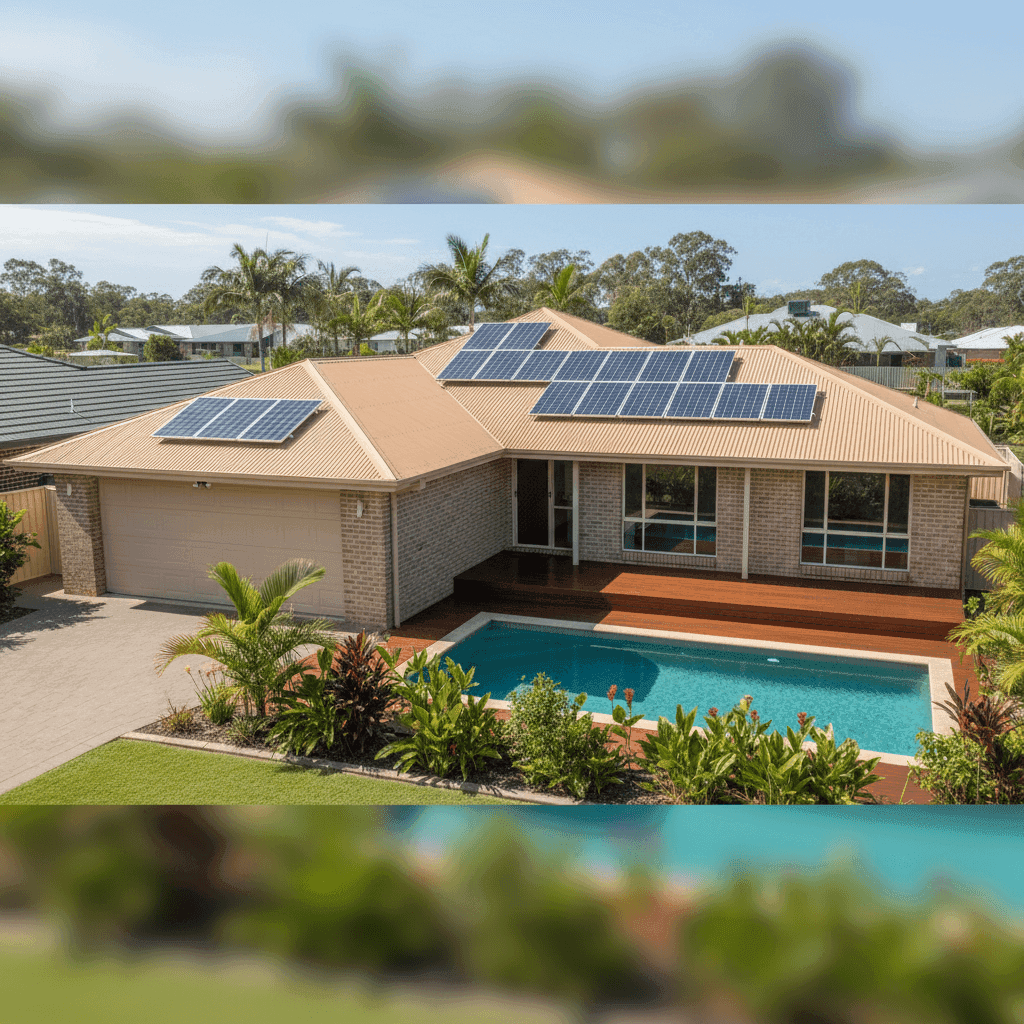

If you own a free standing home in Bundaberg North, QLD 4670, you've probably wondered whether you're paying a fair price for home insurance — or whether you're leaving money on the table. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom brick veneer home in the suburb, and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $4,711 per year (or $445 per month) for combined home and contents cover, with a building sum insured of $700,000 and contents valued at $100,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average.

That might sound underwhelming, but in the context of Bundaberg North's insurance market, it's actually a reasonably strong result. The suburb average premium sits at $8,181 per year, and the median is $7,132 per year — meaning this quote comes in well below what most homeowners in the area are paying. In fact, at $4,711, this premium lands between the suburb's 25th percentile ($3,956/yr) and the median ($7,132/yr), placing it in the more affordable half of the local market.

The "Fair" rating reflects that while the quote isn't rock-bottom cheap, it's competitive given the property's size, features, and location — and it's substantially better than what many neighbours are likely paying.

---

How Bundaberg North Compares

To understand whether this premium makes sense, it helps to zoom out and look at the broader picture. Here's how Bundaberg North stacks up against Queensland and the national average:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Bundaberg North (4670) | $8,181/yr | $7,132/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

(Based on 104 quotes analysed for the Bundaberg North suburb.)

The numbers tell a clear story: Bundaberg North is a notably expensive suburb for home insurance by any measure. The suburb average is nearly 80% higher than the Queensland state average, and almost three times the national average. This reflects the elevated risk profile of many properties in regional Queensland — including flood exposure, storm damage history, and the general cost pressures facing insurers in non-metropolitan areas.

You can explore the full suburb breakdown on the Bundaberg North insurance stats page, compare it against the Queensland state overview, or see where it sits on the national insurance stats page.

For this particular property, securing a premium of $4,711 — below both the suburb average and median — represents genuine value in a market where costs can easily spiral past $10,000 per year.

---

Property Features That Affect Your Premium

Every home is different, and insurers weigh up a range of property-specific factors when calculating your premium. Here's how the key features of this Bundaberg North home likely influence the cost:

Brick Veneer Walls & Colorbond Roof

Brick veneer is generally viewed favourably by insurers — it's durable, fire-resistant, and holds up well against the elements. Paired with a steel Colorbond roof (constructed in 2007), the home benefits from materials that are considered low-to-moderate risk. Colorbond roofing is particularly well-regarded in Queensland for its resistance to heat, wind, and rain.

Concrete Slab Foundation

A slab foundation is typically one of the more insurer-friendly options. It's structurally sound and less susceptible to movement or pest damage compared to older stumped or timber-framed subfloors. This likely has a modest positive effect on the premium.

Timber & Laminate Flooring

Timber and laminate floors are attractive but can be costly to repair or replace following water damage or flooding. Insurers factor in the replacement cost of internal fittings, so this may nudge the contents and building replacement estimates slightly higher.

Swimming Pool

Having a pool on the property adds to the overall insured value and introduces additional liability considerations. Pool-related incidents — from property damage to third-party liability — are a factor insurers account for, which can contribute to a marginally higher premium.

Solar Panels

Solar panels are increasingly common in Queensland, and most insurers now include them as part of the building sum insured. Panels can be expensive to replace after storm or hail damage, so their presence is factored into the building replacement cost calculation. Ensuring your sum insured of $700,000 adequately covers the panels (and any associated inverter or battery system) is worth confirming with your insurer.

214 sqm Building Size

At 214 square metres, this is a comfortably sized family home. Larger floor areas generally mean higher rebuild costs, which flows through to a higher building sum insured — and therefore a higher premium. The $700,000 sum insured reflects the cost to fully rebuild the home to its current standard, including fixtures, fittings, and site costs.

Standard Fittings Quality

With standard-grade fittings throughout, the home avoids the premium uplift that comes with high-end or luxury finishes. This is one area where the property works in the owner's favour from an insurance pricing perspective.

---

Tips for Homeowners in Bundaberg North

Whether you're reviewing an existing policy or shopping for new cover, here are four practical steps to help you get the best outcome:

- Check your sum insured regularly. Building costs in Queensland have risen significantly in recent years. Make sure your $700,000 building sum insured still reflects the true cost to rebuild — not just the market value of your home. Underinsurance is one of the most common and costly mistakes homeowners make.

- Bundle home and contents for savings. As demonstrated in this quote, combining building and contents cover under a single policy often attracts a discount compared to taking out separate policies. It also simplifies the claims process.

- Review your excess settings. A $1,000 excess is fairly standard, but increasing it voluntarily can reduce your annual premium. If you have a solid emergency fund and are unlikely to make small claims, a higher excess could save you money each year.

- Compare quotes annually. The Bundaberg North market shows enormous variation — from under $3,956 at the 25th percentile to over $11,980 at the 75th percentile. Loyalty doesn't always pay in insurance. Shopping around at renewal time is one of the most effective ways to avoid overpaying.

---

Ready to Compare Home Insurance Quotes?

If you're a homeowner in Bundaberg North or anywhere else in Queensland, it pays to know what the market looks like before you commit to a policy. CoverClub makes it easy to compare home and contents insurance quotes from multiple insurers in one place — so you can see exactly where your premium sits and whether there's a better deal available.

Get a home insurance quote at CoverClub today and find out if you're paying a fair price for your home.