If you own a free standing home in Bungendore, NSW 2621, you've probably noticed that insurance premiums can vary quite a bit depending on who you ask. Bungendore is a charming township in the Snowy Monaro Regional Council area, sitting roughly 35 kilometres east of Canberra. It's a popular spot for tree-changers and families looking for a relaxed rural lifestyle without straying too far from the capital. But like any property market, home insurance costs here come with their own unique set of drivers — and understanding them can help you make a smarter purchasing decision.

This article breaks down a recent building-only insurance quote for a 4-bedroom, 2-bathroom free standing home in Bungendore, compares it against local, state and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,602 per year (or $255 per month) for building-only cover, with a $1,000 building excess and a sum insured of $750,000. Our price rating for this quote is EXPENSIVE — above average for the area.

To put that in context, the suburb average premium for Bungendore sits at $2,252 per year, with a median of $2,044. This quote lands well above both figures — roughly $350 above the suburb average and $558 above the median. It also sits above the 75th percentile for the suburb ($2,503), meaning it's more expensive than approximately three-quarters of comparable quotes in the area.

That said, "expensive" doesn't automatically mean "wrong." A higher sum insured, specific property features, or the insurer's own risk appetite can all push a premium upward. The key question is whether the coverage justifies the cost — and whether shopping around might reveal a more competitive rate for the same level of protection.

---

How Bungendore Compares

Understanding where Bungendore sits relative to broader benchmarks gives important perspective. Here's a quick snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Bungendore (suburb) | $2,252/yr | $2,044/yr |

| Snowy Monaro LGA | $2,614/yr | — |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the NSW state average of $9,528 is extraordinarily high — this is heavily skewed by flood-prone and high-risk postcodes across the state, particularly in northern NSW and areas around the Hawkesbury. The state median of $3,770 is a more reliable benchmark for typical NSW homeowners.

Compared to the national median of $2,764, the Bungendore suburb median of $2,044 is actually quite favourable, suggesting the area is generally considered lower risk on a national scale. The quote in question, at $2,602, does exceed the national median — but it remains well below the NSW state median, which speaks to the relatively contained risk profile of this region.

You can explore more local data on the Bungendore suburb insurance stats page, compare it to the NSW state overview, or see how it stacks up against national home insurance benchmarks.

---

Property Features That Affect Your Premium

Every property is different, and insurers weigh a range of characteristics when calculating your premium. Here's how the features of this particular home play into the pricing:

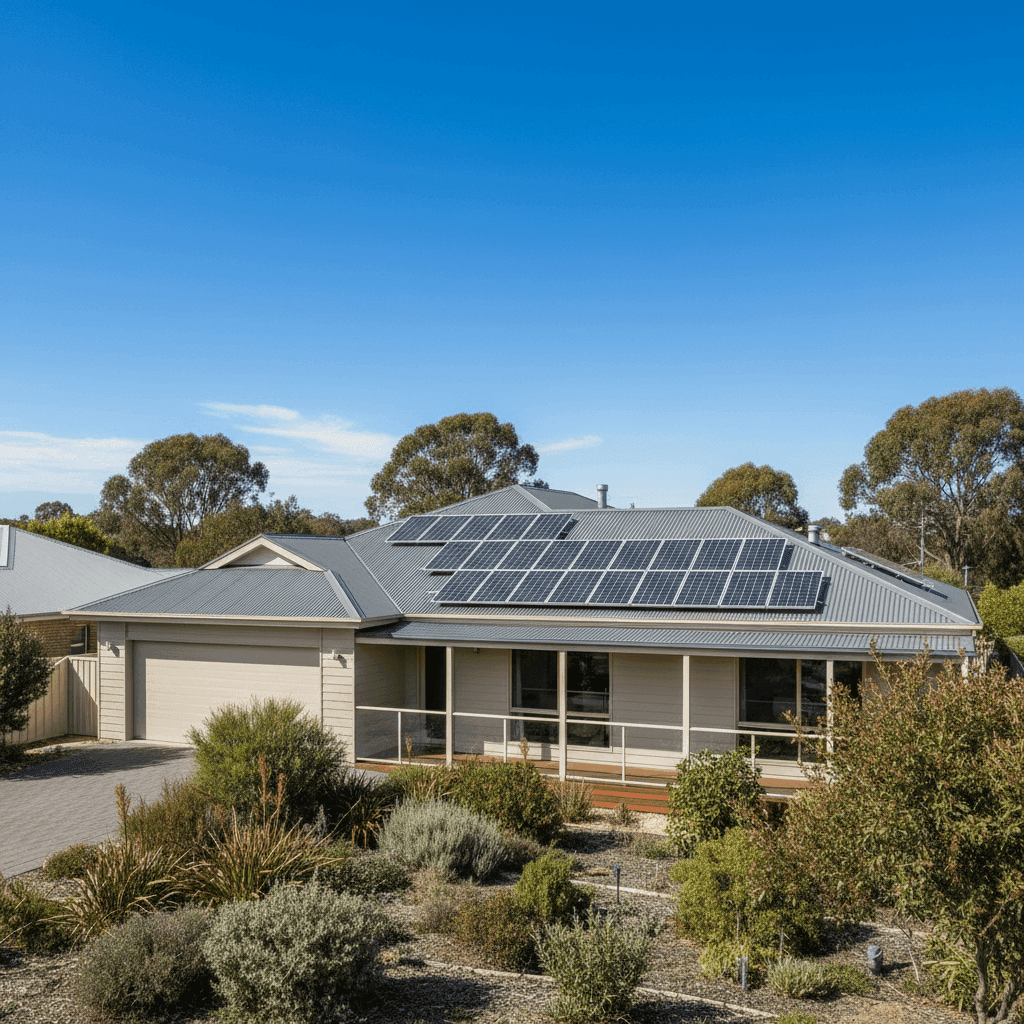

Hardiplank / Hardiflex External Walls

Fibre cement cladding such as Hardiplank and Hardiflex is generally viewed favourably by insurers. It's durable, fire-resistant, and low-maintenance compared to timber weatherboard. This material is common in newer and renovated homes in regional NSW and typically doesn't attract a loading.

Steel / Colorbond Roof

A Colorbond steel roof is considered one of the better roofing materials from an insurance perspective. It's resistant to fire, won't crack or warp, and handles the temperature swings common in the Bungendore region well. Insurers generally price this more competitively than terracotta tiles or older corrugated iron.

Concrete Slab Foundation

Slab-on-ground construction is standard for homes of this era and is well-regarded by underwriters. It reduces the risk of subsidence and pest-related damage compared to elevated timber stumps.

Solar Panels

This property includes rooftop solar panels, which are increasingly common across regional NSW. Solar panels do add replacement value to the building and may contribute modestly to the premium, as they can be costly to repair or replace after storm or hail damage. It's worth confirming with your insurer that solar is explicitly covered under your policy.

Ducted Climate Control

Ducted air conditioning systems are a meaningful addition to a home's insured value. These systems are expensive to replace, and their presence is reflected in the sum insured calculation.

Construction Year (1993) and Size (130 sqm)

A home built in 1993 is well past the point of being considered "new," but it's not so old as to raise significant concerns around outdated wiring or plumbing. At 130 sqm, it's a modestly sized home relative to the 4-bedroom, 2-bathroom configuration, which may indicate a more compact or efficient floorplan.

Sum Insured: $750,000

The sum insured is a significant factor here. At $750,000 for a 130 sqm home, the per-square-metre rebuild cost works out to roughly $5,769/sqm — which is on the higher end but not unreasonable when accounting for current construction costs, site accessibility in regional NSW, and inclusions like ducted climate control and solar.

---

Tips for Homeowners in Bungendore

Whether you're reviewing an existing policy or shopping for the first time, here are four practical steps to help manage your home insurance costs in Bungendore:

- Review your sum insured carefully. Underinsurance is a real risk, but overinsurance costs you money every year. Use a professional building replacement cost calculator or get a quantity surveyor's estimate to ensure your sum insured reflects current rebuild costs — not just the market value of your property.

- Compare multiple quotes. With this quote sitting above the suburb's 75th percentile, it's worth getting at least two or three competing quotes. Insurers price risk differently, and savings of $300–$600 per year are entirely achievable for the same level of cover.

- Ask about bundling discounts. If you're also insuring contents, a vehicle, or other assets, many insurers offer multi-policy discounts that can bring your overall cost down meaningfully.

- Check your excess settings. A $1,000 excess is fairly standard, but increasing it to $1,500 or $2,000 can reduce your annual premium. This makes sense if you're financially comfortable covering minor claims out of pocket and want to reduce your recurring costs.

---

Compare Home Insurance Quotes in Bungendore

If this quote feels a little steep, you're not alone in asking the question. The good news is that the home insurance market is competitive, and the right policy for your property is out there. CoverClub makes it easy to compare building insurance options side by side so you can see exactly what you're paying for — and where you might be able to save.