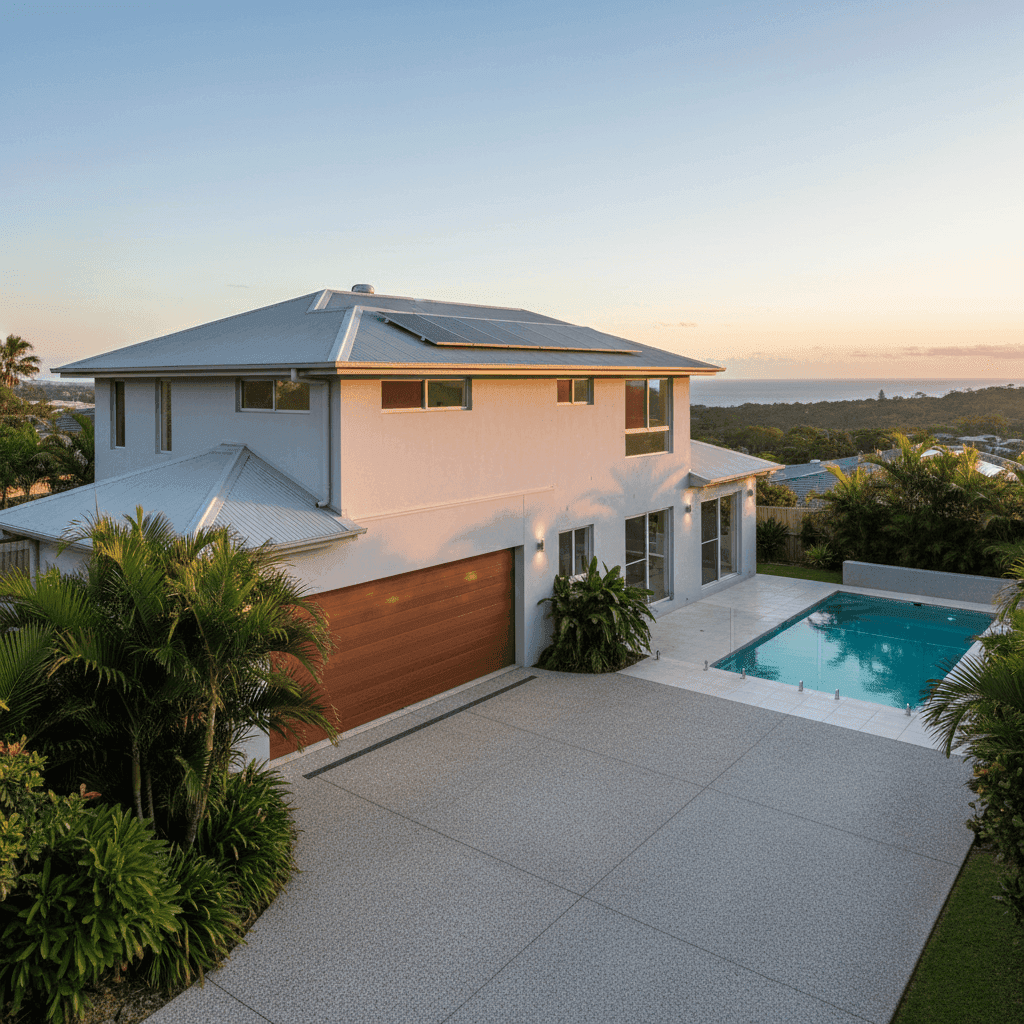

Burleigh Heads is one of the Gold Coast's most sought-after coastal suburbs — a blend of relaxed beach lifestyle, modern development, and strong property values. If you own a free standing home here, you already know that protecting it with the right insurance is non-negotiable. But how do you know whether the premium you're being quoted is actually good value? This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom free standing home in Burleigh Heads (postcode 4220), and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,895 per year (or $277/month) for combined home and contents cover, with a building sum insured of $844,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — around average for the area. That might sound underwhelming, but in the context of Burleigh Heads and the broader Queensland market, "around average" is actually a reasonably comfortable position to be in.

The suburb average premium sits at $4,169 per year, meaning this quote is roughly $1,274 below the local average — a meaningful saving. It also comes in under the suburb median of $3,193/yr, placing it closer to the 25th percentile ($2,339/yr) than the 75th ($4,971/yr). In practical terms, this homeowner is paying less than the majority of their neighbours for comparable cover.

That said, there's still room to explore whether a better deal exists. Being below average doesn't necessarily mean you're at the floor of the market.

---

How Burleigh Heads Compares

To appreciate how this quote stacks up, it helps to zoom out and look at the broader picture. You can explore full pricing data on the Burleigh Heads insurance stats page, the Queensland state overview, and national insurance statistics.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Burleigh Heads (4220) | $4,169/yr | $3,193/yr |

| Gold Coast LGA | $8,161/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out from this data:

- Queensland's average premium is extraordinarily high at $9,129/yr — one of the most expensive states in the country for home insurance. This is largely driven by extreme weather events, particularly cyclones and flooding in regional and northern parts of the state.

- Burleigh Heads bucks the state trend. The suburb average of $4,169/yr is well below the QLD average, reflecting the relatively lower-risk profile of this part of the Gold Coast compared to areas further north.

- The Gold Coast LGA average of $8,161/yr is significantly higher than the Burleigh Heads suburb average, suggesting that some Gold Coast postcodes are dragging that LGA figure up considerably — likely those in higher flood or storm surge zones.

- Nationally, the median premium of $2,764/yr is actually slightly below this quote, which is a reminder that even a "fair" local price may still have room for improvement when shopping broadly.

Based on a sample of 50 quotes in the 4220 postcode, the spread is wide — ranging from around $2,339/yr at the 25th percentile up to $4,971/yr at the 75th. This variability underscores the importance of comparing multiple insurers rather than accepting the first quote you receive.

---

Property Features That Affect Your Premium

The characteristics of this particular property play a meaningful role in how insurers price the risk. Here's what's likely influencing the premium:

Hebel external walls are generally viewed favourably by insurers. Autoclaved aerated concrete (AAC) panels like Hebel offer strong fire resistance and durability, which can contribute to more competitive premiums compared to timber-framed homes.

Steel/Colorbond roofing is another positive signal. Colorbond is a proven, low-maintenance roofing material that performs well in Queensland's harsh climate — resisting heat, wind, and corrosion. Insurers tend to rate it well.

Slab foundation is standard for new builds in Queensland and is generally considered low-risk from a structural perspective, particularly in areas without significant flood exposure.

New construction (2024) is a significant premium advantage. Brand-new homes are built to current Australian Standards and the latest building codes, meaning they're structurally sound, electrically compliant, and less likely to generate claims related to wear and deterioration.

Swimming pool adds to the insured value and introduces some liability considerations, which can nudge premiums upward slightly. Ensuring your policy includes adequate liability cover for pool-related incidents is important.

Solar panels add replacement value to the building sum insured and may be a factor in the $844,000 building valuation. It's worth confirming with your insurer that panels are explicitly covered under the building section of your policy.

Ducted climate control is a high-value fixture that contributes to the overall building replacement cost. Again, verifying this is captured in your sum insured is worthwhile.

Vinyl flooring and standard fittings keep the fit-out value at a moderate level, which helps contain the contents and building valuation compared to premium finishes.

No cyclone risk designation is a notable advantage for this property. While Burleigh Heads is in Queensland, it sits outside the officially designated cyclone-prone zones that apply to much of northern QLD — and this can make a substantial difference to premiums.

---

Tips for Homeowners in Burleigh Heads

1. Review your building sum insured annually Construction costs have risen sharply in recent years. A 2024 build at 235 sqm is currently insured for $844,000 — roughly $3,591/sqm — which is a reasonable estimate, but rebuild costs can shift. Make sure your sum insured keeps pace with current construction rates to avoid being underinsured.

2. Confirm what's covered under your solar and pool Both solar panels and swimming pools can be grey areas in standard policies. Check whether your solar system is covered for accidental damage and storm damage, and whether your pool structure, pump, and filtration equipment are included. Some policies require these to be listed separately.

3. Shop around at renewal time Even with a "fair" rating, there's a meaningful gap between the 25th and 75th percentile premiums in this suburb. Loyalty doesn't always pay — insurers frequently offer better rates to new customers. Use a comparison tool like CoverClub to benchmark your renewal quote before accepting it.

4. Consider your excess carefully Both excesses on this policy are set at $1,000. Opting for a higher excess (say, $2,000 or $2,500) can reduce your annual premium noticeably. If you have a strong financial buffer and are unlikely to make small claims, this trade-off can make good financial sense over time.

---

Find a Better Deal with CoverClub

Whether you're renewing your existing policy or insuring a new purchase, it pays to compare. CoverClub aggregates real insurance data from across Australia to help homeowners make informed decisions. Get a home insurance quote today and see how your premium stacks up against what others in Burleigh Heads and across Queensland are actually paying.