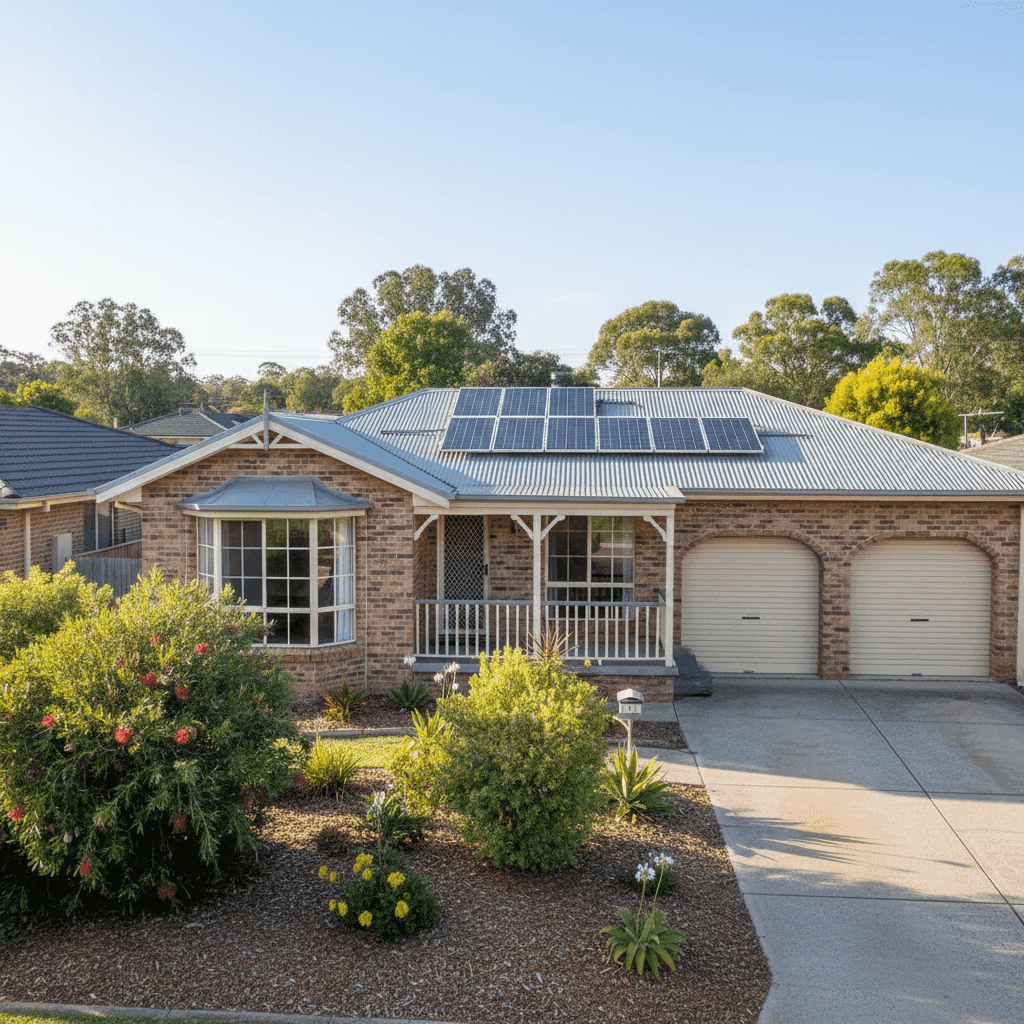

If you own a free standing home in Burnside, QLD 4560, you've probably noticed that home insurance isn't exactly cheap. Sitting within the Sunshine Coast Local Government Area, Burnside is a quiet residential suburb where property values — and the cost of protecting them — have been on the rise. This article takes a close look at a real home and contents insurance quote for a three-bedroom, two-bathroom brick veneer home in the suburb, unpacking whether it represents fair value and what local homeowners can do to keep premiums in check.

---

Is This Quote Fair?

The quote in question comes in at $3,085 per year (or $289 per month) for combined home and contents cover, with a building sum insured of $456,000 and contents valued at $50,000. Both the building and contents excesses are set at $1,000 each.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. At $3,085 per year, this premium sits comfortably within the middle band of what Burnside homeowners are currently paying. It's above the suburb median of $2,408/yr, but well below the 75th percentile of $3,169/yr — meaning roughly three-quarters of comparable quotes in the area come in at a similar price or higher.

This is not a bargain, but it's also not an outlier. For a home of this size, age, and construction type in a regional Queensland suburb, a premium in this range is broadly in line with market expectations. That said, "fair" doesn't mean you can't do better — and we'll touch on that shortly.

---

How Burnside Compares

To put this quote into proper context, it helps to zoom out and look at the broader pricing landscape. Here's how Burnside stacks up against state and national benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Burnside (QLD 4560) | $2,740/yr | $2,408/yr |

| Queensland (State) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| Sunshine Coast LGA | $7,249/yr | — |

(Based on [Burnside suburb data](https://coverclub.com.au/stats/QLD/4560/burnside), [QLD state data](https://coverclub.com.au/stats/QLD), and [national insurance data](https://coverclub.com.au/stats/national) from CoverClub.)

A few things stand out here. First, the Queensland state average of $9,129/yr is extraordinarily high — driven largely by North Queensland postcodes where cyclone risk pushes premiums into the stratosphere. The median of $3,903/yr is a more realistic representation of what most Queenslanders pay, and even against that figure, this Burnside quote looks competitive.

Compared to the Sunshine Coast LGA average of $7,249/yr, the Burnside quote of $3,085/yr is notably lower. This again reflects the wide variation within regional Queensland — coastal and flood-prone areas within the same LGA can attract dramatically higher premiums than inland suburban properties like those in Burnside.

Against the national median of $2,764/yr, this quote is modestly above average, which aligns with the "fair" rating. Burnside isn't a high-risk postcode by national standards, but Queensland's elevated weather risk profile does push premiums slightly above what you'd expect to pay in, say, suburban Melbourne or Adelaide.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on the premium calculated. Understanding these can help you anticipate costs and make smarter decisions at renewal time.

Brick Veneer Construction Brick veneer is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to weatherboard or fibrous cement cladding. This construction type typically attracts lower premiums than more vulnerable wall materials, and it's a positive factor for this property.

Steel / Colorbond Roof Colorbond steel roofing is highly regarded in the Australian insurance market. It's resistant to fire, handles heavy rain well, and has a long lifespan. Insurers tend to price this more favourably than tile roofs, which can crack, leak, or suffer hail damage more readily.

Concrete Slab Foundation A slab-on-ground foundation is standard for Queensland homes of this era and is considered low-risk from an insurer's perspective. It eliminates the under-floor moisture and pest issues sometimes associated with raised timber stumps, which can be a cost factor in older homes.

Timber / Laminate Flooring While attractive and popular, timber and laminate flooring can be more expensive to replace than carpet following a water or flood event. Insurers factor in the higher reinstatement cost of these materials when calculating premiums, particularly for contents cover.

Solar Panels This property has solar panels installed. While solar is great for energy bills, it does add to the overall replacement value of the home and may slightly increase the building sum insured required to achieve adequate cover. It's important to ensure your sum insured accounts for the cost of replacing the solar system.

Ducted Climate Control Ducted air conditioning is a significant built-in asset. Like solar panels, it contributes to the overall rebuild cost and is a factor in why the building sum insured of $456,000 is appropriate for a 139 sqm home. Underinsuring a home with premium fixtures like ducted climate control is a common and costly mistake.

Construction Year: 1997 At roughly 27 years old, this home is mature but not aged. Homes from the late 1990s were built to reasonable cyclone and structural standards, though not to the more stringent modern building codes introduced post-2000. This can have a modest upward effect on premiums compared to newer builds.

---

Tips for Homeowners in Burnside

1. Review Your Sum Insured Annually Building costs in Queensland have risen sharply over the past few years due to labour shortages and material price increases. A sum insured of $456,000 for a 139 sqm home with solar and ducted air conditioning is reasonable today, but it's worth reassessing each year at renewal. Underinsurance is one of the most common problems homeowners face at claim time.

2. Consider Increasing Your Excess This policy carries a $1,000 excess on both building and contents. If you have a financial buffer and are unlikely to make small claims, opting for a higher excess (say $1,500 or $2,000) can meaningfully reduce your annual premium. Just make sure the saving justifies the additional out-of-pocket risk.

3. Bundle Your Cover Thoughtfully Combined home and contents policies, like this one, often come with a bundling discount compared to taking out two separate policies. However, it's still worth comparing the bundled price against standalone options — some insurers price one component very competitively while inflating the other.

4. Compare at Every Renewal The insurance market is dynamic, and loyalty doesn't always pay. Insurers regularly adjust their pricing models, and a premium that was competitive two years ago may no longer be the best available. Using a comparison tool like CoverClub at each renewal takes only a few minutes and could save you hundreds of dollars.

---

Find a Better Deal with CoverClub

Whether you're happy with your current insurer or suspect you might be overpaying, it always pays to compare. CoverClub makes it easy to see how your home insurance quote stacks up against real data from your suburb, your state, and across Australia. Get a quote today and find out if you're getting the cover you deserve at a price that makes sense.