Burnside is a quiet residential suburb nestled in the Sunshine Coast hinterland, sitting just west of Nambour in postcode 4560. It's a popular choice for families seeking a relaxed lifestyle with easy access to coastal amenities — and like many Queensland suburbs, home insurance here comes with its own set of considerations. This article breaks down a recent building insurance quote for a free standing home in Burnside, examines how it measures up against local, state, and national benchmarks, and offers practical guidance for homeowners looking to make the most of their cover.

---

Is This Quote Fair?

The quote in question — $2,900 per year (or around $283 per month) for building-only cover on a 235 sqm free standing home — has been rated Fair (Around Average). That rating is well-supported by the data.

Compared to the suburb average of $2,740/yr and the suburb median of $2,408/yr, this premium sits modestly above both benchmarks. It lands comfortably within the interquartile range for Burnside, which runs from $1,899/yr at the 25th percentile to $3,169/yr at the 75th percentile. In other words, roughly half of all comparable quotes in the area fall between those two figures — and this one sits in the upper-middle portion of that range.

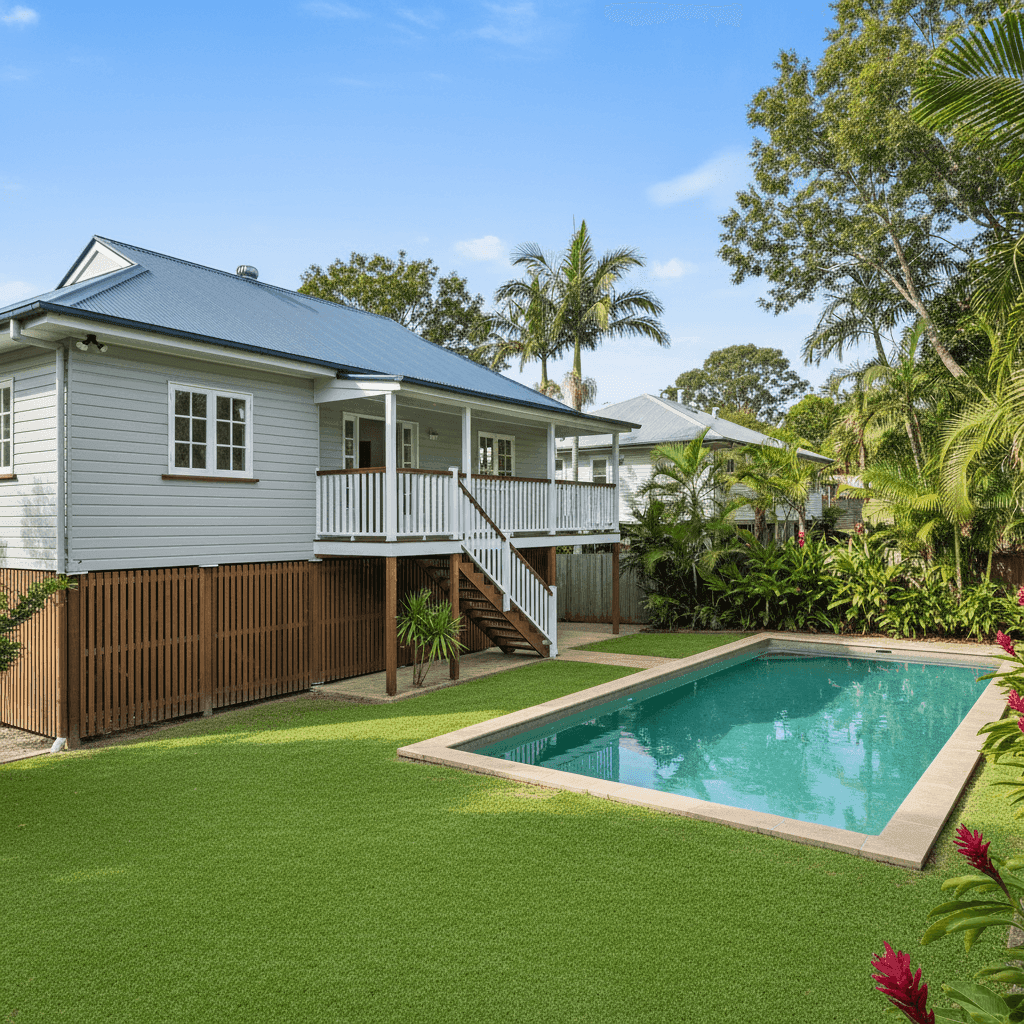

Given the property's characteristics — a pole-frame construction, timber/laminate flooring, and a swimming pool — a slight premium above the suburb median is entirely reasonable. These features introduce specific risk considerations that insurers price accordingly. The $1,000 building excess is also standard for this type of property and cover level.

The sum insured of $820,000 reflects the cost to rebuild a well-appointed, 235 sqm home to modern standards, which is a sensible and realistic figure for the Sunshine Coast region.

---

How Burnside Compares

To properly contextualise this quote, it helps to zoom out and look at the broader picture. Here's how Burnside stacks up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Burnside (4560) | $2,740/yr | $2,408/yr |

| Sunshine Coast LGA | $7,249/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The contrast between Burnside's figures and the broader Queensland average is striking. At $9,129/yr, the Queensland state average is more than three times the Burnside suburb average — a reflection of the enormous variability in risk across the state. Coastal and cyclone-prone regions in Far North Queensland, along with flood-affected areas in South East Queensland, drive that state average significantly upward.

The Sunshine Coast LGA average of $7,249/yr also sits well above Burnside's local figures. This is likely influenced by beachside suburbs and areas with greater flood or storm surge exposure within the broader LGA boundary.

Nationally, the average sits at $5,347/yr, again well above what Burnside homeowners are typically paying. Even the national median of $2,764/yr is only marginally higher than Burnside's suburb median.

The takeaway? Burnside is a relatively affordable suburb for home insurance by both state and national standards. You can explore the full data for this suburb at the Burnside insurance stats page, or compare it against the Queensland state overview and national benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful bearing on the premium calculated:

Pole Frame Foundation

The home is elevated on poles — a classic Queensland construction style that offers excellent ventilation and, in many cases, improved resilience against localised flooding and moisture. However, insurers view pole-frame homes with nuance: while they can fare well in minor flood events, the elevated structure introduces specific risks around subfloor damage, pest ingress, and structural movement. Premiums for pole homes are often slightly higher than slab-on-ground equivalents.

Hardiplank / Hardiflex Cladding

The external walls are clad in fibre cement sheeting — a durable, low-maintenance material that performs well in Queensland's humid subtropical climate. It's resistant to rot and termites, which insurers generally view favourably. This is a positive factor in the risk assessment.

Steel / Colorbond Roof

Colorbond roofing is widely regarded as one of the most resilient roofing materials available in Australia. It handles heat, heavy rain, and wind exceptionally well, and its longevity reduces the likelihood of weather-related claims. This is another tick in the homeowner's favour.

Swimming Pool

A pool adds value to a property but also introduces liability considerations and increases the complexity of a rebuild. Pool fencing compliance, equipment replacement, and potential water damage to surrounding structures all factor into how insurers assess the risk. Homeowners with pools should ensure their sum insured accounts for the full cost of pool reinstatement.

Ducted Climate Control

Ducted air conditioning systems are a significant fixed asset within the building. Their inclusion in the building sum insured is important — and at $820,000, this quote appears to account for that appropriately.

Construction Year: 2014

A home built in 2014 benefits from compliance with modern building codes, including improved cyclone and wind resistance standards introduced after the 2011 Queensland floods. This relatively recent construction date is a positive risk indicator.

---

Tips for Homeowners in Burnside

1. Review your sum insured annually Building costs in South East Queensland have risen sharply in recent years due to labour shortages and material price increases. A sum insured that was accurate two or three years ago may no longer reflect today's rebuild cost. Use a building cost calculator or speak with a quantity surveyor to verify your coverage remains adequate.

2. Check your policy's flood definition carefully Even in suburbs not classified as high-risk flood zones, heavy rainfall events can cause localised inundation. Policies vary significantly in how they define and cover flood versus storm water damage. Read the Product Disclosure Statement (PDS) closely and ask your insurer directly if you're unsure.

3. Maintain your pole frame subfloor Pole homes require periodic inspection of the subfloor space. Timber bearers and joists should be checked for pest damage, rot, and structural integrity. Some insurers exclude damage that results from lack of maintenance, so staying on top of this protects both your home and your claim eligibility.

4. Compare quotes before renewal Insurance loyalty rarely pays off in Australia. Insurers frequently offer better rates to new customers than to existing ones. Before your renewal date, take fifteen minutes to compare quotes at CoverClub — you may find equivalent cover at a meaningfully lower price.

---

Compare Your Own Quote

Whether you're a first-time buyer or a long-term Burnside resident, it's worth knowing where your premium sits relative to the market. CoverClub aggregates real insurance data from across Australia so you can benchmark your quote with confidence. Get started at CoverClub and see how your home insurance stacks up in seconds — no obligation, no personal details required to browse.