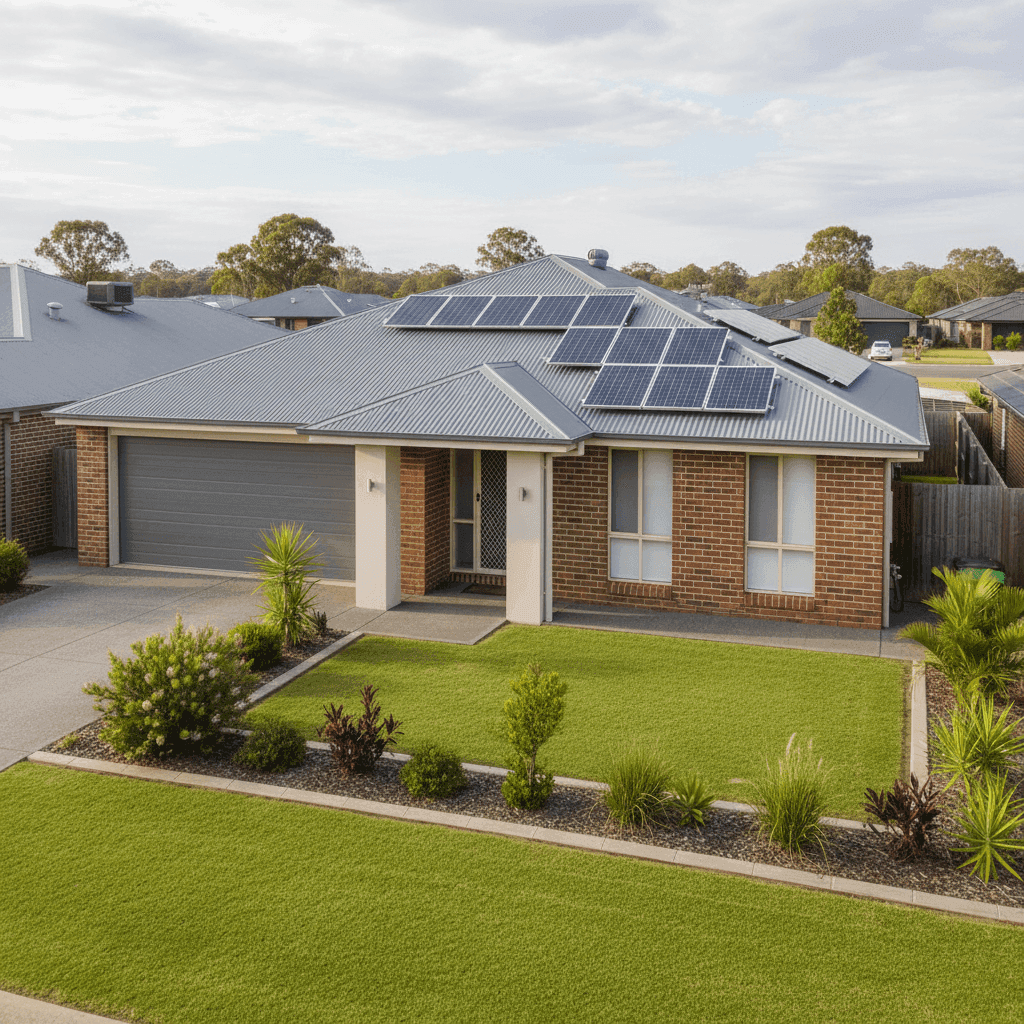

Burpengary East is a growing residential suburb in the Moreton Bay region of South East Queensland — a popular choice for families seeking newer homes with space, without straying too far from Brisbane. If you own or are considering insuring a free standing home in this area, understanding what a fair premium looks like can save you hundreds of dollars a year. This article breaks down a real home and contents insurance quote for a 4-bedroom, 2-bathroom brick veneer home in Burpengary East (postcode 4505) and puts the numbers into context.

---

Is This Quote Fair?

The quote in question comes in at $2,526 per year (or $241 per month) for combined home and contents cover, with a building sum insured of $674,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000 each.

Our pricing analysis rates this quote as CHEAP — below average for the area. That's a strong result for the homeowner. To put it simply: this premium sits comfortably below what most comparable properties in Burpengary East are paying, and it also undercuts both Queensland and national benchmarks.

For a property of this size — 214 sqm, built in 2002, with solar panels and ducted climate control — a sub-$2,600 annual premium represents genuine value. Insurers consider a wide range of variables when pricing a policy, and in this case, several factors appear to be working in the homeowner's favour.

---

How Burpengary East Compares

Looking at suburb-level data for Burpengary East (QLD 4505), the numbers tell an interesting story:

| Benchmark | Premium |

|---|---|

| This quote | $2,526/yr |

| Suburb 25th percentile | $3,283/yr |

| Suburb median | $4,589/yr |

| Suburb 75th percentile | $7,442/yr |

| Suburb average | $73,156/yr |

| LGA (Moreton Bay) average | $3,435/yr |

| QLD state median | $3,903/yr |

| QLD state average | $9,129/yr |

| National median | $2,764/yr |

| National average | $5,347/yr |

A couple of things stand out here. First, the suburb average of $73,156 is dramatically higher than the median of $4,589 — a classic sign that a small number of very high-cost outlier quotes are skewing the average upward (the suburb sample size is 16 quotes, which is relatively modest). The median is a more reliable indicator of typical costs in this postcode.

Against that median of $4,589, this quote of $2,526 is roughly 45% cheaper — a significant saving. It also beats the Moreton Bay LGA average of $3,435 and sits below the Queensland state median of $3,903. Interestingly, it's even marginally below the national median of $2,764, which is notable given that Queensland properties often attract higher premiums due to weather-related risks.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the competitive premium. Here's how each one plays into the insurer's risk assessment:

Brick Veneer Walls & Colorbond Roof

Brick veneer is widely regarded as a solid, low-maintenance wall construction — it resists fire and pests well and is a common choice in South East Queensland builds from the late 1990s and early 2000s. Paired with a steel Colorbond roof, this combination is generally viewed favourably by insurers. Colorbond is durable, lightweight, and performs well in high-wind events, which matters in Queensland.

Concrete Slab Foundation

A slab foundation is standard for homes of this era in QLD and typically presents a lower risk profile than stumped or suspended floors, particularly in terms of moisture ingress and structural movement. It's a neutral-to-positive factor for pricing.

Timber & Laminate Flooring

Flooring type can influence contents and building replacement costs. Timber and laminate floors are moderately priced to replace compared to premium hardwood or polished concrete, which helps keep the sum insured — and therefore the premium — in check.

Solar Panels

This property has solar panels installed. While solar adds value to a home, it also adds a small degree of complexity to insurance. Panels need to be covered under the building policy, and some insurers include them automatically while others require a specific endorsement. It's worth confirming your policy explicitly covers solar panel damage, including storm and hail events.

Ducted Climate Control

Ducted air conditioning systems are a significant asset — they can cost $10,000–$25,000 or more to replace. Ensuring your building sum insured accounts for this is important. At $674,000, the sum insured here appears to reflect a well-considered replacement cost estimate for a 214 sqm home of standard fittings quality.

No Cyclone Risk

Burpengary East falls outside designated cyclone risk zones, which is a meaningful premium advantage for Queensland homeowners. Properties in cyclone-prone areas of North Queensland can pay dramatically more for equivalent cover.

---

Tips for Homeowners in Burpengary East

Whether you're reviewing an existing policy or shopping for new cover, here are four practical steps to make sure you're getting the right protection at the right price.

1. Double-check your building sum insured annually Construction costs in South East Queensland have risen sharply over the past few years. A sum insured that was accurate two years ago may no longer reflect true rebuild costs. Use a building calculator or speak to a local builder to sense-check your figure — underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm solar panels are explicitly covered As mentioned, solar panel coverage isn't always automatic. Read your Product Disclosure Statement (PDS) carefully and ask your insurer directly whether panels are included, and up to what value. Given rising panel replacement costs, this is worth verifying.

3. Consider your excess level strategically Both excesses on this policy are set at $1,000. Opting for a higher excess can reduce your annual premium, but make sure you could comfortably cover that amount out of pocket in a claim scenario. Conversely, if you've set a low excess, you may be paying more in premiums than necessary.

4. Compare quotes at renewal — every year Even if you're happy with your insurer, the home insurance market shifts regularly. Loyalty doesn't always pay — in fact, many insurers offer better rates to new customers. Comparing quotes annually takes only a few minutes and could uncover significant savings, especially given how much variance exists across Burpengary East quotes.

---

Find the Right Cover for Your Home

This quote is a strong result — but the right policy for you depends on your specific property, risk appetite, and budget. Whether you're in Burpengary East or anywhere else in Australia, comparing multiple quotes side by side is the most reliable way to find genuine value.

[Get a home insurance quote at CoverClub](https://coverclub.com.au/?focus=address) and see how your property stacks up against suburb, state, and national benchmarks in seconds.