If you own a free standing home in Burringbar, NSW 2483, you're living in one of the Northern Rivers region's quieter, semi-rural pockets — a beautiful part of the world, but one that comes with its own set of insurance considerations. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom brick veneer home in the area, compares it against suburb, state, and national benchmarks, and offers practical tips to help you get the best value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,804 per year (or $274 per month) for combined home and contents insurance, covering a building sum insured of $746,000 and contents valued at $50,000. Both the building and contents excess are set at $5,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb average premium for Burringbar sits at $2,810 per year, meaning this quote lands almost exactly on the local benchmark. That's a reassuring sign that the policyholder isn't being significantly overcharged relative to their neighbours.

That said, "average" doesn't always mean "optimal." There's meaningful spread in what Burringbar homeowners are paying — the 25th percentile sits at $1,160/yr, while the 75th percentile reaches $3,994/yr. This wide range suggests that with the right insurer and policy structure, there may be room to reduce this premium without compromising on cover.

---

How Burringbar Compares

To put this quote in proper context, it helps to zoom out and look at the broader picture. Here's how Burringbar stacks up against state and national figures:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Burringbar (2483) | $2,810/yr | $1,326/yr |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

Note: Burringbar suburb data is based on a sample of 11 quotes. State and national figures draw on a much larger dataset.

At first glance, Burringbar's averages look remarkably affordable compared to the NSW state average of $9,528/yr and the national average of $5,347/yr. However, it's worth noting that the Tweed LGA average — the broader local government area that includes Burringbar — sits at a striking $26,089/yr. This outlier figure is likely influenced by high-value coastal properties and elevated flood or storm risk in parts of the Tweed region, and may not be representative of Burringbar's specific risk profile.

The national median of $2,764/yr is actually very close to this quote's $2,804/yr, reinforcing the "fair" rating. You can explore more localised data on the Burringbar suburb stats page.

---

Property Features That Affect Your Premium

Every home is unique, and insurers price risk based on a combination of property characteristics. Here's how the features of this particular home are likely influencing the premium:

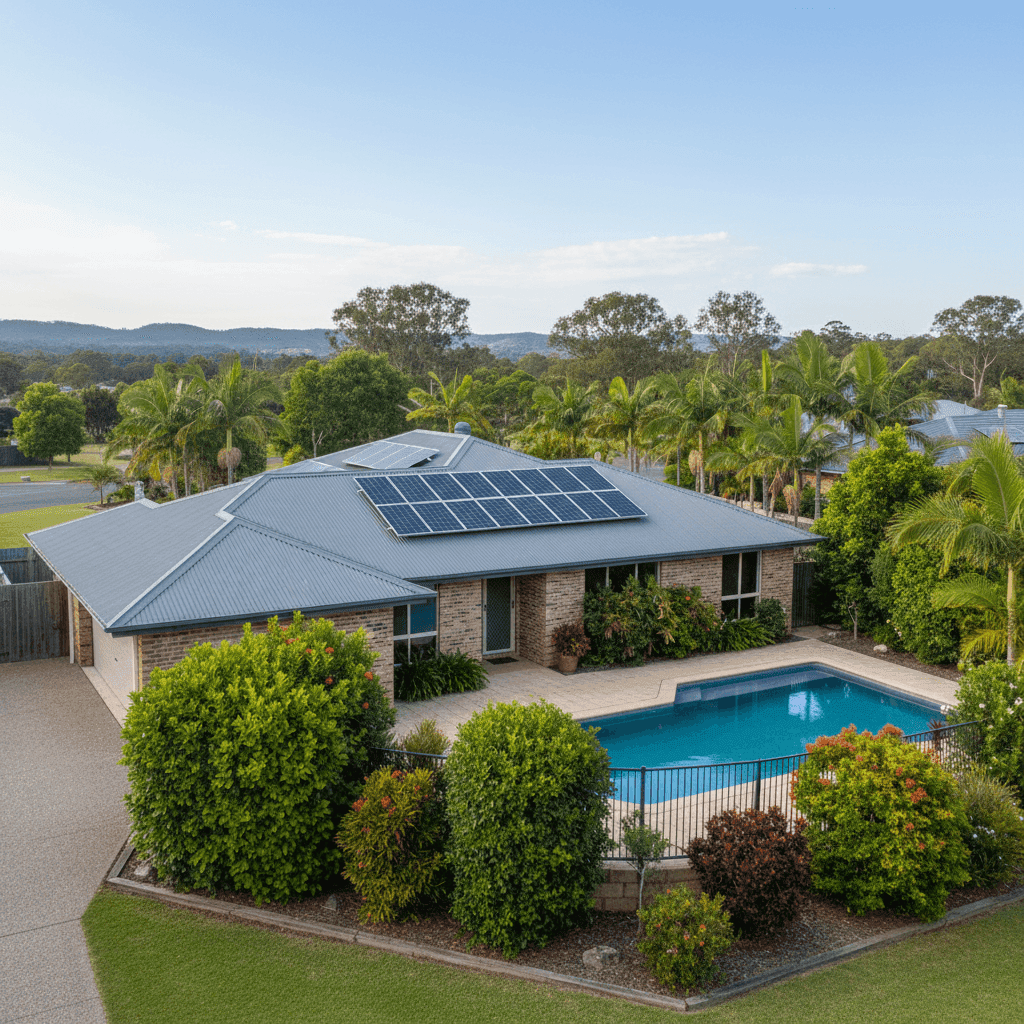

Brick Veneer Walls & Colorbond Roof Brick veneer is one of the more common wall constructions in Australian homes, and insurers generally view it favourably. It offers solid fire resistance and durability. The steel Colorbond roof is similarly well-regarded — it's lightweight, resistant to corrosion, and performs well in high-wind events. Together, these materials typically attract more competitive premiums than timber-framed or fibro-clad homes.

Slab Foundation & Tile Flooring A concrete slab foundation is considered low-risk by most insurers, as it's less susceptible to subsidence and termite damage than pier-and-beam alternatives. Tile flooring throughout also signals durability and ease of replacement, which can work in the policyholder's favour.

Swimming Pool The presence of a pool adds to the overall replacement cost of the property and introduces some additional liability considerations. This will contribute modestly to a higher premium, and it's important to ensure the sum insured accounts for the pool's full reinstatement value.

Solar Panels Solar panels are increasingly common on Australian rooftops, and most home insurance policies cover them as a fixed fixture of the building. However, it's worth confirming with your insurer that the panels are explicitly included under the building sum insured — particularly given their replacement cost can be significant.

Ducted Climate Control Ducted air conditioning systems are a meaningful asset and add to the cost of rebuilding or repairing the home. Ensuring the building sum insured reflects this (and any other built-in systems) is essential to avoid being underinsured.

Construction Year: 1991 At around 34 years old, this home sits in a middle ground — old enough that some wear and maintenance may be a factor, but modern enough to have been built to reasonable construction standards. Insurers may factor in the age of plumbing, electrical systems, and roofing when assessing risk.

No Cyclone Risk Burringbar is not classified as a cyclone risk area, which is a meaningful premium advantage compared to properties in Far North Queensland or parts of Western Australia. This absence of cyclone loading likely contributes to the relatively moderate premium.

---

Tips for Homeowners in Burringbar

1. Review Your Building Sum Insured Carefully At $746,000, the building sum insured needs to cover full reinstatement — not just the market value of the home. Factor in the cost of demolition, debris removal, architect fees, and the replacement of fixed assets like solar panels, the pool, and the ducted air conditioning system. Use a building calculator or speak to a quantity surveyor if you're unsure.

2. Consider Whether a $5,000 Excess Is Right for You A $5,000 excess is on the higher end of the spectrum. While a higher excess typically lowers your premium, it also means you'll be significantly out of pocket if you need to make a claim. If cash flow is a concern, it may be worth requesting quotes with a lower excess to compare the trade-off.

3. Shop Around — The Spread Is Wide With Burringbar premiums ranging from $1,160/yr to $3,994/yr across the market, there's clearly significant variation between insurers. Even if this quote is "fair," comparing multiple policies could reveal a better deal. Get a quote at CoverClub to see how different insurers price your specific property.

4. Check for Flood and Storm Cover The Northern Rivers region has experienced significant flooding in recent years. While Burringbar itself may not be in a high-flood zone, it's worth confirming whether your policy includes flood cover as standard or as an optional extra — and understanding exactly what storm damage scenarios are covered.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy to see how your home insurance quote stacks up against real data from your suburb and beyond. Enter your address at CoverClub to get started and find out if you're getting a genuinely competitive deal on your home and contents insurance.