If you own a free standing home in Burrum Town, QLD 4659, you may be wondering whether your home insurance premium is competitive — or whether you're quietly paying more than you should. This analysis breaks down a real home and contents insurance quote for a three-bedroom property in the area, comparing it against local, state, and national benchmarks to give you a clearer picture of where you stand.

---

Is This Quote Fair?

The quote in question comes in at $2,420 per year (or roughly $232 per month) for combined home and contents cover, with a building sum insured of $459,000 and contents valued at $79,000. Both the building and contents excess are set at $1,000 — a fairly standard arrangement.

Our price rating for this quote is CHEAP — below average, and the data backs that up convincingly. The suburb average for Burrum Town sits at $3,580 per year, meaning this quote is approximately $1,160 cheaper than what most locals are paying. Even the 25th percentile — representing the cheaper end of the market locally — comes in at $3,290 per year, which is still $870 more expensive than this quote.

Put simply, this is a genuinely strong result. Homeowners who receive a quote in this range are in a favourable position compared to their neighbours.

---

How Burrum Town Compares

To put things in broader context, it helps to look at how Burrum Town sits within Queensland and the country as a whole.

| Benchmark | Premium |

|---|---|

| This Quote | $2,420/yr |

| Burrum Town Suburb Average | $3,580/yr |

| Burrum Town Suburb Median | $3,452/yr |

| Fraser Coast LGA Average | $4,810/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, Queensland's state average of $9,129 is extraordinarily high compared to the national average of $5,347 — a reflection of the elevated natural hazard risk across much of the state, particularly in cyclone-prone coastal and far north regions. However, the state median of $3,903 tells a more nuanced story: half of Queensland homeowners are paying under that figure, suggesting a wide spread driven by high-risk outliers.

Burrum Town's suburb average of $3,580 is actually below the QLD median, which indicates the area is considered relatively moderate in risk terms compared to many other Queensland postcodes. The Fraser Coast LGA average of $4,810 is notably higher than the suburb figure, suggesting some neighbouring areas within the LGA carry greater risk weighting.

Nationally, this quote also compares well — sitting below the national median of $2,764 when you consider the level of cover provided (building + contents, $538,000 combined). You can explore Queensland-wide insurance pricing trends and Burrum Town suburb statistics for more context.

---

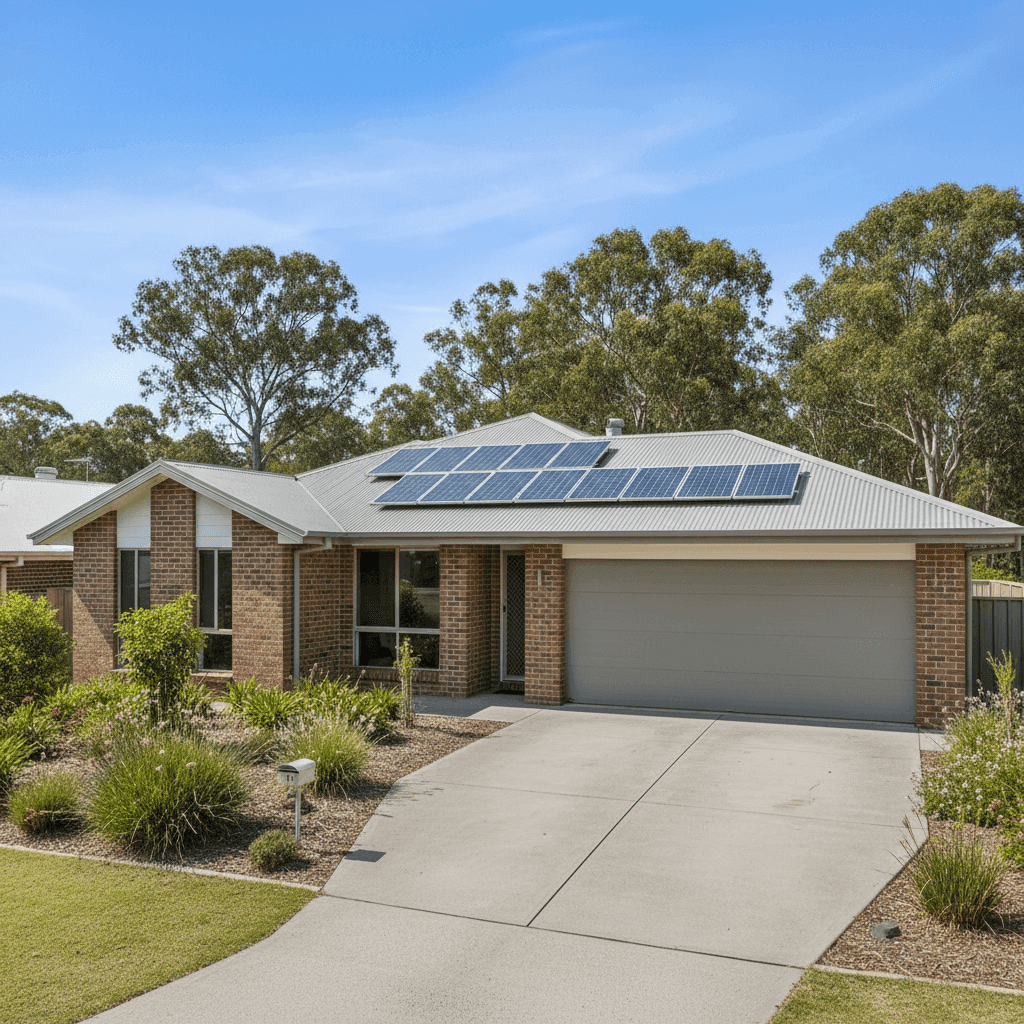

Property Features That Affect Your Premium

Every home insurance quote is shaped by the specific characteristics of the property. Here's how the features of this Burrum Town home likely influence the premium:

Brick Veneer Walls Brick veneer is generally viewed favourably by insurers. It offers solid fire resistance and structural durability, which can contribute to lower premiums compared to weatherboard or lightweight cladding.

Steel / Colorbond Roof A Colorbond roof is another tick in the right column. Metal roofing is durable, resistant to ember attack, and less prone to storm damage than older tile roofs. It's a common and well-regarded choice for Queensland homes.

Concrete Slab Foundation Slab foundations are straightforward for insurers to assess and typically carry no additional loading. There's no underfloor space to worry about, which reduces certain risks associated with moisture and pests.

Solar Panels This property has solar panels installed, which adds some replacement value to the building sum insured. Insurers typically include solar systems under building cover, so it's worth confirming your sum insured accounts for the cost of replacing your system — including inverters and installation.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and is generally covered under building insurance. Again, this is a reason to ensure your building sum insured is set accurately — underinsurance is a real risk when high-value systems like these are factored in.

No Pool, No Cyclone Risk Zone The absence of a pool removes liability and equipment replacement considerations. Importantly, this property is not located in a designated cyclone risk area, which is a meaningful factor in Queensland. Properties in cyclone zones often attract substantially higher premiums, so this is a genuine cost advantage for Burrum Town homeowners.

Built in 1993 A home built in 1993 is at an age where some components — roofing, plumbing, electrical — may be approaching the end of their serviceable life. Insurers may factor this in, though a well-maintained home of this era with modern materials (like Colorbond roofing) can still attract competitive rates.

---

Tips for Homeowners in Burrum Town

1. Review your building sum insured regularly With solar panels and ducted climate control on the property, the cost to rebuild from scratch is higher than a basic home. Use a building calculator to ensure your $459,000 sum insured reflects current construction costs — which have risen significantly in recent years.

2. Don't assume your current insurer is competitive Even if you're currently paying a reasonable premium, the insurance market shifts. Comparing quotes annually — especially at renewal time — can reveal meaningful savings. This quote came in well below the local average, which shows the spread between insurers can be substantial.

3. Consider your excess carefully A $1,000 excess on both building and contents is standard, but raising your excess is one of the most direct ways to reduce your premium. If you have sufficient savings to cover a higher excess in the event of a claim, this trade-off can be worthwhile.

4. Keep records of your contents With $79,000 in contents cover, it's worth maintaining an up-to-date home inventory — photos, receipts, and serial numbers where possible. This makes any future claim significantly smoother and reduces the risk of disputes over item values.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. Get a home insurance quote at CoverClub and see how your premium stacks up against the local market in seconds.