Buxton is a quiet residential locality sitting within the Fraser Coast region of Queensland — an area known for its laid-back lifestyle, proximity to the coast, and the kind of character-filled homes that make it a genuinely appealing place to put down roots. If you own a free-standing home here, you'll know that protecting it with the right building insurance is non-negotiable. But how do you know whether the premium you've been quoted is actually reasonable?

This article breaks down a real building-only insurance quote for a 3-bedroom, 1-bathroom free-standing home in Buxton (postcode 4660), and compares it against local, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $26,734 per year (or $2,562/month) for building-only cover, with a $1,000 building excess and a sum insured of $658,000.

Our price rating for this quote is EXPENSIVE — above average.

To put that into perspective: the average home insurance premium across Buxton sits at just $2,390 per year, and the median is even lower at $2,366 per year. That means this particular quote is more than 10 times the suburb average — a significant gap that warrants a closer look at what's driving the cost.

Even when you factor in the elevated sum insured of $658,000 (which is on the higher end and will naturally push premiums up), the figure is still substantially above what most Buxton homeowners are paying. It's worth shopping around and comparing multiple insurers before committing to this premium.

---

How Buxton Compares

Understanding where Buxton sits relative to broader benchmarks gives useful context when evaluating any quote. Here's a snapshot of the Buxton insurance market based on 23 quotes collected for this postcode:

| Benchmark | Premium |

|---|---|

| Buxton 25th percentile | $1,808/yr |

| Buxton average | $2,390/yr |

| Buxton median | $2,366/yr |

| Buxton 75th percentile | $2,901/yr |

| Fraser Coast LGA average | $4,810/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, Buxton's median premium of $2,366 is actually below the national median of $2,764 — suggesting that, on the whole, Buxton is a relatively affordable suburb to insure. This is somewhat surprising given Queensland's reputation for elevated insurance costs driven by weather-related risks.

Second, Queensland's state average of $9,129 is dramatically higher than its median of $3,903 — a clear sign that a small number of very high-risk or high-value properties are pulling the average upward. This is a common pattern in Queensland, where coastal and flood-prone areas can attract eye-watering premiums.

The Fraser Coast LGA average of $4,810 sits between the suburb and state figures, reflecting the mix of risk profiles across the broader region.

---

Property Features That Affect Your Premium

Every property has its own risk fingerprint, and insurers price premiums accordingly. Several features of this particular home are likely influencing the cost of cover:

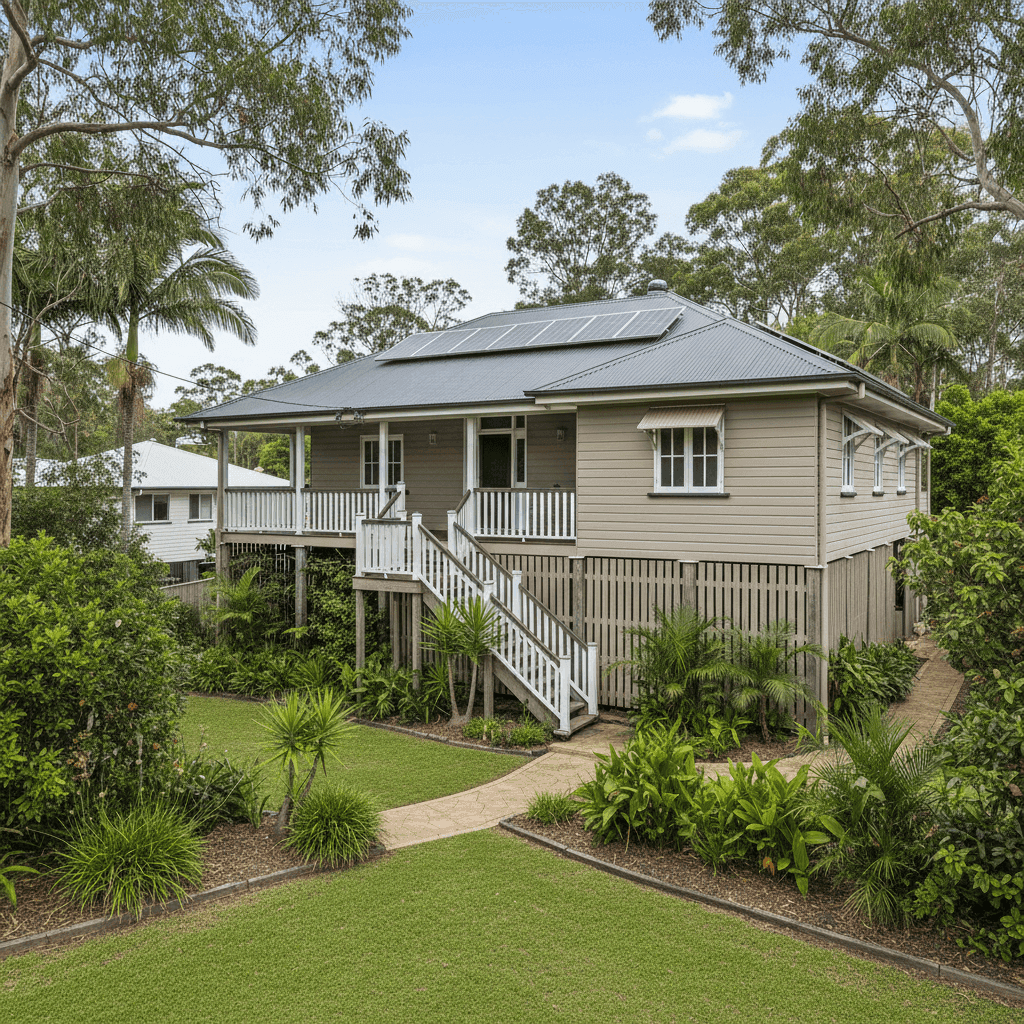

Weatherboard Timber Walls

Weatherboard timber construction is one of the most common building types in older Queensland homes, but it does carry a higher fire risk compared to brick veneer or double brick. Insurers typically apply a loading for timber-framed homes, which can push premiums higher.

Steel/Colorbond Roof

On the positive side, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, resistant to corrosion, and performs well in high-wind events — all of which can help moderate your premium compared to older tile or fibrous cement roofing.

Elevated Foundation (Poles — At Least 1m)

This home is elevated on poles by at least one metre — a classic Queenslander-style design. Elevation can be a double-edged sword for insurance purposes. On one hand, it can reduce flood inundation risk to the main living areas. On the other, elevated homes can be more exposed to wind uplift, and the subfloor space adds complexity to repair assessments.

Construction Year: 1985

At roughly 40 years old, this home sits in a bracket where insurers may apply age-related loadings. Older homes can have ageing electrical systems, plumbing, and structural elements that increase the likelihood of a claim.

Solar Panels

Solar panels are an insurable asset that add replacement value to a property. Most building policies cover panels as part of the structure, but their presence does contribute to the overall sum insured — and by extension, the premium.

Ducted Climate Control

Ducted air conditioning systems are a significant fixed installation and are typically covered under building insurance. Like solar panels, they add to the replacement cost of the home and can influence the sum insured calculation.

Timber/Laminate Flooring

Timber flooring, while beautiful, can be costly to repair or replace following water damage or impact events. This is another factor that may contribute to a higher sum insured and, consequently, a higher premium.

---

Tips for Homeowners in Buxton

If you're looking to get better value on your building insurance, here are four practical steps worth considering:

- Review your sum insured carefully. A sum insured of $658,000 for a 160 sqm home may be higher than necessary depending on local construction costs. Use a building cost calculator to verify the rebuild cost — over-insuring is a common and costly mistake.

- Compare multiple insurers. The gap between the cheapest and most expensive quotes in any suburb can be enormous. Get a quote through CoverClub to see how different insurers price your specific property.

- Ask about discounts for home improvements. If you've recently updated your electrical system, plumbing, or roof, let your insurer know. Some providers offer premium reductions for homes with modernised infrastructure.

- Consider your excess level. Opting for a higher voluntary excess can meaningfully reduce your annual premium. If you have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim, this trade-off can make sense over the long term.

---

Ready to Find a Better Deal?

Whether you're renewing your policy or buying cover for the first time, comparing quotes is the single most effective way to avoid overpaying. CoverClub makes it easy to see what multiple insurers would charge for your Buxton home — all in one place.

Compare home insurance quotes for your property today →

You can also explore detailed insurance pricing data for Buxton and postcode 4660, the broader Queensland market, or national benchmarks to see how your area stacks up.