If you own a four-bedroom free standing home in Byford, WA 6122, you've probably wondered whether you're getting a fair deal on your home and contents insurance. Byford is a fast-growing suburb in the City of Serpentine-Jarrahdale, about 40 kilometres south-east of Perth's CBD. With new estates continuing to expand and property values rising, making sure your home is properly covered — at the right price — has never been more important.

This article breaks down a real home and contents insurance quote for a double brick, tile-roofed home in Byford, compares it against local, state and national benchmarks, and offers practical tips to help you get better value on your premium.

---

Is This Quote Fair?

The quote in question comes in at $1,806 per year (or $173/month) for combined home and contents cover, with a building sum insured of $633,000 and contents valued at $70,000. Both the building and contents excess are set at $1,000.

Based on CoverClub's pricing data, this quote is rated Expensive — above average for the Byford area.

To put that in perspective: the average home and contents premium among the 49 quotes collected for Byford sits at $1,406 per year, while the suburb median is a lower $1,281/yr. This quote lands about $400 above the suburb average and roughly $525 above the median — a meaningful gap that's worth investigating before you renew.

That said, "expensive" doesn't automatically mean "wrong." A higher sum insured, quality fittings, and specific property features can all legitimately push a premium upward. The key is understanding why you're paying more — and whether there's room to reduce the cost without sacrificing the cover you need.

---

How Byford Compares

One of the most useful ways to evaluate any insurance quote is to zoom out and look at the broader picture. Here's how Byford stacks up:

| Benchmark | Annual Premium |

|---|---|

| This quote | $1,806 |

| Byford suburb average | $1,406 |

| Byford suburb median | $1,281 |

| Byford 25th percentile | $829 |

| Byford 75th percentile | $1,773 |

| LGA (Serpentine-Jarrahdale) average | $1,448 |

| WA state average | $2,811 |

| WA state median | $2,127 |

| National average | $5,347 |

| National median | $2,764 |

A few things stand out here. First, this quote sits just above the 75th percentile for Byford ($1,773/yr), meaning it's more expensive than roughly three-quarters of comparable quotes in the suburb. That's a signal worth paying attention to.

Second — and this is genuinely good news — Byford is a relatively affordable place to insure a home compared to the rest of Western Australia and the country as a whole. The WA state average of $2,811/yr is more than 55% higher than this quote, and the national average of $5,347/yr is nearly three times higher. Much of that national figure is driven by high-risk areas in Queensland and northern Australia, but the comparison still highlights that Perth's southern suburbs enjoy relatively moderate insurance costs.

You can explore more localised data on the Byford suburb stats page.

---

Property Features That Affect Your Premium

Every property is different, and insurers weigh up a range of factors when calculating your premium. Here's how this home's specific characteristics likely influence the quote:

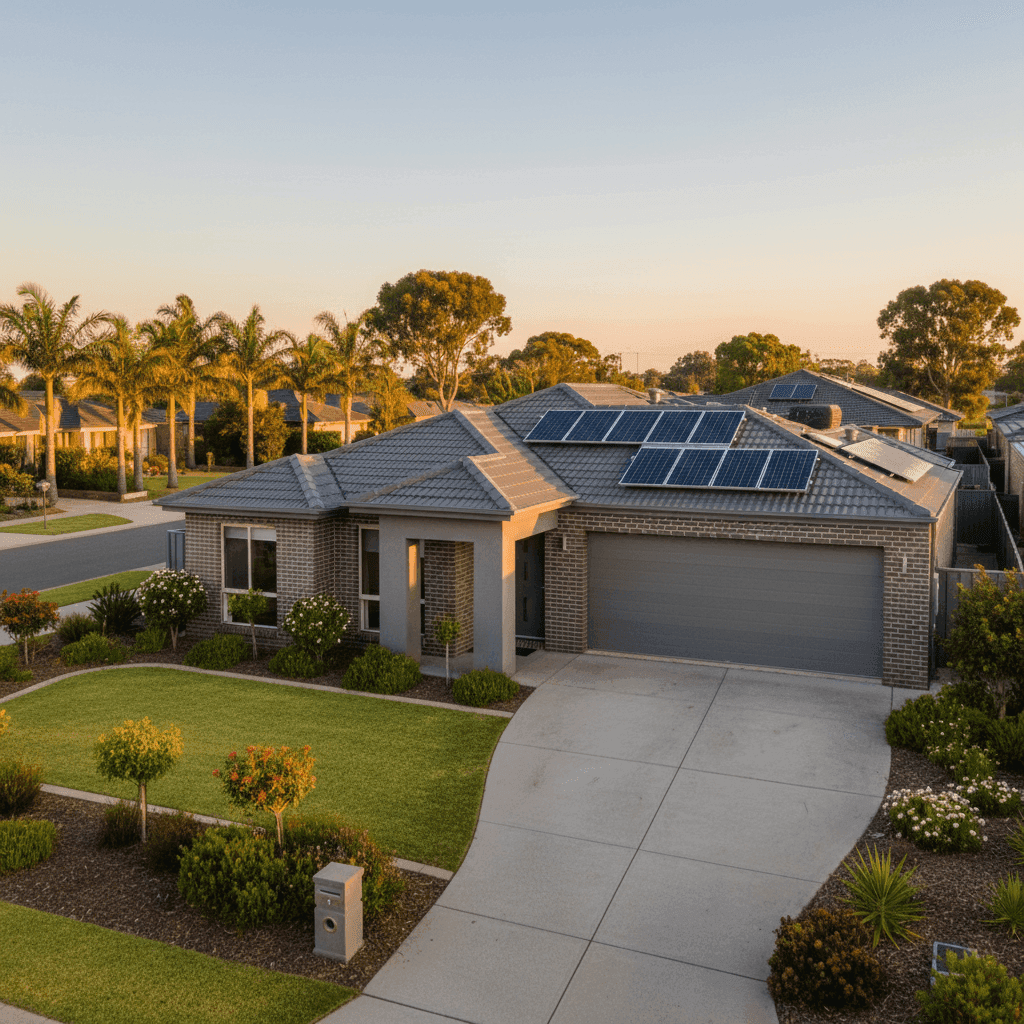

Double Brick Construction Double brick is generally favoured by insurers in WA — it's durable, fire-resistant and performs well in storms. Homes built with double brick often attract lower premiums than those with lightweight cladding or timber frames, so this works in the homeowner's favour.

Tiled Roof Terracotta or concrete tiles are considered a solid roofing choice. They're less susceptible to fire than some alternatives and tend to hold up well in moderate weather events. This is another feature that typically keeps premiums in check.

Slab Foundation & Vinyl Flooring A concrete slab foundation is standard in WA and doesn't add significant risk from an insurer's perspective. Vinyl flooring is practical and relatively inexpensive to replace, which may help moderate the contents and building replacement cost.

Built in 2016 Newer homes (post-2010 in particular) benefit from modern building codes, which mandate improved structural standards and energy efficiency. A 2016 build is recent enough that major structural issues are unlikely, which insurers view positively.

Solar Panels Solar panels add value to a home but also add complexity to an insurance policy. They can be damaged by hail, storms or falling debris, and their replacement cost needs to be factored into the building sum insured. It's worth confirming your policy explicitly covers solar panel damage and that your $633,000 sum insured accounts for their full replacement value.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset. Like solar panels, they should be included in your building sum insured. If this system needs full replacement, costs can run into the tens of thousands — so it's important this is reflected accurately.

No Pool, No Cyclone Risk The absence of a pool removes a common liability risk, and Byford falls outside designated cyclone risk zones — both factors that help keep premiums lower than properties in northern WA.

---

Tips for Homeowners in Byford

1. Review Your Sum Insured Annually With construction costs rising across WA, the cost to rebuild your home may have increased since you last updated your policy. A building sum insured of $633,000 for a 214 sqm double brick home is reasonable, but it's worth cross-checking against current builder rates (typically $2,500–$3,500/sqm for quality builds in Perth's outer suburbs) to ensure you're not underinsured.

2. Shop Around at Renewal Time This quote sits above the 75th percentile for Byford — which means there's a real chance you could find comparable cover for less. Don't let your policy auto-renew without comparing at least two or three alternatives. Get a new quote at CoverClub to see what's available for your address.

3. Consider Adjusting Your Excess Opting for a higher excess (say, $1,500 or $2,000 instead of $1,000) can meaningfully reduce your annual premium. If you have a financial buffer to cover a larger out-of-pocket cost in the event of a claim, this can be a smart trade-off — particularly for a newer, lower-risk home like this one.

4. Confirm Solar Panel and Ducted AC Coverage Before your next renewal, call your insurer and confirm that your solar panels and ducted climate control system are explicitly covered under your building policy — and that their replacement value is captured in your sum insured. These are easy items to overlook but expensive to replace without cover.

---

Compare and Save with CoverClub

Whether you're renewing your existing policy or shopping for cover on a new purchase, CoverClub makes it easy to see how your premium stacks up and find better value. With real data from thousands of Australian homeowners, you can get a quote tailored to your property and compare it against what others in your suburb are paying. Don't pay more than you need to — start comparing today.