Caboolture, sitting in the heart of the Moreton Bay region north of Brisbane, is a well-established suburb popular with families seeking space and value. For owners of a four-bedroom, free-standing home in postcode 4510, understanding what you should be paying for building insurance — and why — can make a real difference to your household budget. This article breaks down a recent building-only quote of $2,364 per year for a property in Caboolture and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: yes, broadly speaking. This quote has been rated Fair (Around Average), which means it sits comfortably within the typical range for the suburb — neither a standout bargain nor an overpriced outlier.

At $2,364 annually (or $211 per month), the premium comes in below the Caboolture suburb average of $2,515/yr and below the suburb median of $2,548/yr. That's a meaningful saving compared to what many neighbours are paying. It also sits within the interquartile range for the area — the middle 50% of quotes in Caboolture fall between $1,797/yr and $3,291/yr — so this figure is well within normal territory.

It's worth noting that the building excess on this policy is $5,000, which is relatively high. A higher excess typically reduces the annual premium, so part of the reason this quote looks competitive may be because the policyholder is absorbing more out-of-pocket risk in the event of a claim. Always weigh up the excess against your ability to cover that cost if something goes wrong.

---

How Caboolture Compares

To appreciate whether this quote represents good value, it helps to zoom out and look at the broader picture. You can explore the full data on the Caboolture suburb stats page, the Queensland state overview, or the national insurance stats.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Caboolture (4510) | $2,515/yr | $2,548/yr |

| Moreton Bay LGA | $3,435/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. Queensland's average premium of $9,129/yr is extraordinarily high compared to both the national average and the Caboolture suburb average. This is largely driven by high-risk coastal and cyclone-prone areas in Far North Queensland, which pull the state average upward significantly. The median of $3,903/yr is a more representative figure for typical Queensland homeowners.

Caboolture, by contrast, is not classified as a cyclone risk area — a major factor that keeps premiums more manageable in this part of South East Queensland. The suburb's average of $2,515/yr is also notably lower than the broader Moreton Bay LGA average of $3,435/yr, suggesting Caboolture is relatively affordable within its own region.

Compared to the national median of $2,764/yr, this quote of $2,364/yr is actually below the national midpoint, which is a positive sign for the policyholder.

---

Property Features That Affect Your Premium

Every property is different, and insurers assess a range of physical characteristics when calculating your premium. Here's how the key features of this particular home are likely influencing the cost:

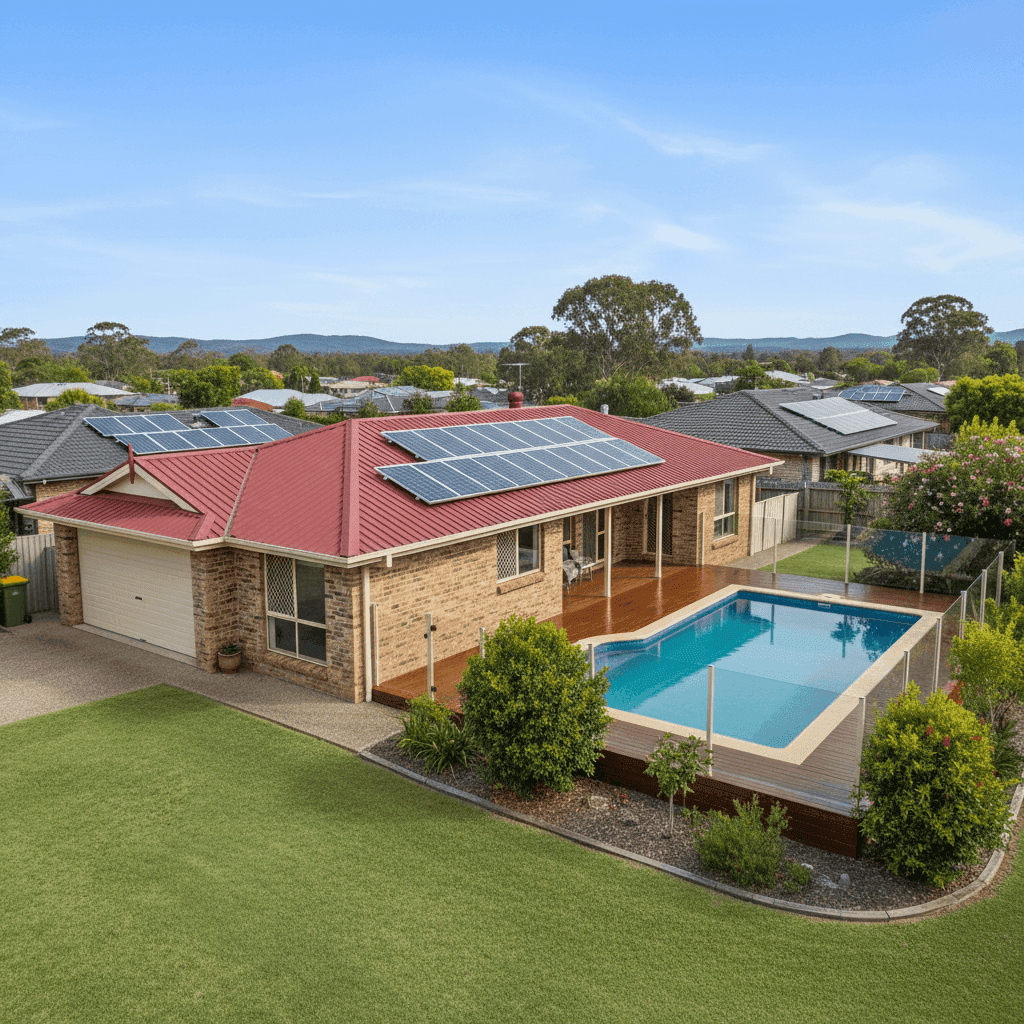

Brick Veneer Walls & Colorbond Roof Brick veneer is one of the most common and well-regarded construction types in Australia. It offers solid fire resistance and durability, which insurers generally view favourably. The steel Colorbond roof is similarly regarded as a strong performer — it's resistant to ember attack, doesn't rot or crack, and handles the Queensland heat well. Together, these materials typically attract more competitive premiums than timber-framed or fibro construction.

Slab Foundation A concrete slab foundation is standard for homes built in this era and region. It's structurally sound and reduces the risk of subsidence-related claims, which is a plus from an underwriting perspective.

Timber & Laminate Flooring While attractive and popular, timber and laminate flooring can be more costly to repair or replace than tiles in the event of water damage or flooding. This is a minor factor but worth keeping in mind when reviewing your sum insured.

Swimming Pool A pool adds both value and liability to a property. Insurers factor in the increased replacement cost and the potential for water-related damage to surrounding structures. If your policy includes pool cover, make sure the sum insured of $750,000 adequately accounts for the pool and associated infrastructure.

Solar Panels Solar panels are increasingly common on Queensland rooftops, but they do add to the rebuild cost of a home. Ensure your sum insured reflects the replacement value of your solar system — a standard 6.6kW system can cost $5,000–$10,000 to replace, and larger systems even more.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and should be factored into your building sum insured. Systems can cost $10,000–$20,000 or more to replace, and they're often underestimated in building valuations.

Above-Average Fittings With above-average fittings quality across a 244 sqm home with four bedrooms and two bathrooms, the cost to rebuild this property to its current standard would be higher than a comparable home with standard finishes. This is appropriately reflected in the $750,000 sum insured.

---

Tips for Homeowners in Caboolture

1. Review your sum insured regularly Construction costs have risen sharply across Australia over the past few years. A sum insured that was accurate in 2021 or 2022 may no longer reflect the true cost to rebuild your home today. With solar panels, ducted air conditioning, a pool, and above-average fittings, this property has multiple high-value components that should be reassessed annually.

2. Understand your excess before you commit A $5,000 building excess is on the higher end. While it reduces your premium, it means you'll need to cover that amount yourself before your insurer pays out on any building claim. Make sure this is financially manageable for your household, particularly for smaller claims like storm damage to the roof.

3. Check for flood and storm cover Caboolture and the broader Moreton Bay region can be affected by heavy rainfall and localised flooding. Confirm whether your policy includes flood cover as standard or as an optional add-on — and if it's excluded, consider whether that's a risk you're comfortable carrying.

4. Compare quotes at renewal time Insurance loyalty doesn't always pay. Premiums can shift significantly from year to year, and different insurers assess risk differently. Using a comparison tool at renewal ensures you're not overpaying simply out of habit.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for cover on a new property, comparing quotes is the smartest first step. Get a home insurance quote at CoverClub and see how your premium stacks up against what others in Caboolture and across Queensland are paying. It takes just a few minutes and could save you hundreds.