If you own a free standing home in Caboolture South, QLD 4510, you've probably wondered whether you're paying a fair price for home insurance — or leaving money on the table. This article breaks down a real home and contents insurance quote for a three-bedroom property in the suburb, and puts the numbers in context against local, state-wide, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $1,663 per year (or $169/month) for combined home and contents cover, with a building sum insured of $450,000 and contents valued at $20,000. The building excess is set at $3,000 and the contents excess at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Based on 80 quotes collected for Caboolture South, the suburb's median premium sits at $1,671/year — meaning this quote is essentially right on the median. The suburb average is slightly higher at $1,797/year, suggesting a small number of higher-priced quotes are pulling the mean upward.

In practical terms, this homeowner is paying less than the average Caboolture South resident while sitting squarely in the middle of the pack. It's not a bargain-basement price, but it's certainly not inflated either. For a property of this size and age, a "fair" rating is a reasonable outcome — though there's always room to explore whether a better deal exists.

---

How Caboolture South Compares

One of the most striking things about this quote is just how affordable Caboolture South is relative to the broader Queensland market.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Caboolture South (suburb) | $1,797/yr | $1,671/yr |

| Moreton Bay LGA | $3,435/yr | — |

| Queensland (state) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The Queensland state average of $9,129/year is heavily skewed by high-risk areas — think cyclone-prone Far North Queensland, flood-affected river towns, and coastal communities exposed to extreme weather. When you look at the state median of $3,903/year, the picture is more balanced, but Caboolture South still comes in well below it.

Compared to the national median of $2,764/year, this quote of $1,663 is about 40% cheaper — a meaningful difference that reflects the suburb's relatively low natural hazard exposure. Caboolture South sits in the Moreton Bay region, which, while not immune to severe weather, doesn't face the same cyclone and flood risk that drives premiums sky-high in other parts of Queensland.

The Moreton Bay LGA average of $3,435/year is also worth noting — it's nearly double this quote, suggesting that pockets of the region carry significantly higher risk profiles. Caboolture South, it seems, is one of the more insurer-friendly postcodes in the area.

---

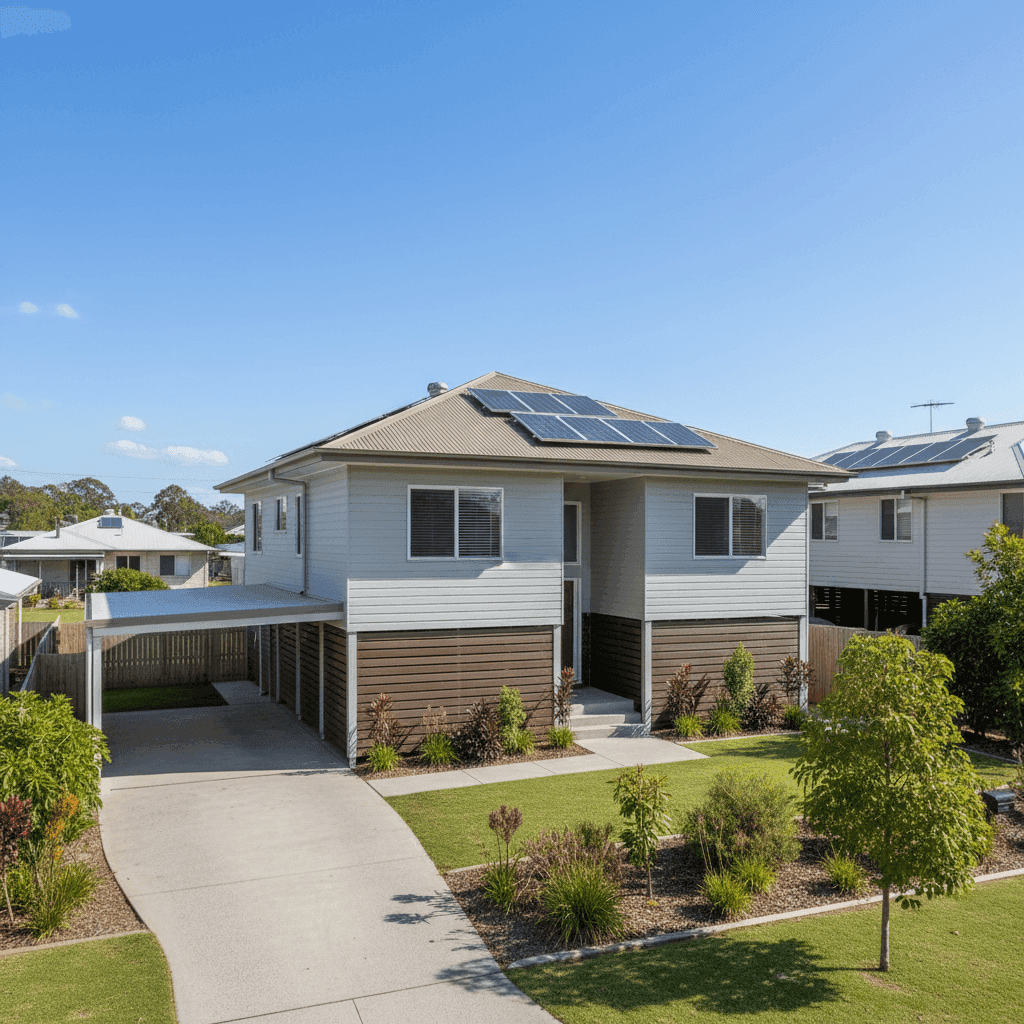

Property Features That Affect Your Premium

Several characteristics of this particular property will be influencing the premium, both positively and negatively.

Hardiplank/Hardiflex external walls are a strong positive. Fibre cement cladding is fire-resistant, durable, and holds up well against the elements — insurers generally view it favourably compared to older timber weatherboard or brick veneer construction.

Steel/Colorbond roofing is another tick in the right column. Colorbond is one of the most popular roofing materials in Queensland for good reason — it's lightweight, resistant to corrosion, and performs well in high-wind events. Insurers tend to price it more competitively than terracotta or concrete tiles, which can crack or dislodge in storms.

Slab foundation is standard for the era (built in 1993) and generally considered a neutral to positive factor. It's a known quantity for insurers, with fewer concerns about subfloor moisture or pest damage compared to older raised timber stumps.

Elevated by at least 1 metre is a notable feature. In Queensland, elevation is often associated with flood resilience — a raised home allows floodwater to pass beneath the structure rather than inundating the living areas. This can be a meaningful premium reducer in areas with any flood history.

Solar panels are worth a mention. While they add value to the property, they also add replacement cost in the event of a claim — hail, storm, or fire damage to solar systems can be expensive to repair. It's worth confirming your policy explicitly covers solar panels as part of the building sum insured.

Timber and laminate flooring can be a cost consideration in claims — water damage to timber floors is expensive to remediate — but it's unlikely to be a major premium driver on its own.

---

Tips for Homeowners in Caboolture South

1. Review your building sum insured regularly A $450,000 sum insured for a 214 sqm home in Caboolture South seems reasonable, but construction costs have risen sharply in recent years. Make sure your sum insured reflects what it would actually cost to rebuild your home from scratch — not its market value. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm solar panel coverage As mentioned above, solar panels should be explicitly included in your building cover. Check your policy documents to confirm whether the system is covered for storm, hail, and fire damage, and whether the sum insured is adequate to replace the full system.

3. Consider whether your contents value is sufficient A $20,000 contents sum insured is on the lower end for a three-bedroom home. Do a quick audit of your furniture, appliances, clothing, electronics, and valuables — you may find the total replacement cost is higher than you'd expect. Being underinsured on contents can leave you significantly out of pocket after a claim.

4. Compare quotes at renewal time A "fair" rating means you're around average — but average isn't necessarily the best available. Insurers price risk differently, and switching at renewal (or even mid-term in some cases) can yield meaningful savings. Use a comparison tool to see what else is on the market before automatically renewing.

---

Ready to Compare?

Whether you're happy with your current quote or curious whether you could pay less, it pays to compare. At CoverClub, you can get a home insurance quote in minutes and see how your premium stacks up against real data from your suburb and beyond. Don't just accept the first number you're given — the right cover at the right price is out there.