If you own a four-bedroom free standing home in Cairns North, QLD 4870, you already know that insuring it comes with a few more moving parts than the average Australian property. Cyclone exposure, elevated construction, ageing building stock, and the unique character of tropical Queensland homes all play a role in how insurers price your risk. This article breaks down a real home and contents insurance quote for a property in this suburb, compares it against local, state, and national benchmarks, and offers practical guidance for homeowners looking to make the most of their cover.

---

Is This Quote Fair?

The quote in question sits at $4,878 per year (or $478/month) for combined home and contents insurance, covering a building sum insured of $820,000 and $18,000 in contents. The building excess is $2,000 and the contents excess $1,000.

Our price rating for this quote is CHEAP — below the suburb average — and the data backs that up clearly.

The suburb average premium for Cairns North sits at $10,350 per year, with a median of $9,213. This quote comes in at less than half the suburb average — a significant saving by any measure. Even the cheapest quarter of quotes in the area (the 25th percentile) averages $7,378 per year, meaning this premium is well below what most Cairns North homeowners are paying.

Compared to the QLD state average of $4,547/yr, this quote is broadly in line — actually sitting just slightly above the state figure, which is expected given the elevated cyclone risk in far north Queensland. Against the national average of $2,965/yr, it is notably higher, but that gap reflects the genuine risk differential between coastal tropical Queensland and the broader Australian market.

In short: for a property of this size, age, and location, this is a competitive premium. Homeowners in Cairns North who are paying closer to the suburb average of $10,350 should seriously consider whether their current insurer is giving them fair value.

---

How Cairns North Compares

The pricing gap between Cairns North and the rest of Australia is stark, and it is worth understanding why.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $4,878 |

| Cairns North Suburb Average | $10,350 |

| Cairns North Suburb Median | $9,213 |

| Cairns North 25th Percentile | $7,378 |

| Cairns North 75th Percentile | $14,330 |

| LGA (Cairns) Average | $12,404 |

| QLD State Average | $4,547 |

| QLD State Median | $3,931 |

| National Average | $2,965 |

| National Median | $2,716 |

(Based on 18 quotes sampled for the Cairns North suburb.)

The Cairns LGA average of $12,404 is among the highest in Queensland, driven largely by cyclone risk, storm surge exposure, and the high cost of rebuilding in a regional area where labour and materials carry a premium. The spread between the 25th and 75th percentiles — $7,378 to $14,330 — tells you just how much variation there is between insurers for the same suburb. That range alone is a compelling reason to compare quotes rather than simply renewing with your existing provider.

You can explore the full pricing data for this suburb at the Cairns North stats page, or browse QLD-wide insurance trends for broader context.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on how insurers assess and price the risk.

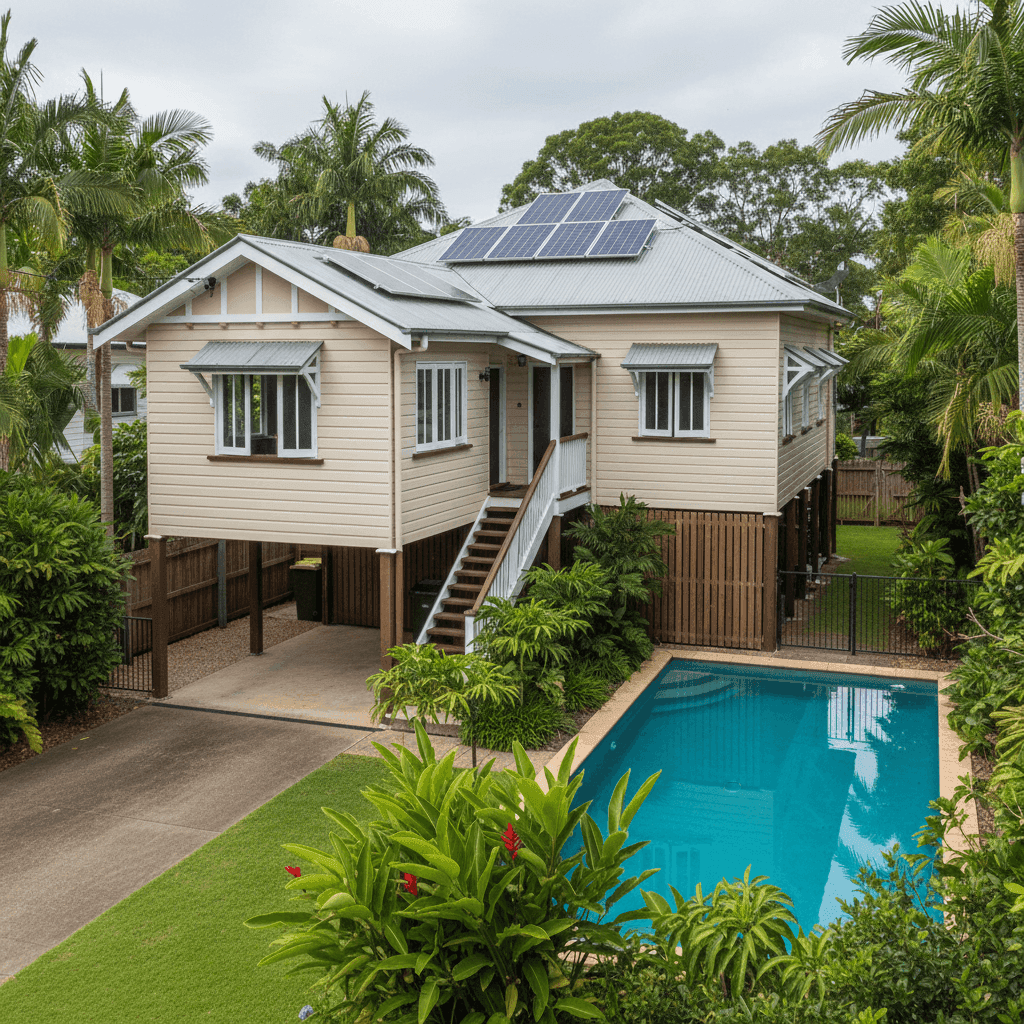

Age and Construction (Built 1960, Weatherboard Timber)

At over 60 years old, this home predates modern building codes and cyclone-resistant construction standards. Weatherboard timber walls, while charming and common in tropical Queensland, are considered higher risk than brick or rendered masonry — they are more susceptible to wind damage and moisture ingress. Older wiring, plumbing, and roofing components can also increase the likelihood of a claim.

Elevated Foundation

Being elevated by at least one metre is actually a significant protective factor in this region. Elevated homes — often referred to as Queenslanders — are less vulnerable to flood inundation and storm surge, which can meaningfully reduce premiums compared to slab-on-ground homes in flood-prone areas. This feature likely contributes to the competitive pricing of this quote.

Steel/Colorbond Roof

Colorbond roofing performs well in cyclonic conditions relative to older materials like terracotta tiles or fibrous cement sheeting. It is less likely to become airborne projectile debris in high winds, which insurers view favourably.

Cyclone Risk Area

Cairns sits squarely within Australia's cyclone belt. Insurers apply a cyclone loading to premiums in this region, and many policies include a separate cyclone excess. This is the single biggest driver of the gap between Cairns North premiums and the national average.

Pool, Solar Panels, and Ducted Climate Control

These three features add to the overall replacement value of the property and its contents, and each carries its own risk profile. Swimming pools can be a liability and may require specific cover. Solar panel systems — particularly inverters and panels themselves — can be damaged in storms or hail events. Ducted air conditioning systems are expensive to repair or replace and are a common claim item after cyclone events.

Building Size and Sum Insured

At 214 sqm and a building sum insured of $820,000, this is a substantial property. The sum insured reflects not just the size of the home but the cost of rebuilding in a regional area — labour and materials in far north Queensland carry a significant premium over metropolitan centres.

---

Tips for Homeowners in Cairns North

1. Review your sum insured annually. Construction costs have risen sharply in recent years, and regional Queensland has been hit harder than most. If your building sum insured hasn't been updated recently, you may be underinsured — meaning you'd face a shortfall in the event of a total loss. Use a building replacement cost calculator or ask your insurer to review the figure.

2. Understand your cyclone excess. Many policies in cyclone-prone areas carry a separate, higher excess for cyclone-related claims — sometimes 1–2% of the sum insured. On an $820,000 home, that could mean an out-of-pocket expense of $8,200–$16,400 before your insurer pays anything. Make sure you know what your policy says before cyclone season arrives.

3. Maintain your home proactively. Insurers can and do reduce or deny claims where damage is attributable to lack of maintenance. In a tropical climate, this means regularly inspecting your roof, gutters, and external walls for signs of rust, rot, or deterioration — particularly before the wet season. Keeping records of maintenance work is also worthwhile.

4. Compare quotes every year — don't just auto-renew. The spread of premiums in Cairns North is enormous. The difference between the cheapest and most expensive quotes in this suburb can exceed $7,000 per year for similar properties. Loyalty rarely pays in home insurance; comparing the market annually is one of the most effective ways to keep your costs down.

---

Ready to Compare?

Whether you're renewing soon or simply curious about what you should be paying, CoverClub makes it easy to see how your current premium stacks up. Get a home insurance quote at CoverClub and find out if you could be paying less — without sacrificing the cover you need.