Calderwood is one of the Illawarra region's newer residential growth corridors, sitting within the Kiama local government area just inland from the South Coast. As master-planned estates continue to attract families and first-home buyers to the area, understanding the true cost of home insurance in Calderwood has never been more important. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom free-standing home in the suburb — and helps you decide whether the price stacks up.

---

Is This Quote Fair?

The quote in question comes in at $3,902 per year (or $374 per month) for combined home and contents cover, with a building sum insured of $900,000 and contents valued at $200,000. Both the building and contents excesses are set at $2,000.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up.

The suburb average for Calderwood sits at just $1,000 per year, with a median of $805. That means this quote is roughly 3.9 times the local average and nearly five times the suburb median. Even accounting for the higher-than-typical sum insured ($900,000 for the building alone), that's a significant premium to be paying relative to neighbours in the same postcode.

That said, it's worth zooming out. Compared to the NSW state average of $9,528 per year, this quote is actually well below what many homeowners across the state are paying. The NSW median sits at $3,770 — so at $3,902, this quote is only marginally above the state midpoint. At the national level, the average is $5,347 and the median is $2,764, placing this quote above the national median but below the national average.

The takeaway? This quote is expensive relative to Calderwood specifically, but not outrageous in the broader NSW or national context — particularly given the property's features and the level of cover being sought.

---

How Calderwood Compares

Here's a snapshot of how this quote sits across different benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Calderwood (postcode 2527) | $1,000/yr | $805/yr |

| Kiama LGA | $3,332/yr | — |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| This Quote | $3,902/yr | — |

Calderwood's suburb-level premiums are notably low compared to the rest of the Kiama LGA ($3,332 average) and the state. This likely reflects the area's newer housing stock, lower claims history, and reduced exposure to some of the coastal and bushfire risks that push up premiums elsewhere in the region. However, individual quotes — especially those with high sums insured and premium property features — can diverge significantly from the suburb average.

It's also worth noting that the suburb sample size of 25 quotes is relatively small, which means the local averages may not fully capture the range of premiums in the area.

---

Property Features That Affect Your Premium

This particular property has several characteristics that insurers weigh carefully when calculating risk and replacement cost.

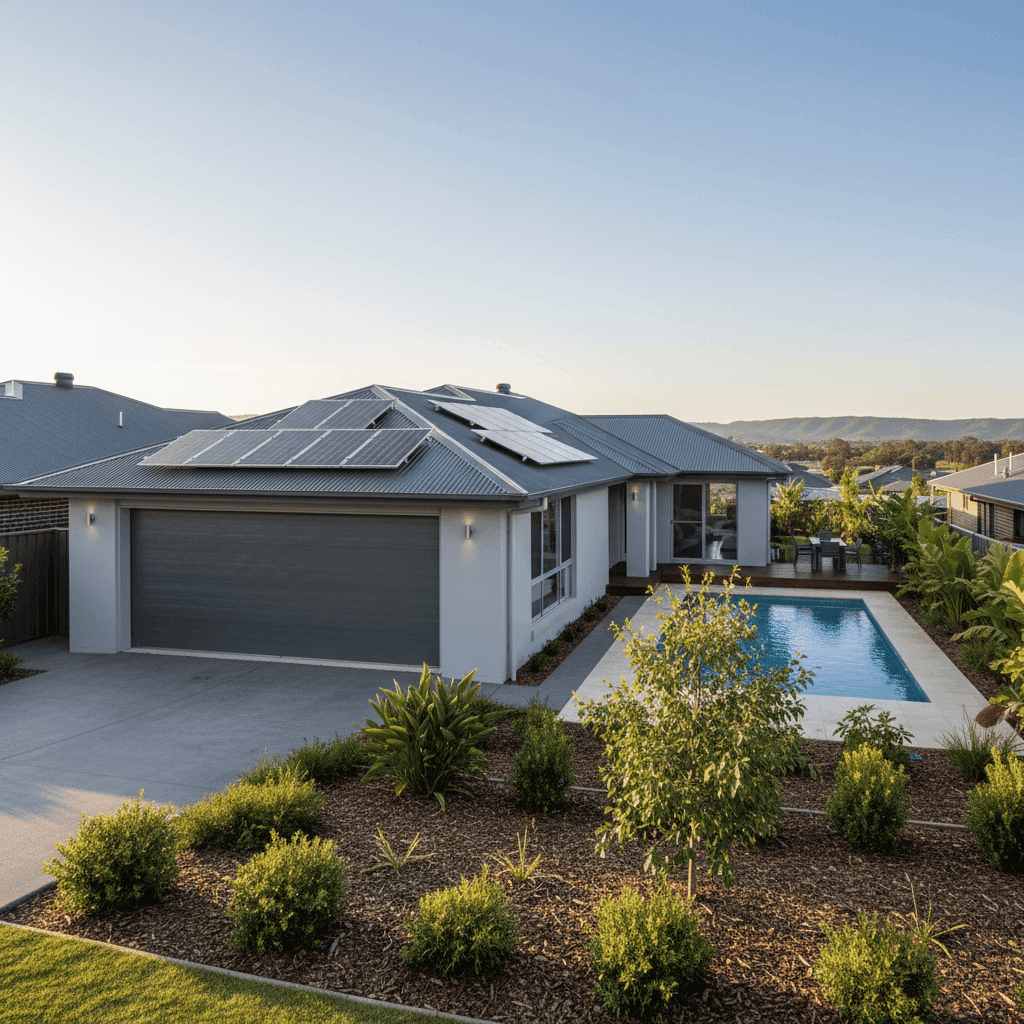

Newly built construction (2026): Brand-new homes generally attract favourable treatment from insurers — modern building codes mean better structural integrity, fire resistance, and safety standards. However, a 2026 build also signals a higher replacement cost, which is reflected in the $900,000 sum insured.

Hardiplank/Hardiflex external walls: Fibre cement cladding like Hardiplank is considered a relatively low-risk external wall material. It's non-combustible, resistant to rot and termites, and durable in coastal and humid environments — all of which can work in your favour at renewal time.

Steel/Colorbond roof: Colorbond is one of the most common and well-regarded roofing materials in Australia. It's lightweight, durable, and performs well in high-wind and storm conditions. Insurers generally view it positively compared to older materials like terracotta tiles.

Concrete slab foundation: Slab foundations are standard for newer builds and present minimal additional risk from an insurance perspective. They're less susceptible to subsidence issues than older pier-and-beam constructions.

Timber/laminate flooring: While aesthetically desirable, timber and laminate floors carry a higher replacement cost than concrete or vinyl alternatives. This can push up the contents and building valuation slightly.

Above-average fittings: Kitchens, bathrooms, and fixtures rated above average command higher rebuild and replacement costs. This is one of the more significant drivers of a higher sum insured — and therefore a higher premium.

Swimming pool: Pools add both value and liability to a property. From an insurance perspective, they increase the cost of a full rebuild and may attract additional public liability considerations.

Solar panels: Rooftop solar systems are increasingly common but not always well covered under standard policies. They add to the overall insured value and can be expensive to replace after storm or hail damage.

Ducted climate control: Ducted air conditioning systems are costly to repair or replace, contributing to a higher building sum insured.

---

Tips for Homeowners in Calderwood

1. Review your sum insured annually With a $900,000 building sum insured on a newly built home, it's essential to ensure this figure keeps pace with construction cost inflation. Building costs have risen sharply in recent years, and being underinsured can leave you significantly out of pocket after a major claim. Use a professional building cost estimator or ask your insurer about index-linked cover.

2. Confirm your solar panels and pool are explicitly covered Not all home insurance policies automatically cover solar panel systems or swimming pools under the standard building definition. Read your Product Disclosure Statement carefully and ask your insurer to confirm these are included — and to what limit.

3. Shop around before renewal The gap between the cheapest and most expensive quotes in Calderwood is substantial. Even if you're happy with your current insurer, comparing quotes at renewal could save you hundreds of dollars. Use CoverClub to compare quotes across multiple providers in minutes.

4. Consider your excess level Both the building and contents excesses on this quote are set at $2,000. Opting for a higher excess can reduce your annual premium meaningfully — but make sure the amount is something you could comfortably cover in the event of a claim. Strike a balance that suits your financial position.

---

Ready to Find a Better Rate?

Whether you're insuring a new build or an established home in Calderwood, it pays to compare. Premiums vary widely between insurers — even for properties with identical features — and the difference can easily run into the hundreds of dollars each year. Head to CoverClub to get a personalised quote and see how your current cover stacks up against the market.