If you own a free standing home in Caloundra West, QLD 4551, you're living in one of the Sunshine Coast's most established and family-friendly suburbs. Like any homeowner, you've probably wondered whether your home insurance premium is competitive — or whether you're quietly paying more than you need to. This article breaks down a real home and contents insurance quote for a four-bedroom property in the area, benchmarks it against local, state, and national data, and offers practical tips to help you get the best value on cover.

---

Is This Quote Fair?

The quote in question comes to $2,947 per year (or $284/month) for combined home and contents insurance, with a $695,000 building sum insured and $50,000 in contents cover. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as FAIR — around average for the area. That's a reasonable result, but it's worth unpacking what "average" actually means in context.

Compared to the 37 quotes we've recorded for Caloundra West, this premium sits modestly above the suburb average of $2,686/yr and just above the suburb median of $2,756/yr. In other words, roughly half of comparable properties in the area are being quoted less — but the figure is still well within the normal range for the suburb, comfortably below the 75th percentile of $3,520/yr.

The good news? This property is faring significantly better than broader Queensland benchmarks. The QLD state average sits at $4,547/yr, and the Sunshine Coast LGA average is even higher at $4,608/yr — both dramatically above this quote. Much of that premium pressure in Queensland is driven by flood, cyclone, and storm risk across the state, particularly in higher-risk postcodes. Caloundra West's position outside designated cyclone risk zones is a meaningful advantage.

---

How Caloundra West Compares

Here's how this quote stacks up across the key benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $2,947/yr |

| Caloundra West Suburb Average | $2,686/yr |

| Caloundra West Suburb Median | $2,756/yr |

| Caloundra West 25th Percentile | $1,748/yr |

| Caloundra West 75th Percentile | $3,520/yr |

| QLD State Average | $4,547/yr |

| QLD State Median | $3,931/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

Interestingly, this quote is almost perfectly aligned with the national average of $2,965/yr, sitting just $18 below it. That puts Caloundra West in a relatively favourable position compared to much of Queensland, where premiums are consistently elevated due to natural hazard exposure.

For the full picture of what homeowners in this postcode are paying, visit the Caloundra West insurance stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence how insurers price the risk. Understanding these factors can help you make sense of your own quote.

Construction & Materials

Built in 2014, this home benefits from relatively modern building standards, which generally translates to lower risk in the eyes of insurers. Newer homes are less likely to have ageing electrical systems, plumbing issues, or structural wear that can lead to claims.

The brick veneer external walls and tiled roof are both well-regarded construction types in Queensland. Brick veneer offers solid fire resistance and structural integrity, while tiles are durable and perform well in the region's subtropical climate. Combined with a concrete slab foundation, this is a construction profile that most insurers view favourably.

Home Size & Fittings

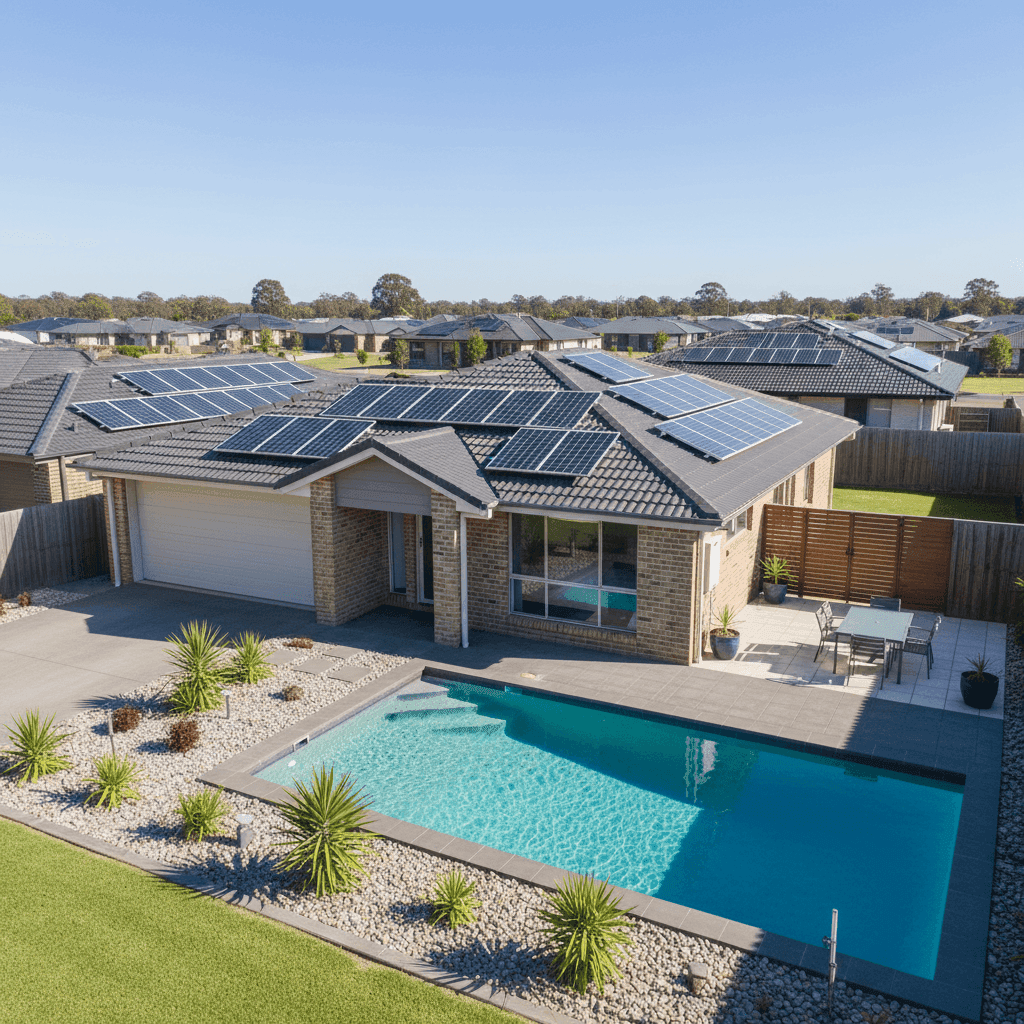

At 214 sqm with four bedrooms and two bathrooms, this is a substantial family home. The $695,000 building sum insured reflects the cost to fully rebuild — not the market value — and at this size and specification, that figure appears well-considered. Standard-grade fittings throughout (as opposed to premium or high-end finishes) help keep the rebuild cost — and therefore the premium — from escalating unnecessarily.

Pool, Solar & Climate Control

Three features of this property are worth noting from an insurance perspective:

- Swimming pool: Pools add some liability exposure and can increase the cost of a claim (e.g., damage to pool equipment or surrounds), which may contribute marginally to the premium.

- Solar panels: These are an asset worth protecting. Homeowners should confirm whether their solar system is included under the building sum insured or requires separate cover — not all policies treat rooftop solar the same way.

- Ducted climate control: A ducted air conditioning system is a significant fixed asset. Mechanical breakdown is typically excluded from home insurance, but damage from an insured event (such as a storm) should be covered under the building policy.

No Cyclone Risk

Caloundra West is not classified as a cyclone risk area, which is a notable premium advantage for a Queensland property. Cyclone loading can add hundreds — sometimes thousands — of dollars to annual premiums in higher-risk coastal and northern Queensland postcodes.

---

Tips for Homeowners in Caloundra West

Whether you're renewing your policy or shopping for the first time, here are four practical ways to make sure you're getting the right cover at a competitive price.

- Review your sum insured annually. Building costs in South East Queensland have risen sharply in recent years. Make sure your $695,000 building sum insured still reflects the true cost to rebuild your home — not what you paid for it. Underinsurance is one of the most common and costly mistakes homeowners make.

- Confirm your solar panels are covered. Ask your insurer explicitly how your rooftop solar system is treated under your policy. Some insurers include it as part of the building; others require it to be listed separately. Given the value of a modern solar installation, this is worth clarifying before you need to make a claim.

- Compare quotes before renewing. Loyalty doesn't always pay in insurance. Premiums can vary significantly between providers for the same property — sometimes by hundreds of dollars. Use a comparison service like CoverClub to see what other insurers would charge before you automatically renew.

- Consider your excess carefully. Both the building and contents excess on this policy are set at $1,000. Opting for a higher excess can reduce your annual premium, but make sure the saving is meaningful and that you could comfortably cover the excess out of pocket if you needed to make a claim.

---

Ready to Compare?

Whether your current premium feels too high or you simply want peace of mind that you're on a competitive rate, it pays to shop around. At CoverClub, we make it easy to compare home and contents insurance quotes for properties across Caloundra West and the broader Sunshine Coast. Get a quote today and see how your current policy stacks up.