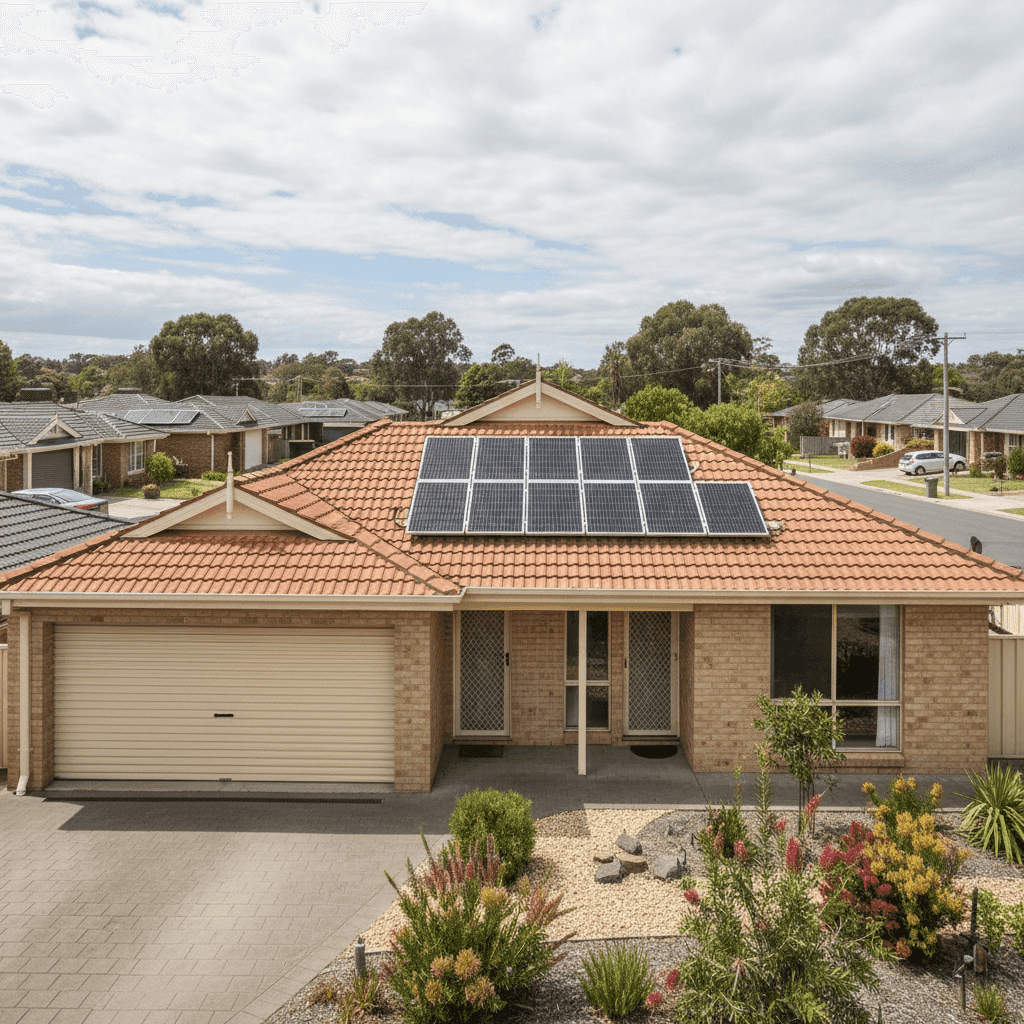

If you own a free standing home in Calwell, ACT 2905, you've probably wondered whether your home insurance premium is competitive — or whether you're quietly overpaying year after year. In this article, we analyse a real building insurance quote for a four-bedroom, two-bathroom brick veneer home in Calwell, and put that figure under the microscope using suburb, territory, and national data.

---

Is This Quote Fair?

The quote in question comes in at $1,809 per year (or $173/month) for building-only cover on a 305 sqm free standing home, with a building excess of $2,000 and a sum insured of $900,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up.

Compared to the Calwell suburb average of $1,835/yr, this quote sits just $26 below the mean — essentially right on the money. It's also comfortably within the interquartile range for the suburb: the 25th percentile sits at $1,507/yr and the 75th at $2,293/yr, meaning this premium lands squarely in the middle of what most Calwell homeowners are paying.

That said, "fair" doesn't necessarily mean "the best available." The suburb median is $1,678/yr — about $131 less than this quote — which suggests there may be room to find a more competitive price without sacrificing quality cover. It's worth shopping around to see whether another insurer will come in closer to that median mark.

---

How Calwell Compares

One of the most striking takeaways from this data is just how affordable Calwell is relative to broader benchmarks.

| Benchmark | Average Premium |

|---|---|

| Calwell (suburb average) | $1,835/yr |

| Unincorporated ACT (LGA average) | $2,172/yr |

| ACT (state average) | $2,288/yr |

| National average | $5,347/yr |

The quote analysed here is 21% below the ACT average and a remarkable 66% below the national average. Even accounting for the fact that national figures are skewed upward by high-risk regions — particularly cyclone-prone areas in Queensland and northern Western Australia — the ACT consistently emerges as one of the more affordable places to insure a home in Australia.

You can explore the full breakdown of ACT home insurance statistics or compare against national home insurance data to see how your own situation stacks up.

It's also worth noting that the suburb sample size here is 26 quotes — a reasonably solid dataset for a suburban ACT locality, giving us decent confidence in these figures.

---

Property Features That Affect Your Premium

Every home is different, and insurers weigh up a range of property characteristics when calculating your premium. Here's how the features of this particular Calwell home are likely influencing the price:

Brick Veneer Walls & Tiled Roof

Brick veneer construction is generally viewed favourably by insurers. It's durable, fire-resistant, and widely used across Canberra's suburban housing stock. Combined with a tiled roof — another low-risk, long-lasting material — this home presents a solid risk profile that typically attracts more competitive premiums than, say, weatherboard or metal sheet construction.

Stump Foundation

Homes built on stumps (also known as pier or post foundations) are common in certain parts of Australia, including some ACT properties from this era. While stumps can offer benefits like underfloor ventilation and easier access for maintenance, some insurers may apply a modest loading depending on the age and condition of the stumps. It's worth confirming your policy covers the foundation structure itself.

Solar Panels

This property includes solar panels, which are increasingly common across Canberra. Most standard building policies will cover fixed solar panels as part of the building structure, but it's essential to confirm this with your insurer. Given the replacement cost of a quality solar system, you'll want to ensure your sum insured accounts for this — and that the panels are explicitly listed as covered.

Ducted Climate Control

Ducted heating and cooling systems are a significant fixed asset in any home. As a built-in system, it should be covered under building insurance, but again, it's worth verifying with your insurer that the sum insured is sufficient to cover full replacement — including ductwork, the central unit, and installation costs.

Construction Year: 1990

At around 35 years old, this home is well past its initial build phase but not yet in the "ageing property" category that some insurers treat with extra caution. That said, it's a good idea to periodically review your sum insured to ensure it reflects current rebuild costs, which have risen substantially across Australia in recent years due to construction inflation.

No Pool, Standard Fittings

The absence of a swimming pool removes a common source of premium loading (pools introduce liability and maintenance risk). Standard fittings quality also keeps the replacement cost calculation straightforward, without the premium uplift that high-end finishes can attract.

---

Tips for Homeowners in Calwell

1. Review your sum insured regularly With $900,000 insured on a 305 sqm home, this policy is working with a rebuild rate of roughly $2,950/sqm — broadly in line with current ACT construction costs. However, building costs have been volatile. Use a building cost calculator annually to ensure you're not underinsured, especially if you've made renovations or improvements.

2. Confirm solar panel coverage in writing Don't assume your solar panels are covered. Contact your insurer and ask them to confirm — in writing — that the panels are included in your building cover and that the sum insured reflects their replacement value. A 6.6kW system can cost $8,000–$12,000 to replace.

3. Shop around at renewal time Even though this quote is rated "fair," the suburb median is $131/yr lower. Over five years, that's potentially $655 in savings. Use a comparison service like CoverClub at each renewal to check whether a better deal is available — loyalty doesn't always pay in insurance.

4. Consider your excess carefully This policy carries a $2,000 building excess. A higher excess generally reduces your premium, but make sure you can comfortably cover that amount out of pocket in the event of a claim. If cash flow is a concern, a lower excess with a slightly higher premium may be the more practical choice.

---

Ready to Compare?

Whether you're renewing an existing policy or insuring a new purchase, it pays to see what the market has to offer. Get a home insurance quote through CoverClub and compare your options in minutes. You can also explore detailed Calwell suburb insurance statistics to benchmark any quote you receive against real local data.