If you own a free standing home in Camden Park, NSW 2570, you've probably wondered whether your home insurance premium is competitive — or whether you're quietly paying too much. In this article, we break down a real home and contents insurance quote for a four-bedroom, three-bathroom brick veneer home in Camden Park, comparing it against suburb, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

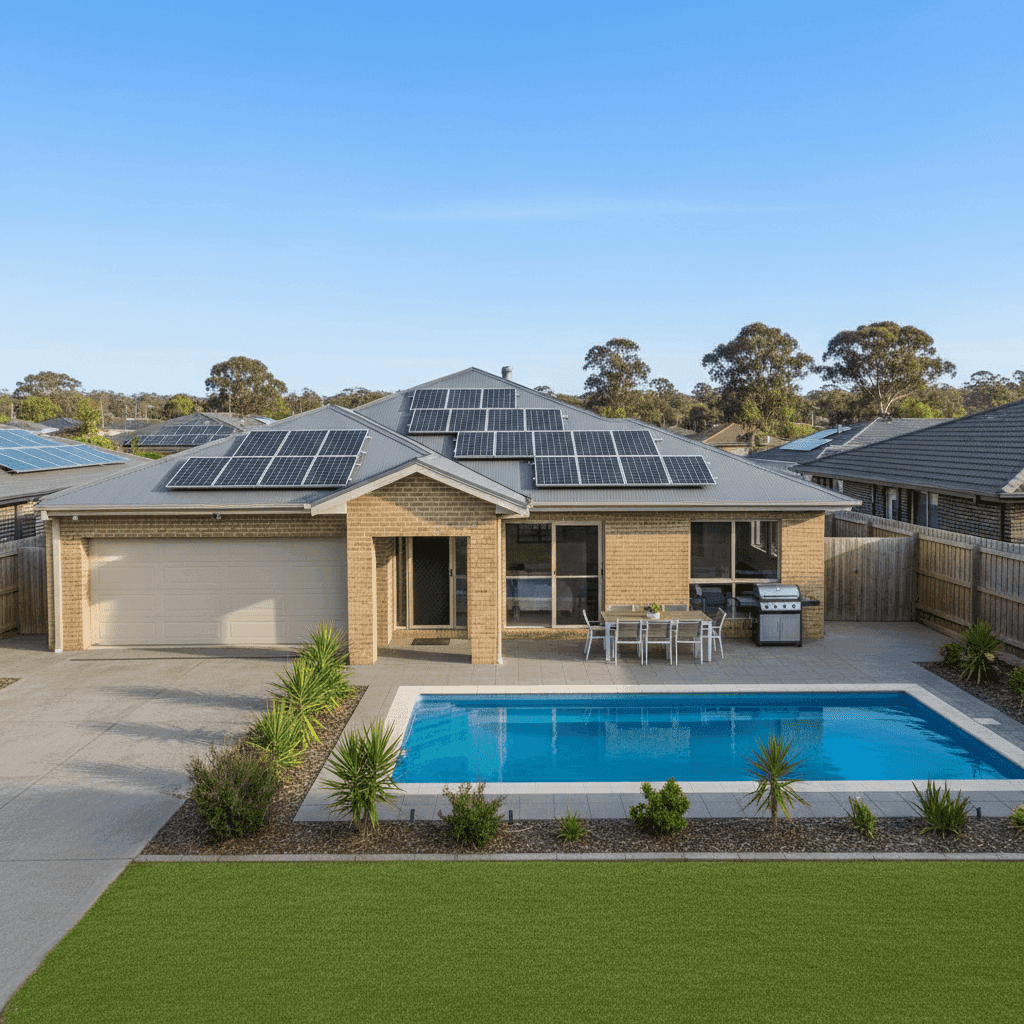

The quote in question comes to $3,473 per year (or $340 per month) for combined home and contents cover, with a building sum insured of $1,486,000 and contents valued at $249,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — Above Average.

To put that in perspective: the average home and contents premium across Camden Park suburbs sits at around $1,615 per year, with a median of $1,520. This quote is more than double that suburb median, which naturally raises a few eyebrows.

That said, context matters enormously here. The building sum insured of $1,486,000 is substantial — well above what many comparable homes in the area are insured for. A higher replacement value directly drives up the premium, so the comparison isn't entirely apples-to-apples. The property is also 268 sqm in size, features above-average fittings, a swimming pool, solar panels, and ducted climate control — all of which add to both the rebuild cost and the insurer's risk assessment.

Still, even accounting for these factors, there may be room to shop around and find a more competitive rate for this level of cover.

---

How Camden Park Compares

Understanding where Camden Park sits within the broader insurance landscape helps frame whether a premium is reasonable or inflated.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Camden Park (suburb) | $1,615/yr | $1,520/yr |

| Wollondilly LGA | $2,297/yr | — |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The NSW state average of $9,528 per year is notably high — driven largely by premium-heavy postcodes in flood-prone, bushfire-affected, or coastal regions across the state. Camden Park's suburb average of $1,615 is well below both the state and national averages, suggesting it's a relatively low-risk area from an insurer's perspective.

The Wollondilly LGA average of $2,297 per year is a useful middle ground — it reflects the broader local government area, which includes a mix of rural and suburban properties that can attract higher premiums due to bushfire exposure and distance from emergency services.

For Camden Park specifically, the 25th percentile sits at $1,453 and the 75th percentile at $1,864, based on a sample of 19 quotes. This quote at $3,473 sits well above the 75th percentile, reinforcing the "expensive" rating — though again, the high sum insured is a significant contributing factor.

---

Property Features That Affect Your Premium

This particular property has a number of characteristics that influence how insurers price the risk. Here's what's likely at play:

Brick veneer construction and tiled roof are generally viewed favourably by insurers. These materials are durable, fire-resistant, and less susceptible to storm damage compared to timber weatherboard or metal roofing. This typically results in a lower base premium.

Slab foundation is standard for homes of this era in NSW and doesn't typically attract a loading. However, slab homes can be more expensive to repair if subsidence or cracking occurs — something insurers factor into their long-term risk models.

Swimming pool adds to the insured value and introduces liability considerations. Most policies will include the pool structure under building cover, but it's worth confirming this with your insurer and ensuring the sum insured accounts for pool fencing, equipment, and any decking.

Solar panels are increasingly common on Australian homes, but they're not always automatically covered under standard building policies. Some insurers include them as part of the building; others treat them separately. With the cost of a quality solar system running into the tens of thousands, it's essential to confirm your panels are covered and that the sum insured reflects their replacement value.

Ducted climate control is a high-value fixture that contributes to the overall rebuild cost. At above-average fittings quality, this home likely features premium appliances, joinery, and finishes throughout — all of which push the sum insured higher and, in turn, the premium.

Construction year of 2008 places this home in a relatively modern bracket. Homes built after the introduction of updated Australian building codes generally benefit from better structural standards, which can positively influence premium pricing.

---

Tips for Homeowners in Camden Park

1. Review your sum insured carefully The building sum insured of $1,486,000 is a key driver of this premium. Use a reputable building cost calculator — such as the one provided by Cordell or your insurer — to confirm this figure is accurate. Over-insuring inflates your premium unnecessarily, while under-insuring leaves you exposed in the event of a total loss.

2. Confirm solar panels and pool are correctly covered Don't assume these are automatically included. Contact your insurer to verify that your solar system and pool are listed under your building cover, and that the sum insured accounts for their full replacement cost.

3. Compare quotes from multiple insurers With a premium sitting above the suburb's 75th percentile, it's well worth getting a fresh quote to see what other insurers would charge for the same level of cover. Premiums for identical properties can vary by hundreds — sometimes thousands — of dollars between providers.

4. Consider your excess level Both the building and contents excess are set at $1,000. Opting for a higher voluntary excess (say, $2,500 or $5,000) can meaningfully reduce your annual premium. Just make sure you're comfortable covering that amount out of pocket if you need to make a claim.

---

Compare Your Home Insurance Today

Whether you're renewing your policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from Camden Park and beyond. Get a home insurance quote today and find out whether you're getting a fair deal — or whether it's time to switch.