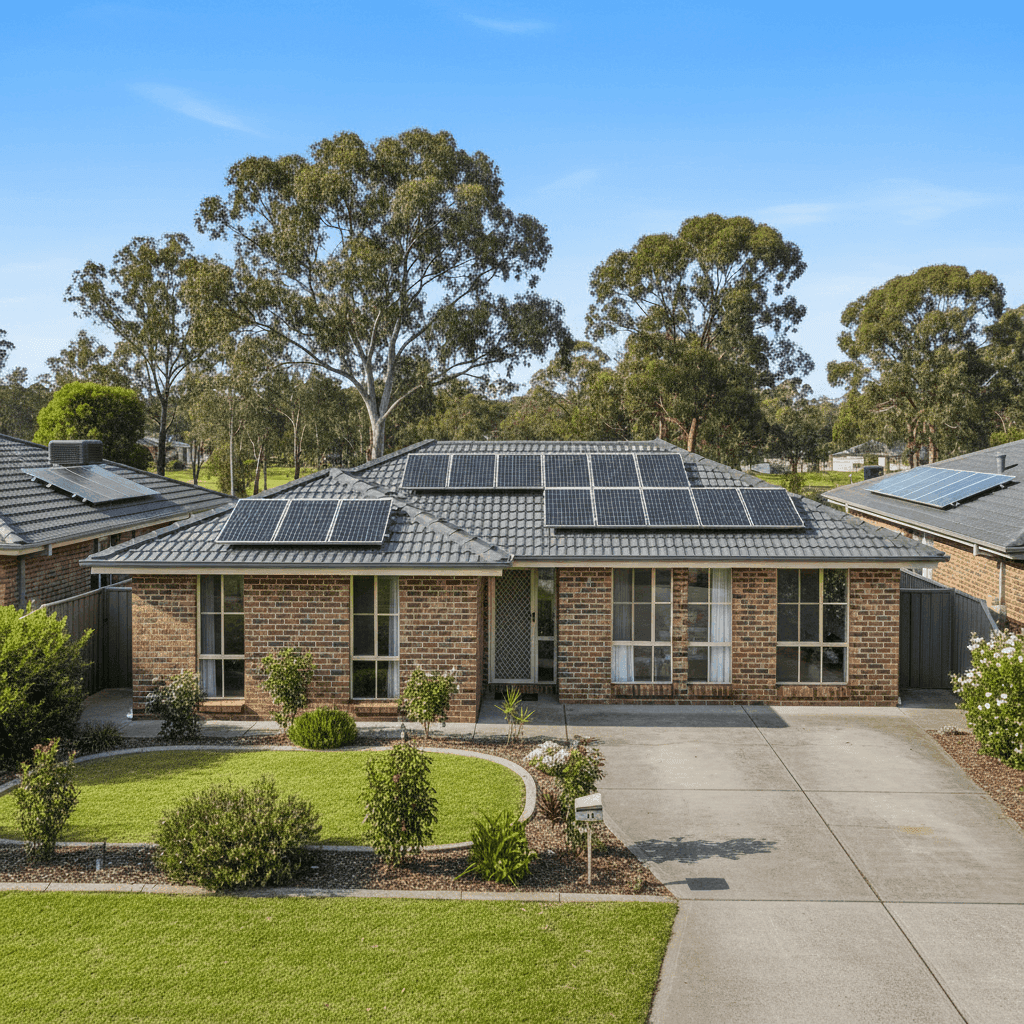

Cameron Park is a well-established residential suburb in the Lake Macquarie local government area, sitting roughly 20 kilometres south-west of Newcastle's CBD. Known for its family-friendly streets, bushland surrounds, and solid brick homes, it's the kind of suburb where homeowners tend to put down roots — and where protecting that investment with the right insurance cover really matters.

This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free-standing home in Cameron Park (postcode 2285), examining whether the price stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $3,927 per year (or $376 per month) for combined home and contents cover, with a building sum insured of $948,000 and contents valued at $248,000. Both the building and contents excess are set at $2,000.

Our pricing model rates this quote as Fair — Around Average, and the data backs that up. The suburb average for Cameron Park sits at $4,012 per year, meaning this quote is tracking just below the local average — a modest saving of around $85 annually. Against the suburb median of $3,769, it's sitting slightly above, which is consistent with the higher-than-typical sum insured and contents value included in this policy.

In short, this isn't a bargain-basement price, but it's not an outlier either. For the level of cover provided — nearly $1.2 million in combined insured value — it represents a reasonable market rate for the area.

---

How Cameron Park Compares

Understanding where Cameron Park sits in the broader insurance landscape helps put this quote in context. Here's how the numbers line up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,927 |

| Cameron Park Suburb Average | $4,012 |

| Cameron Park Suburb Median | $3,769 |

| Newcastle LGA Average | $3,835 |

| NSW State Average | $9,528 |

| NSW State Median | $3,770 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. The NSW state average of $9,528 looks alarming at first glance, but this figure is heavily skewed by high-risk and high-value properties across the state — think coastal properties, flood-prone areas, and prestige homes in Sydney. The state median of $3,770 is a far more representative figure for typical NSW homeowners, and this quote sits just $157 above that mark.

Compared to the national average of $5,347, Cameron Park homeowners are faring well. The suburb benefits from relatively low natural hazard risk — no cyclone exposure, no significant coastal flooding history — which keeps premiums competitive. You can explore Cameron Park suburb insurance statistics in more detail, or compare against NSW state-wide data and national benchmarks to see the full picture.

The 25th–75th percentile spread for Cameron Park runs from $2,665 to $5,247, which tells us there's meaningful variation in what locals are paying. This quote sits comfortably within the middle band of that range — neither the cheapest nor the most expensive.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence how insurers assess risk and calculate the premium.

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability, which can help keep premiums lower compared to timber-framed or clad homes. Combined with a tiled roof, this property sits in a construction category that most insurers consider low-to-moderate risk.

The stump foundation is worth noting. Homes on stumps (also known as pier foundations) are common in older NSW properties and can be more susceptible to subsidence or movement over time, particularly in areas with clay-heavy soils. Insurers may factor this in when pricing the policy.

Timber and laminate flooring throughout the home adds to the contents and building replacement cost, and is reflected appropriately in the sum insured. High-quality flooring can be expensive to replace after events like flooding or fire, so ensuring the building sum insured is adequate is important.

The presence of solar panels is an increasingly common feature in Cameron Park homes, and it's a detail that matters for insurance purposes. Solar panel systems — including inverters and mounting hardware — can represent a significant asset. Homeowners should confirm with their insurer whether panels are covered under the building policy and to what value.

Ducted climate control is another feature that adds to the overall replacement cost of the home. These systems are expensive to install and should be factored into the building sum insured calculation to avoid being underinsured in the event of a total loss.

At 214 square metres, this is a generously sized home, and the building sum insured of $948,000 reflects a rebuild cost of roughly $4,430 per square metre — broadly in line with current construction costs in the Newcastle region.

---

Tips for Homeowners in Cameron Park

1. Review your sum insured annually Construction costs have risen sharply in recent years. The cost to rebuild a home in the Newcastle region has increased significantly since 2020, and many homeowners find themselves underinsured without realising it. Use a building cost calculator or speak to a quantity surveyor to make sure your sum insured keeps pace with current rebuild costs.

2. Confirm solar panel coverage If your home has solar panels, check the specific terms of your policy. Some insurers include panels as part of the building sum insured, while others treat them as a separate item or exclude certain types of damage. Given the cost of a quality solar system, this is worth clarifying before you need to make a claim.

3. Consider your excess carefully This quote carries a $2,000 excess on both building and contents. A higher excess typically reduces your premium, but it also means a larger out-of-pocket cost when you claim. Think about what you could comfortably cover in an emergency and choose an excess that reflects your financial buffer.

4. Shop around at renewal time Insurance loyalty doesn't always pay. Insurers frequently offer better rates to new customers, and the difference between your current premium and a competitive quote can be substantial. Use comparison tools to benchmark your renewal offer before accepting it — even a "fair" price might have room to improve.

---

Compare Your Home Insurance with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new property, CoverClub makes it easy to see how your quote stacks up. We analyse real insurance data from across Australia to help homeowners in Cameron Park and beyond make informed decisions. Get a home insurance quote today and find out if you're paying a fair price — or if there's a better deal waiting for you.