Camira is a well-established suburb in the City of Ipswich, sitting about 28 kilometres south-west of Brisbane's CBD. Known for its leafy streets and family-friendly atmosphere, it attracts homeowners who appreciate the space and affordability that greater Ipswich offers. This analysis looks at a building-only insurance quote for a four-bedroom, two-bathroom free-standing home in Camira — and digs into whether the price stacks up against what others in the area are paying.

---

Is This Quote Fair?

The quote in question comes in at $4,393 per year (or $414 per month) for building-only cover, with a building excess of $5,000 and a sum insured of $1,500,000. Our price rating for this quote is Expensive — Above Average.

To put that in perspective, the suburb median premium for Camira (QLD 4300) sits at $2,880 per year. This quote is roughly 53% above that median, which is a meaningful gap. The 75th percentile for the suburb is $3,458 per year, meaning this quote exceeds what three-quarters of comparable properties in the area are paying. That's a signal worth taking seriously.

That said, "expensive" doesn't necessarily mean "wrong." Several property-specific factors — which we'll explore below — can legitimately push a premium above the local norm. The key question is whether those factors fully account for the difference, or whether there's room to shop around for a more competitive rate.

---

How Camira Compares

One of the more striking things about Camira's insurance data is the wide spread between the average and the median. The suburb average premium is $16,801 per year — dramatically higher than the median of $2,880. This kind of divergence usually signals that a small number of very high premiums (often for properties with elevated flood, subsidence, or other risk profiles) are skewing the average upward. The median is generally the more reliable benchmark for a "typical" property.

Here's how the numbers stack up across different levels:

| Benchmark | Premium |

|---|---|

| Camira (4300) Median | $2,880/yr |

| Camira (4300) Average | $16,801/yr |

| Camira 25th Percentile | $1,869/yr |

| Camira 75th Percentile | $3,458/yr |

| LGA (Ipswich) Average | $8,901/yr |

| QLD State Median | $3,903/yr |

| QLD State Average | $9,129/yr |

| National Median | $2,764/yr |

| National Average | $5,347/yr |

Interestingly, this quote of $4,393 sits above the national average of $5,347 — wait, actually it sits just below the national average, but well above the national median of $2,764. Compared to the Queensland state median of $3,903, this quote is about 13% higher. Against national benchmarks, it's above the median but below the state and national averages — placing it in a moderately elevated tier.

The Ipswich LGA average of $8,901 per year does provide some comfort — it suggests that across the broader Ipswich area, premiums can run quite high, and this particular quote is well below that LGA average.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to a premium above the suburb median. Understanding these factors can help you have more informed conversations with insurers.

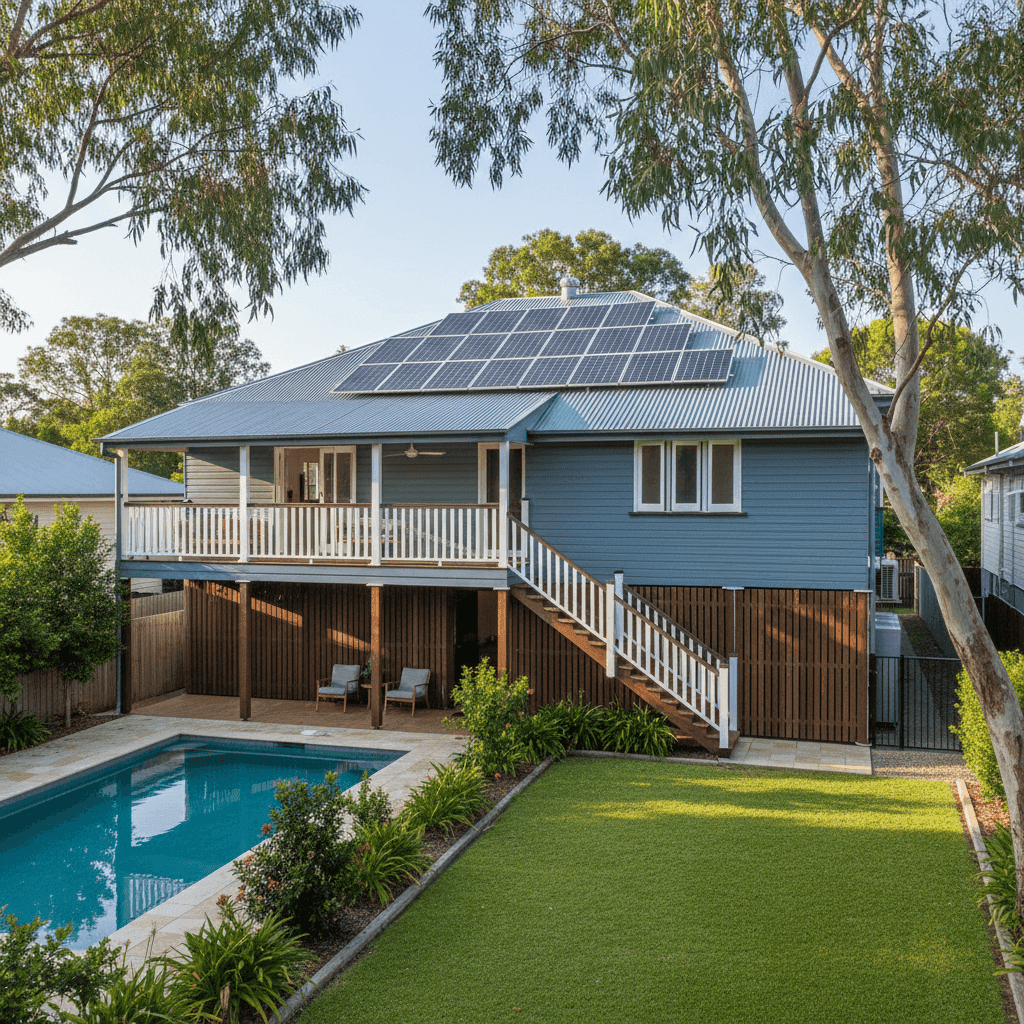

Weatherboard Timber Construction

Weatherboard wood external walls are one of the most significant premium drivers for Australian homes. Timber is considered higher risk than brick veneer or full brick because it is more susceptible to fire, rot, and pest damage. Most insurers apply a loading to timber-clad homes, which can meaningfully lift the base premium.

Elevated on Poles (Queenslander Style)

The home is elevated by at least one metre on poles — a classic Queenslander design feature. While this construction style offers excellent ventilation and some flood resilience (water can flow beneath the structure), it also introduces unique risks. The subfloor space, timber stumps, and elevated flooring can be more expensive to repair or replace, and some insurers price this accordingly.

Steel / Colorbond Roof

On the positive side, a steel Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant, and performs well in storms — which is a genuine consideration in south-east Queensland. This feature is unlikely to be adding to your premium and may even be moderating it.

Swimming Pool

The presence of a pool adds to the insured value of the property and introduces additional liability considerations. Pools require their own maintenance and can be costly to repair or replace after storm or hail events, which is reflected in premiums.

Solar Panels

Solar panels are a growing feature on Australian homes and are typically covered under building insurance. They add to the replacement cost of the structure and can be damaged by hail or severe weather. Insurers factor this into the sum insured and, by extension, the premium.

High Sum Insured ($1,500,000)

A sum insured of $1.5 million for a 268 sqm home is on the higher end. While it's always better to be adequately covered than underinsured, it's worth reviewing whether this figure accurately reflects the rebuild cost of the home. An overestimated sum insured directly inflates your premium. Consider using a building cost calculator or speaking to a quantity surveyor to confirm the right figure.

---

Tips for Homeowners in Camira

1. Review your sum insured carefully With a $1.5 million sum insured, it's worth confirming this aligns with current construction costs in the Ipswich area. Rebuilding a 268 sqm timber home on poles is not cheap, but if the figure is higher than necessary, you may be paying a premium loading you don't need.

2. Shop around — the spread in Camira is wide The gap between the 25th percentile ($1,869/yr) and this quote ($4,393/yr) is substantial. That range exists because different insurers price timber and elevated homes very differently. Getting three or more quotes is especially important for properties with non-standard construction.

3. Consider a higher excess to reduce your premium This quote already carries a $5,000 building excess, which is relatively high. However, if you're comfortable self-insuring for smaller claims, some insurers offer further premium reductions for even higher excess options. Weigh up the savings against the risk.

4. Maintain your home's timber and subfloor structure Insurers may decline claims or apply exclusions if damage is found to result from gradual deterioration, rot, or pest infestation. Regular maintenance of weatherboard cladding, restumping checks, and pest inspections are not just good housekeeping — they protect your ability to claim.

---

Compare Quotes and Find a Better Deal

Whether this quote is the right one for your home depends on your full risk picture — but the data suggests there may be room to find a more competitive rate. CoverClub makes it easy to compare building insurance quotes from multiple insurers in one place, so you can see exactly where your premium sits and make a confident decision.

Get a home insurance quote for your Camira property →

You can also explore the latest premium data for your area on the Camira suburb stats page or browse Queensland-wide insurance trends.