Nestled in the foothills of the D'Aguilar Range just northwest of Brisbane, Camp Mountain is a semi-rural suburb that blends leafy acreage living with reasonable proximity to the city. For homeowners here, protecting a substantial property investment with the right level of insurance cover is a serious consideration — and understanding whether you're paying a fair premium can be just as important as having the cover in the first place.

This article breaks down a recent home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Camp Mountain, QLD 4520, examining how it stacks up against state and national benchmarks, what property features are driving the cost, and what local homeowners can do to make the most of their cover.

---

Is This Quote Fair?

The short answer: yes — and then some.

The quoted annual premium of $5,564 (or $533/month) for combined home and contents cover has been rated CHEAP, meaning it sits below the average for comparable properties. For a building insured at $949,000 with $150,000 in contents cover, that's a competitive outcome by any measure.

To put it in context, the Queensland state average premium currently sits at $9,129 per year, with a state median of $3,903. This quote comes in well below the state average — saving roughly $3,565 annually compared to what many Queenslanders are paying. Against the national average of $5,347 (median: $2,764), the quote is broadly in line, though slightly above the national midpoint given the higher sum insured.

For a property of this size, build quality, and feature set, landing a below-average premium is a genuinely strong result. Homeowners in this position should feel confident they're getting good value — though it's always worth reviewing cover annually to ensure nothing has changed.

---

How Camp Mountain Compares

Suburb-level comparison data isn't currently available for Camp Mountain, but the broader picture tells an interesting story.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $5,564 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

| Brisbane LGA Average | $16,277 |

The standout figure here is the Brisbane LGA average of $16,277 — nearly three times the premium on this quote. While Camp Mountain falls within the broader Brisbane local government area, its semi-rural character, lower density, and distance from some of the flood and storm surge risks that affect inner-Brisbane and bayside suburbs likely contribute to a more favourable risk profile. Properties in low-lying riverside suburbs or areas with known flood histories can attract dramatically higher premiums, which pulls the LGA average up considerably.

For up-to-date suburb and state-level data, visit the CoverClub QLD stats page or explore the national benchmarks to see how your area compares.

---

Property Features That Affect Your Premium

Every insurer assesses risk differently, but certain property characteristics consistently influence what you'll pay. Here's how the features of this particular home play into the pricing:

Brick Veneer Walls & Colorbond Roof This is a solid, modern construction combination. Brick veneer offers good structural resilience and fire resistance, while Colorbond steel roofing is durable, lightweight, and performs well in Queensland's harsh summer conditions. Compared to older materials like asbestos sheeting or ageing timber, this combination generally attracts more favourable underwriting.

Concrete Slab Foundation Slab-on-ground construction is straightforward to assess and generally considered lower risk than suspended timber floors, which can be more susceptible to moisture damage and pest intrusion. It also simplifies claims assessments, which insurers tend to appreciate.

Construction Year: 2005 A home built in 2005 benefits from building codes introduced after the devastating 1999 Sydney hailstorms and other major weather events that prompted significant regulatory reform. These codes introduced stronger requirements for wind and weather resistance, making post-2000 homes statistically less vulnerable to certain types of damage.

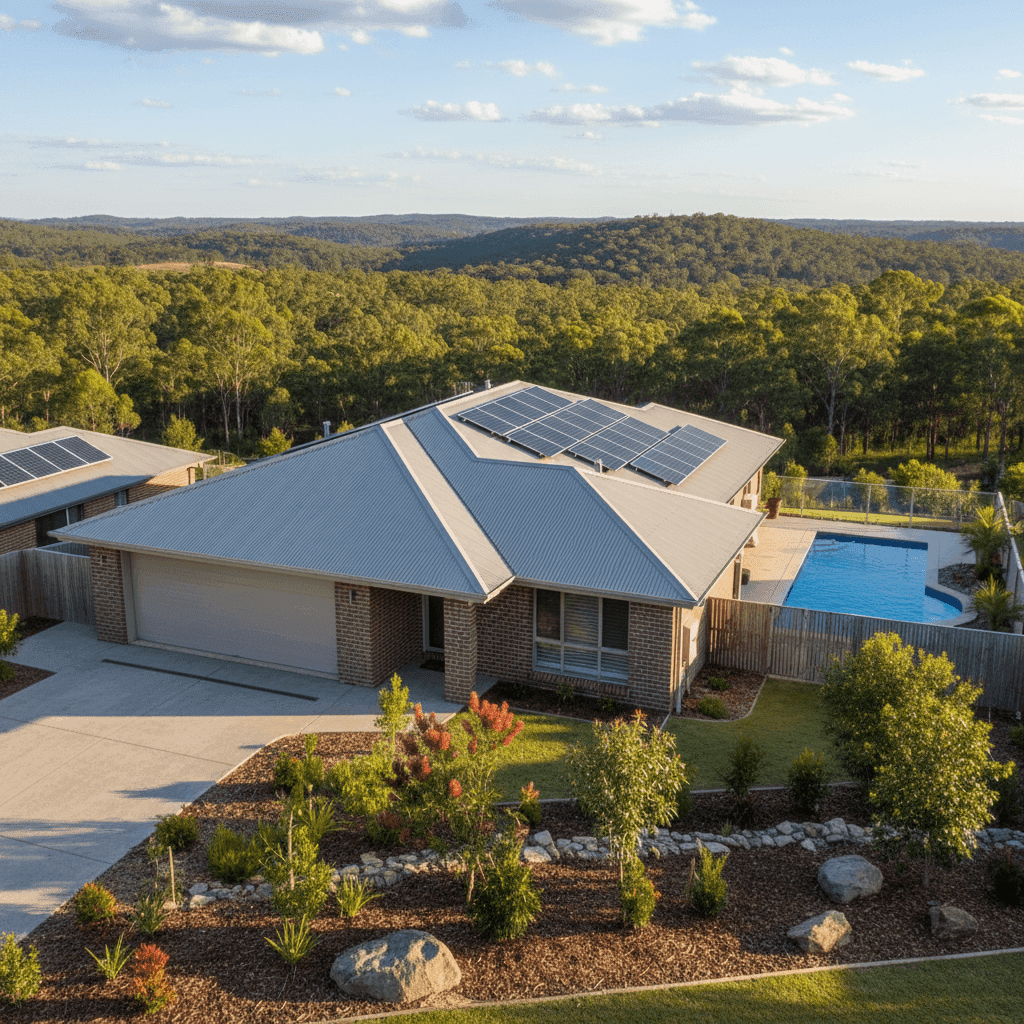

Swimming Pool A pool adds to the replacement cost of the property and introduces some liability considerations. It's factored into the building sum insured and is a legitimate reason for a slightly higher premium than an equivalent home without one.

Solar Panels Rooftop solar is increasingly common across Queensland, and most modern home insurance policies cover panels as part of the building sum insured. It's worth confirming with your insurer that your panels are explicitly included and that the $949,000 building sum adequately accounts for their replacement value.

Ducted Climate Control Ducted air conditioning is a significant fixed asset. Like solar panels, it should be captured within the building sum insured. Given the cost of replacing a full ducted system — often $10,000–$25,000 or more — ensuring it's properly accounted for in your cover is essential.

No Cyclone Risk Camp Mountain is not classified as a cyclone risk area, which is a meaningful factor in keeping premiums lower. Properties in North Queensland and coastal tropical regions often pay a substantial cyclone loading on top of their base premium. Being outside this zone is a genuine pricing advantage.

---

Tips for Homeowners in Camp Mountain

1. Review Your Building Sum Insured Annually With a building insured at $949,000 and features like a pool, solar panels, and ducted climate control, it's important to revisit this figure each year. Construction costs have risen sharply across Australia in recent years, and underinsurance remains one of the most common — and costly — mistakes homeowners make. Use a building cost calculator or ask your insurer to help you verify the figure is still adequate.

2. Check That Solar and Pool Equipment Are Explicitly Covered Don't assume these are automatically included. Read your Product Disclosure Statement (PDS) carefully to confirm solar panels, pool equipment (pumps, filters, heating), and ducted systems are covered for both accidental damage and storm events. If there are exclusions, ask your insurer about adding specific endorsements.

3. Maintain Defensible Space Around Your Property Camp Mountain's bush-adjacent setting means bushfire risk is a real consideration, even if it's not the dominant pricing factor here. Keeping gutters clear, trimming trees away from the roofline, and maintaining a cleared buffer around the home can reduce risk — and some insurers offer discounts for documented mitigation measures.

4. Compare Before You Renew A below-average premium today doesn't guarantee the same outcome at renewal. Insurers regularly re-price books of business, and what was competitive one year may not be the next. Use a comparison tool like CoverClub to benchmark your renewal quote before you accept it automatically.

---

Ready to Find a Better Deal?

Whether you're a Camp Mountain local or a homeowner anywhere in Australia, comparing home insurance quotes is one of the simplest ways to make sure you're not overpaying. CoverClub makes it easy to see real quotes side by side, so you can make an informed decision with confidence.