Cannonvale is a popular residential suburb sitting at the gateway to the Whitsundays in tropical North Queensland — and while the lifestyle is enviable, home insurance here comes with some unique considerations. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing home in Cannonvale (postcode 4802), compares it against suburb, state, and national benchmarks, and offers practical tips for getting the best value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $7,856 per year (or $753 per month) for combined home and contents insurance, covering a building sum insured of $1,478,000 and contents valued at $67,000. The building excess is $1,000 and the contents excess $500.

Our price rating for this quote is Expensive — above average for the Cannonvale area.

To put that in context: the suburb average premium sits at $4,749 per year, and the median is $4,540. This quote lands well above the 75th percentile of $5,898 — meaning it's pricier than at least three-quarters of comparable quotes we've seen in the area. That's a meaningful gap, and it warrants a closer look at what's driving the cost.

That said, "expensive" doesn't automatically mean "wrong." Several features of this particular property — which we'll explore below — genuinely justify a higher-than-average premium. The question is whether the margin above the local benchmark is proportionate.

---

How Cannonvale Compares

Understanding where Cannonvale sits relative to broader benchmarks helps put any individual quote into perspective. Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Cannonvale (4802) | $4,749/yr | $4,540/yr |

| Whitsunday LGA | $4,773/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

(Based on [Cannonvale suburb data](https://coverclub.com.au/stats/QLD/4802/cannonvale) from 45 quotes, [QLD state data](https://coverclub.com.au/stats/QLD), and [national data](https://coverclub.com.au/stats/national).)

A few things stand out here. Queensland's average premium of $9,129 is extremely high compared to the state median of $3,903 — a sign that a relatively small number of very expensive properties (often in cyclone-prone or flood-affected areas) are pulling the average up significantly. Cannonvale's local average of $4,749 is actually quite reasonable in that context, sitting below both the QLD and national averages.

The quote we're analysing, at $7,856, sits above the local suburb average but comfortably below the QLD state average. For a property with the features described below, this is a plausible — if still elevated — outcome.

---

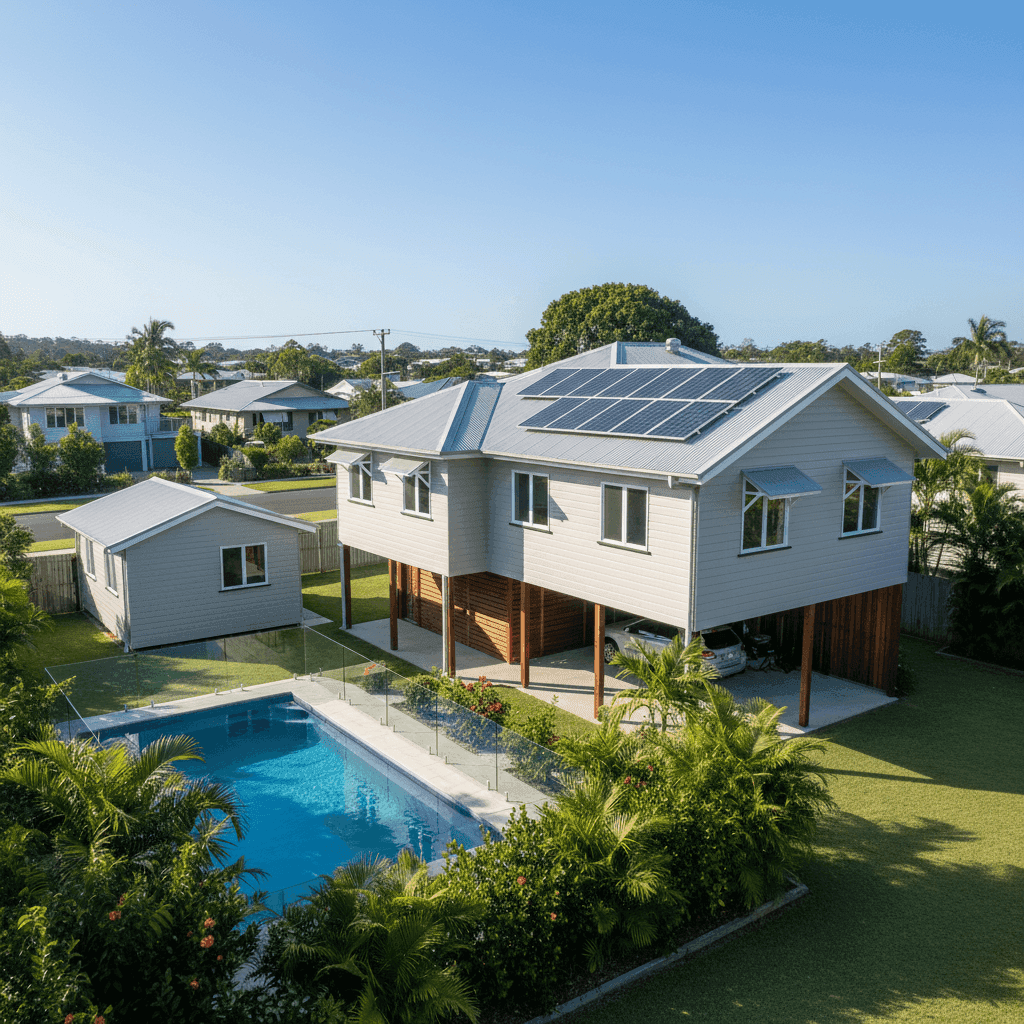

Property Features That Affect Your Premium

This isn't a straightforward suburban home, and insurers price it accordingly. Here's a breakdown of the key features influencing the premium:

🌀 Cyclone Risk Area

Cannonvale falls within a designated cyclone risk zone. This is arguably the single biggest driver of elevated premiums in the region. Insurers apply cyclone-specific loadings that can significantly increase the base cost of cover — and for good reason, given the area's exposure to severe tropical weather events.

🏠 Elevated Foundation (Poles)

The home is built on poles and elevated by at least one metre — a classic Queensland construction style designed to manage flood risk and improve airflow. While this can actually reduce flood risk (a positive for insurers), elevated homes can be more expensive to repair after storm or wind events, which may contribute to higher premiums.

🪵 Hardiplank/Hardiflex Walls & Colorbond Roof

Fibre cement cladding (Hardiplank/Hardiflex) is generally considered a resilient wall material, and Colorbond steel roofing is well-regarded for its durability in harsh Australian climates. These are broadly positive features from an insurer's perspective, though the combination on an older home (built 1984) may still attract some age-related loading.

📅 Construction Year: 1984

At over 40 years old, this home is approaching the age range where insurers start factoring in the cost of bringing electrical, plumbing, and structural elements up to modern standards in the event of a claim. This can push premiums higher compared to newer builds.

🏊 Swimming Pool

Pools add both asset value and liability risk to a property. Most insurers factor pool ownership into their pricing, particularly for contents and liability components of a policy.

☀️ Solar Panels

Solar panels are increasingly common but add complexity to home insurance. They represent a significant asset (typically covered under the building sum insured) and can complicate roof repairs after storm damage — a relevant consideration in a cyclone-prone area.

🏡 Granny Flat

The presence of a granny flat adds additional insurable structures to the property, which is likely reflected in the high building sum insured of $1,478,000. This figure covers the main dwelling and any associated structures, and it's worth ensuring your sum insured accurately reflects the full replacement cost of all buildings on the lot.

❄️ Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace and are typically included in the building sum insured. In a tropical climate like Cannonvale, these systems work hard year-round, which can factor into claims risk.

---

Tips for Homeowners in Cannonvale

1. Review your sum insured carefully At $1,478,000, the building sum insured for this property is substantial — and likely appropriate given the size (235 sqm), elevated construction, pool, solar panels, and granny flat. However, it's worth getting a professional building replacement cost estimate periodically to make sure you're neither underinsured nor paying for more cover than you need.

2. Compare quotes — especially in cyclone zones Insurers price cyclone risk very differently from one another. In areas like Cannonvale, the spread between the cheapest and most expensive quote can be enormous. Using a comparison platform like CoverClub to see multiple quotes side by side is one of the most effective ways to avoid overpaying.

3. Check your cyclone excess Many policies in North Queensland include a separate, higher excess specifically for cyclone-related claims — sometimes 1–2% of the sum insured. On a $1.47M building, that could mean a cyclone excess of $14,000–$29,000. Make sure you understand this before choosing a policy, not after a claim.

4. Ask about discounts for resilience upgrades Some insurers offer premium reductions for homes with cyclone-rated roofing, shutters, or other storm-mitigation features. Given the Colorbond roof and elevated construction, it's worth asking your insurer whether any resilience discounts apply — or whether switching to a provider that rewards these features could save you money.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for the first time, comparing quotes is the smartest move you can make as a homeowner in Cannonvale. Premiums vary widely between insurers — especially in cyclone-risk areas — and the savings can be substantial.

Get a home insurance quote at CoverClub and see how your current premium stacks up. It takes just a few minutes, and you might be surprised by what's available.