Canungra is a picturesque hinterland town nestled in the Scenic Rim region of South East Queensland, known for its lush green valleys, proximity to Lamington National Park, and a relaxed rural lifestyle. It's also a suburb where home insurance pricing can vary considerably — making it worth understanding exactly what you're paying and why.

This article breaks down a real building insurance quote for a four-bedroom, two-bathroom free standing home in Canungra (postcode 4275), and puts the numbers in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,384 per year (or $228/month) for building-only cover on a home insured for $453,000, with a $2,000 building excess. CoverClub's pricing analysis rates this quote as FAIR — around average for the area.

That's a reassuring result. In a suburb like Canungra, where the Scenic Rim LGA carries an average premium of $8,744 per year — heavily skewed by high-risk properties across the broader region — landing below the local suburb average is a solid outcome.

To put it plainly: this quote sits between the suburb's 25th percentile ($2,170/yr) and the median ($2,920/yr), which means roughly half of comparable Canungra properties are paying more. It's not the cheapest quote possible, but it's well within a reasonable range and meaningfully below what many homeowners in the area are being charged.

---

How Canungra Compares

Understanding your premium in isolation only tells part of the story. Here's how this quote stacks up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $2,384/yr |

| Canungra suburb average | $3,159/yr |

| Canungra suburb median | $2,920/yr |

| Canungra 25th percentile | $2,170/yr |

| Canungra 75th percentile | $3,523/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Based on 23 quotes sampled in the Canungra area. [View full Canungra suburb stats](https://coverclub.com.au/stats/QLD/4275/canungra).)

A few things stand out here. The Queensland state average of $9,129/yr is extraordinarily high — a figure driven by cyclone-prone coastal and far north Queensland postcodes, which push the mean well above what most South East Queensland homeowners actually pay. The state median of $3,903 is a more useful reference point, and this quote still comes in comfortably below it.

Compared to the national average of $5,347/yr, this quote is again well below average — though the national median of $2,764 is slightly lower than the quoted premium, suggesting that on a national scale, this sits just above the midpoint.

The key takeaway: for a property in the Scenic Rim hinterland, this is a competitive result.

---

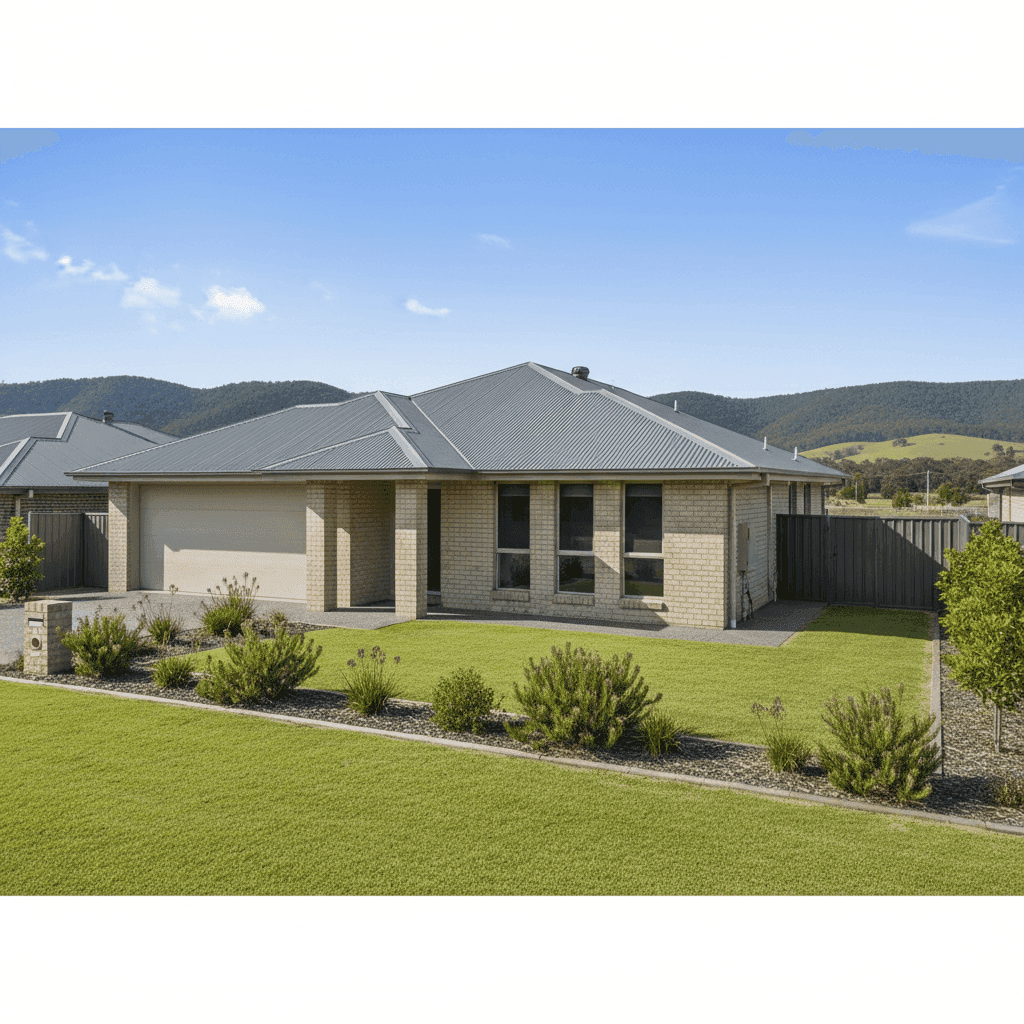

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour from a risk and pricing perspective:

Brick Veneer Walls Brick veneer is one of the more resilient external wall materials for Australian conditions. It offers good fire resistance and structural durability, which insurers generally view favourably compared to lightweight cladding or weatherboard construction.

Steel/Colorbond Roof A Colorbond steel roof is a strong asset when it comes to insurance pricing. It's highly resistant to fire, performs well in high winds, and has a long lifespan with minimal maintenance. Compared to terracotta or concrete tiles, steel roofing is typically associated with lower claim risk for storm and hail events.

Slab Foundation Concrete slab foundations are straightforward to assess and generally carry less subsidence or movement risk than suspended timber floors or pier-and-beam constructions, particularly in stable soil conditions.

Relatively New Construction (2020) A home built in 2020 benefits from modern building codes, which in Queensland have progressively strengthened requirements around wind resistance, weatherproofing, and structural integrity. Newer homes tend to attract more competitive premiums than older stock requiring more maintenance or built to outdated standards.

Ducted Climate Control The presence of ducted air conditioning adds to the overall replacement value of the home — and is correctly factored into the $453,000 sum insured. It's worth ensuring your insurer's policy explicitly covers fixed mechanical systems as part of the building definition.

No Pool, No Solar The absence of a pool removes a common source of liability and maintenance claims. Similarly, no solar panels means one less variable for insurers to price around (panels on older homes can sometimes complicate roof claims). Both simplify the risk profile.

Timber/Laminate Flooring Timber and laminate floors are susceptible to water damage, which is worth keeping in mind when reviewing your policy's water damage provisions — particularly for events like burst pipes or storm water ingress.

---

Tips for Homeowners in Canungra

1. Review your sum insured annually Construction costs in Queensland have risen significantly in recent years. A $453,000 sum insured may be appropriate today, but it's worth recalculating your estimated rebuild cost each year — especially as labour and materials costs fluctuate. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Consider your excess strategically This policy carries a $2,000 building excess. A higher excess typically reduces your annual premium, but make sure it's an amount you could genuinely afford to pay at short notice following a significant event. If cash flow is a concern, a lower excess with a slightly higher premium may be worth the trade-off.

3. Check your policy's bushfire provisions While Canungra is not classified as a cyclone risk area, the Scenic Rim hinterland does carry bushfire exposure, particularly during dry summer months. Review whether your policy includes bushfire cover as standard, and check for any specific exclusions or sub-limits that may apply to your area.

4. Compare at renewal — not just at inception Insurers often offer their best pricing to new customers. If you've held the same policy for two or more years without comparing alternatives, there's a reasonable chance you're paying more than you need to. Use renewal time as a prompt to run a fresh comparison.

---

Compare Your Options at CoverClub

Whether you're renewing an existing policy or shopping for cover on a new purchase, it pays to see the full picture. CoverClub helps Australian homeowners compare building and contents insurance quotes quickly and transparently — so you can make a confident, informed decision.