Caravonica is a quiet residential suburb nestled in the hills just west of Cairns in Far North Queensland — and if you own a free standing home here, you already know that insurance is rarely straightforward. Between the tropical climate, cyclone season, and the unique construction profiles of homes built in this region, premiums in postcode 4878 can vary enormously. This article breaks down a real building insurance quote for a 3-bedroom free standing home in Caravonica, compares it against local, state, and national benchmarks, and offers practical guidance for homeowners looking to get better value on their cover.

---

Is This Quote Fair?

The quote in question sits at $35,359 per year (or $3,389/month) for building-only cover on a 130 sqm concrete home, with a sum insured of $507,000 and a $1,000 building excess. Our price rating for this quote is Expensive — Above Average.

To put that in context: the suburb median premium in Caravonica is $10,007 per year, meaning this quote is more than three times the typical price paid by other homeowners in the same postcode. Even measured against the suburb's 75th percentile — where the priciest quarter of quotes sit — at $26,591/yr, this quote still comes in significantly higher.

That said, it's worth noting that the suburb average is a striking $82,426/yr, which tells us that while most Caravonica homeowners pay around $10,000, a small number of quotes are pulling that average up dramatically. Insurance pricing in cyclone-prone areas can be highly sensitive to individual property risk factors, and outlier quotes are not uncommon.

So while this quote is above average for the suburb, it's not entirely without precedent in a postcode where premiums can swing wildly depending on construction type, age, and proximity to risk zones.

---

How Caravonica Compares

The gap between Caravonica and the rest of Australia is stark. Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Caravonica (4878) | $82,426/yr | $10,007/yr |

| Cairns LGA | $12,404/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

Even the Caravonica median of $10,007 is nearly double the Queensland state median of $3,903, and close to four times the national median of $2,764. This reflects the elevated risk profile of Far North Queensland — a region regularly exposed to tropical cyclones, heavy rainfall, and flooding.

You can explore more detailed suburb-level data on the Caravonica insurance stats page, compare it against Queensland-wide figures, or see where it sits against the national picture.

The wide spread between the 25th percentile ($7,949/yr) and the 75th percentile ($26,591/yr) in Caravonica also highlights just how much individual property characteristics can shift your premium — there's no single "typical" price here.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a direct bearing on what insurers charge — and in some cases, they work in the homeowner's favour.

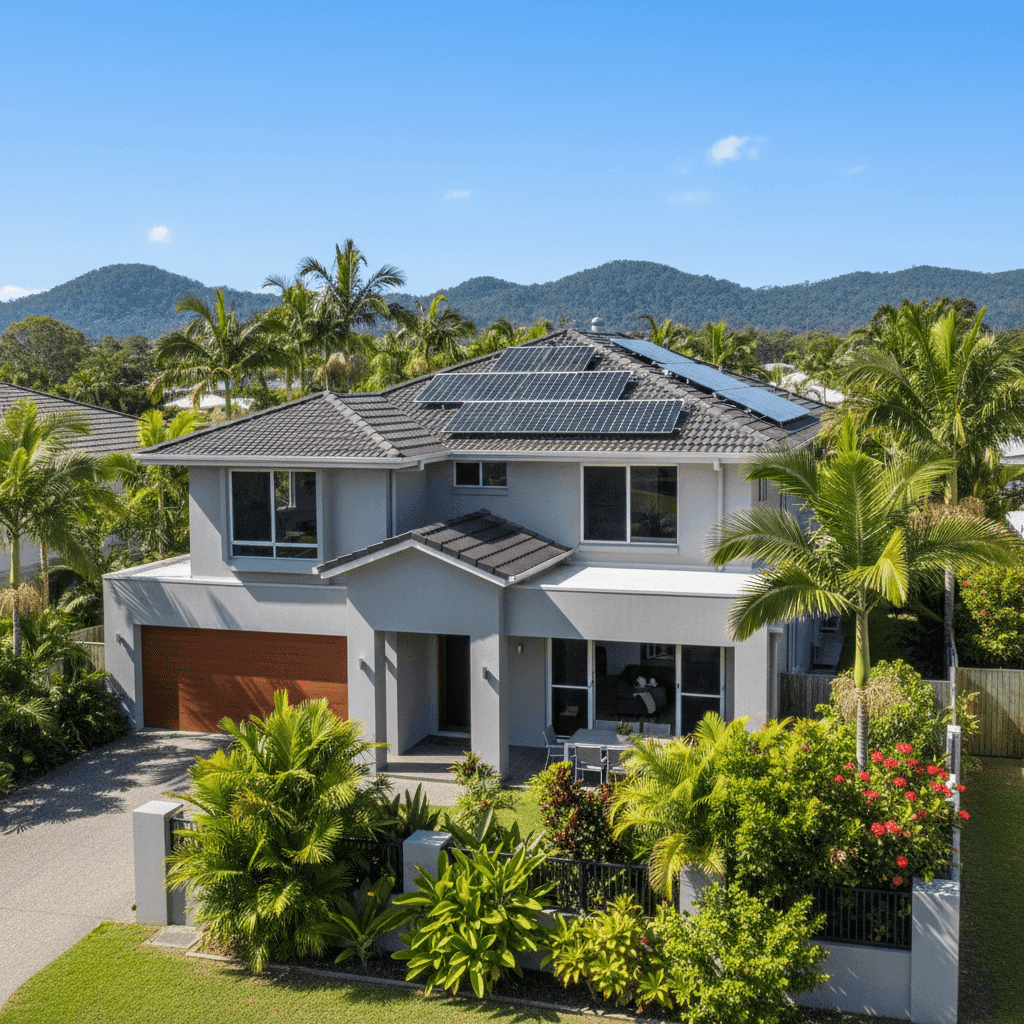

Cyclone Risk Area This is the single biggest driver of elevated premiums in Caravonica. Homes in Far North Queensland fall within designated cyclone risk zones, and insurers price accordingly. Cyclone cover typically includes damage from wind, rain ingress, and associated debris — all of which are costly to claim in a severe event.

Construction Year (1984) A home built in 1984 predates some of the more stringent cyclone building codes introduced in Queensland following Cyclone Tracy and subsequent reviews. Older homes may be viewed as higher risk by underwriters, particularly if they haven't been retrofitted to modern standards.

Concrete External Walls Concrete construction is generally viewed favourably by insurers in cyclone-prone areas — it's more resistant to wind damage than timber weatherboard, for example. This likely helps moderate the premium somewhat compared to less robust wall types.

Tiled Roof Tiles can be a mixed signal for insurers. While they're durable under normal conditions, they can be vulnerable to uplift in high winds if not properly secured. In a cyclone risk zone, this is a factor underwriters pay close attention to.

Slab Foundation A concrete slab foundation is generally considered low-risk and straightforward to assess, which is a neutral-to-positive factor for pricing.

Solar Panels Solar panels add replacement value to the property and introduce some additional risk (roof penetrations, panel damage in storms), which can nudge premiums slightly higher. Ensuring your sum insured accounts for the panels is important.

Ducted Climate Control Ducted air conditioning systems are a meaningful addition to a home's rebuild cost. At 130 sqm, a full ducted system represents a notable portion of the fit-out value, and this should be reflected in the sum insured.

Vinyl Flooring & Standard Fittings These are relatively modest finishes, which helps keep the rebuild cost estimate grounded. Standard fittings and vinyl floors are less expensive to replace than high-end alternatives, which is a moderating factor on the sum insured.

---

Tips for Homeowners in Caravonica

1. Shop around — seriously The spread between the cheapest and most expensive quotes in Caravonica is enormous. With a 25th percentile of $7,949 and quotes like this one at $35,359, the difference between insurers can be tens of thousands of dollars per year. Never accept a renewal without comparing at least two or three alternatives. Get a quote through CoverClub to see what competing insurers are offering.

2. Review your sum insured carefully At $507,000 for a 130 sqm home, the sum insured here works out to roughly $3,900/sqm — which is on the higher end for standard construction. Make sure your figure reflects a realistic rebuild cost (not market value), factoring in your ducted system and solar panels. Overinsuring adds to your premium unnecessarily, while underinsuring leaves you exposed.

3. Ask about cyclone mitigation discounts Some insurers offer premium reductions for homes that have been assessed or retrofitted to improve cyclone resilience — things like roof tie-downs, shutters, or updated connections. It's worth asking your insurer directly whether any works could qualify you for a discount.

4. Consider your excess strategically A $1,000 excess is relatively standard, but in a high-premium environment like Caravonica, opting for a higher voluntary excess can meaningfully reduce your annual cost. If you have the financial buffer to absorb a larger out-of-pocket expense in the event of a claim, this trade-off can be worth exploring.

---

Compare Your Options with CoverClub

Home insurance in Caravonica is genuinely complex — and paying more than you need to is an easy trap to fall into when premiums vary this dramatically. CoverClub makes it simple to compare building and contents insurance quotes from a range of Australian insurers, all in one place.

Whether you're reviewing an existing policy or shopping for cover for the first time, start your comparison at CoverClub and make sure you're getting the right protection at a fair price.