Cardwell is a small coastal town in Far North Queensland, nestled between the rainforest and the Coral Sea on the edge of the Cassowary Coast. It's a beautiful place to call home — but as any local knows, living in tropical Queensland comes with its share of weather-related risks. This article takes a close look at a recent home and contents insurance quote for a three-bedroom, two-bathroom free-standing home in Cardwell (QLD 4849), breaking down whether the price stacks up and what's driving the cost.

---

Is This Quote Fair?

The quote in question comes in at $5,995 per year (or $574/month) for a free-standing home with a building sum insured of $1,132,000 and $50,000 in contents cover. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up.

Compared to the suburb average for Cardwell of $4,735/yr, this quote sits roughly 27% above what other homeowners in the area are paying on average. It also exceeds the suburb's 75th percentile of $5,762/yr, meaning this premium is higher than approximately three-quarters of quotes seen in the postcode.

That said, "expensive" doesn't necessarily mean "wrong." A high sum insured of over $1.1 million — reflecting the top-of-the-range fittings and elevated construction — will naturally push premiums upward. The question is whether there's room to find a more competitive rate for the same level of cover.

---

How Cardwell Compares

To put this quote in proper context, here's how Cardwell's insurance market sits relative to the rest of Queensland and the country:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Cardwell (4849) | $4,735/yr | $4,141/yr |

| LGA (Cassowary Coast) | $5,573/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

(Based on 46 quotes sampled in the Cardwell postcode)

A few things stand out here. The Queensland state average of $9,129/yr is extraordinarily high — driven by a large number of high-risk properties across the state, particularly in cyclone-prone coastal and northern regions. The median of $3,903/yr tells a different story, suggesting that a significant portion of QLD premiums are pulled upward by outliers.

At the national level, the average of $5,347/yr is close to this quote, but the national median of $2,764/yr reflects just how much cheaper home insurance can be in lower-risk parts of Australia.

For Cardwell specifically, the suburb median of $4,141/yr is a useful anchor. This quote at $5,995/yr is notably above that figure, though the elevated building sum insured and premium property features do provide some justification.

---

Property Features That Affect Your Premium

Several characteristics of this particular home have a meaningful influence on the insurance premium — both upward and downward.

🔺 Factors Pushing the Premium Higher

Cyclone Risk Area This is arguably the single biggest driver. Cardwell sits squarely in a declared cyclone risk zone, and insurers price this in heavily. Cyclone damage can be catastrophic and widespread, and premiums in Far North Queensland reflect the statistical likelihood of a significant weather event occurring.

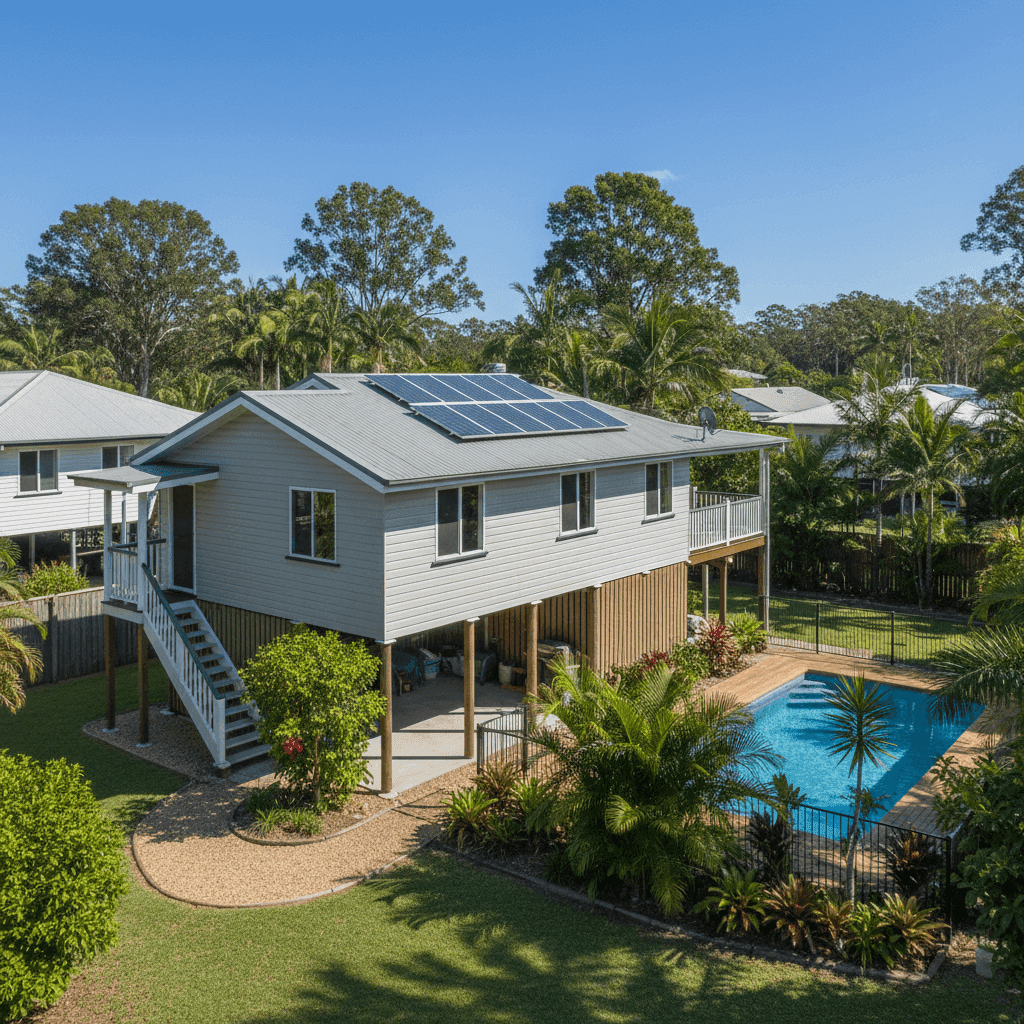

Elevated Construction (Stumps) The home is elevated by at least one metre on stumps — a classic Queenslander-style build. While elevation can actually reduce flood risk, it introduces structural complexity that insurers factor into rebuild costs. Combined with a large building sum insured, this contributes to the premium.

High Sum Insured ($1,132,000) Top-of-the-range fittings — think high-end kitchens, premium bathrooms, quality flooring — significantly increase the cost to rebuild. A $1.1M sum insured is well above the average for a 139 sqm home, and the premium reflects that rebuild value accordingly.

Pool and Solar Panels Both a swimming pool and solar panel system add to the insurable value of the property and introduce additional liability and replacement cost considerations. Pools in particular can be expensive to repair or replace after storm or cyclone damage.

🔻 Factors That May Moderate the Premium

Modern Construction (2018) A home built in 2018 benefits from contemporary building codes, which in Queensland include strict cyclone-resistant construction standards. Newer builds tend to attract slightly lower premiums than older homes of equivalent value.

Steel/Colorbond Roof Colorbond roofing is well-regarded by insurers for its durability, particularly in high-wind environments. It's more resistant to uplift and impact than older roofing materials, which can work in the homeowner's favour at assessment time.

Hardiplank/Hardiflex Cladding Fibre cement cladding is fire-resistant and durable in tropical climates, which insurers generally view positively compared to timber weatherboard or other materials.

Ducted Climate Control While this adds to the replacement value of the home, it's a fixed installation that's already reflected in the sum insured rather than being a separate risk factor.

---

Tips for Homeowners in Cardwell

1. Compare Quotes — Especially in a Cyclone Zone

Insurer appetite for cyclone-risk properties varies enormously. Some insurers price this risk conservatively (read: expensively), while others are more competitive. Given this quote is above the suburb average, it's well worth getting a comparison quote to see what other insurers are offering for the same property.

2. Review Your Sum Insured Carefully

A $1,132,000 sum insured is substantial. Make sure it accurately reflects the cost to rebuild the home (not its market value), including demolition, professional fees, and the cost of your premium fittings. Overinsuring drives your premium up unnecessarily, while underinsuring leaves you exposed. Use a building cost calculator or speak to a quantity surveyor if you're unsure.

3. Ask About Cyclone Mitigation Discounts

Some insurers offer premium reductions for homes that have undergone cyclone mitigation improvements — such as roof tie-down upgrades, storm shutters, or other wind-resistance measures. Given the home was built in 2018, it likely already meets current standards, but it's worth asking your insurer whether any additional measures could reduce your rate.

4. Consider Your Excess Level

Both the building and contents excess are set at $1,000. Increasing your excess — say, to $2,500 or $5,000 — can meaningfully reduce your annual premium. Just ensure you're comfortable covering that amount out of pocket in the event of a claim.

---

Ready to Find a Better Rate?

Whether you're a Cardwell local or researching home insurance in Far North Queensland, CoverClub makes it easy to compare quotes and understand what you're actually paying for. Check out the Cardwell suburb insurance stats to see how your quote stacks up, or get a new quote today to see if there's a more competitive option available for your home.