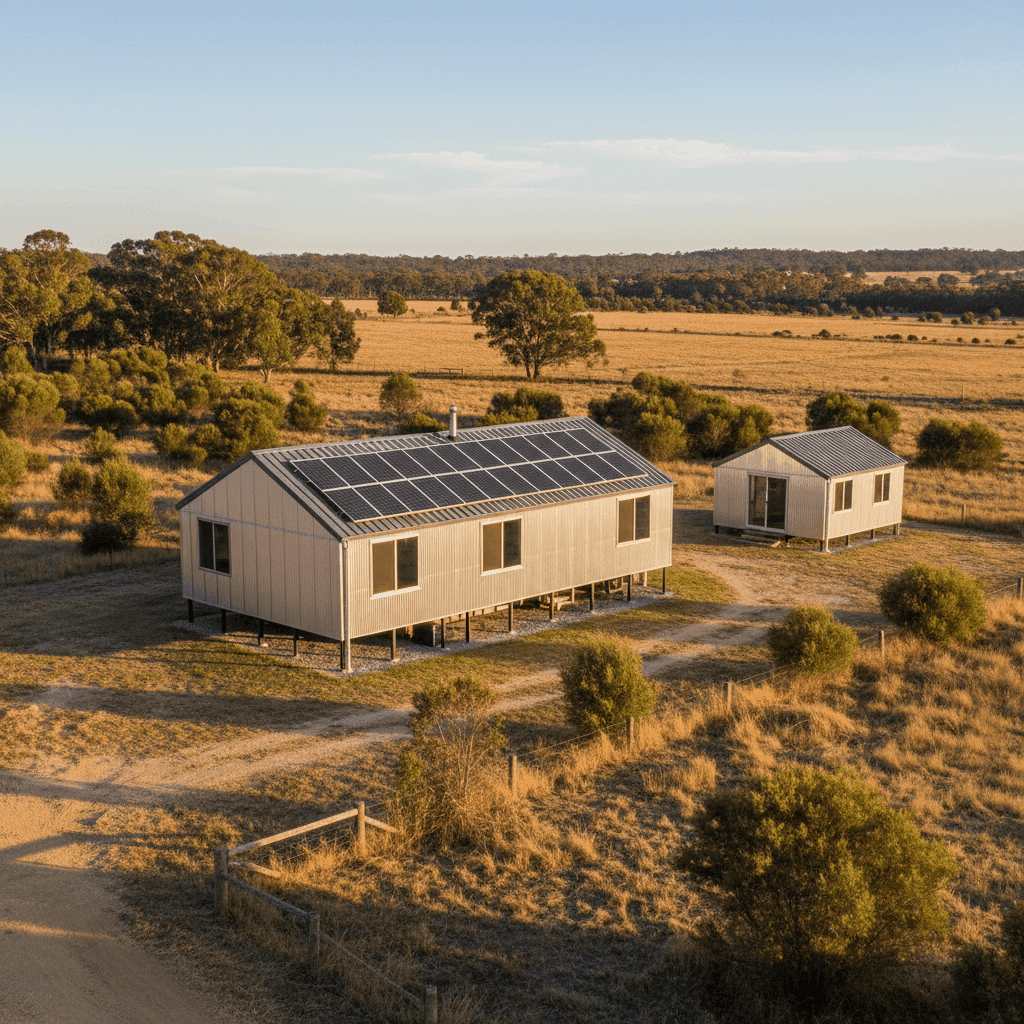

Cargo is a small rural locality in the Central West of New South Wales, sitting within the Cabonne Council area near Orange. It's the kind of place where properties tend to have real character — and this particular free-standing home is no exception. Built in 2014 on stumps with aluminium external walls and a Colorbond steel roof, this three-bedroom, three-bathroom property comes with a granny flat, solar panels, and ducted climate control across 169 square metres. So when a combined home and contents insurance quote comes back at $1,805 per year (or $173/month), the natural question is: is that a fair price?

Let's dig into the numbers.

---

Is This Quote Fair?

The short answer is yes — but only just. This quote has been rated Fair (Around Average), which means it's broadly in line with what other homeowners in Cargo are paying, without being a standout bargain.

To put it in context:

- The suburb median premium for Cargo (postcode 2800) is $1,811/yr — this quote sits almost exactly on that line at $1,805, which is reassuring.

- The suburb average is slightly higher at $1,999/yr, suggesting a handful of more expensive policies are pulling the mean upward.

- At the 25th percentile, some Cargo homeowners are paying as little as $1,257/yr, while those at the 75th percentile are paying up to $2,633/yr.

So while this quote isn't in the cheapest quarter of the market, it's also well clear of the most expensive. Landing right on the median is a solid outcome — it means roughly half of comparable quotes in the area are more expensive, and half are cheaper. That said, there's clearly room to find a better deal if you shop around, with potential savings of over $500/yr compared to this quote if you can access that lower quartile pricing.

---

How Cargo Compares to the Rest of NSW and Australia

One of the more striking aspects of this analysis is just how affordable Cargo is relative to broader benchmarks. Check out NSW home insurance statistics and you'll quickly see that the state average premium sits at a staggering $9,528/yr — though this figure is heavily skewed by high-risk and high-value properties across the state, particularly in coastal and flood-prone areas.

The NSW median of $3,770/yr is a more representative figure, and even then, Cargo's median of $1,811/yr is less than half of that. This reflects the relatively low-risk profile of the region — no cyclone exposure, lower population density, and generally manageable weather patterns compared to coastal NSW.

Zooming out to national home insurance data, the picture is similar:

| Benchmark | Premium |

|---|---|

| National average | $5,347/yr |

| National median | $2,764/yr |

| NSW average | $9,528/yr |

| NSW median | $3,770/yr |

| Cargo suburb average | $1,999/yr |

| This quote | $1,805/yr |

Cargo homeowners are paying significantly less than the national median, which is a genuine advantage of living in this part of regional NSW. The LGA average (Dubbo region) sits at $3,426/yr — again, well above what this property is being quoted.

You can explore more localised data on the Cargo NSW 2800 insurance stats page.

> Note: The suburb sample size here is 17 quotes, which is a reasonably small dataset. Averages can shift as more data comes in, so treat these figures as a useful guide rather than a definitive benchmark.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the premium — some favourably, others less so.

Aluminium cladding and Colorbond roof are generally well-regarded by insurers. Both materials are durable, fire-resistant, and low-maintenance, which reduces the likelihood of weather-related claims. Colorbond in particular performs well in Australian conditions, handling heat, rain, and wind without the vulnerabilities of older roofing materials.

Stump foundations can be a mixed bag. On one hand, they provide good ventilation and are common in regional NSW. On the other, they can be more susceptible to pest damage and may complicate certain types of structural claims. Insurers will factor this in when assessing rebuild risk.

Timber and laminate flooring adds value to the home but can increase the cost of contents and building claims — water damage to timber floors, for example, can be costly to repair or replace.

Solar panels are an increasingly common feature, but they do add to the sum insured. Many policies cover panels as part of the building, though it's worth confirming this explicitly with your insurer. The same applies to ducted climate control, which is a significant fixed asset and should be included in your building sum insured calculation.

The granny flat is an important consideration. Depending on how it's used — whether it's owner-occupied, rented out, or used for family — it may affect your coverage requirements. Some standard home policies don't automatically extend full cover to a separate dwelling on the same property, so it's worth checking the fine print.

The building sum insured of $200,000 for a 169 sqm home built in 2014 warrants a closer look. Construction costs in regional NSW have risen sharply in recent years — it's worth using a building cost calculator to ensure this figure reflects current rebuild costs, including the granny flat.

---

Tips for Homeowners in Cargo

1. Double-check your granny flat is covered A granny flat is a meaningful asset. Confirm with your insurer whether it's included under your main building policy or whether you need a separate endorsement. Don't assume — read the Product Disclosure Statement carefully.

2. Review your building sum insured annually With construction costs rising across regional NSW, a sum insured that was adequate two years ago may now be insufficient. Underinsurance is one of the most common — and costly — mistakes homeowners make. Consider getting a professional valuation or using an online rebuild cost estimator.

3. Confirm solar panel coverage Solar systems can represent tens of thousands of dollars in value. Verify that your policy covers the panels for both accidental damage and storm events, and check whether the inverter and battery (if applicable) are included.

4. Compare quotes before renewing Given that Cargo's 25th percentile sits at $1,257/yr, there's a reasonable chance a comparable policy is available at a lower price point. Insurers don't always reward loyalty — comparing quotes at renewal is one of the simplest ways to reduce your premium without reducing your cover.

---

Ready to Find a Better Deal?

Whether you're happy with your current quote or looking to see what else is out there, comparing policies is always worth doing. CoverClub makes it easy to benchmark your premium against real data from your suburb and beyond. Get a home insurance quote today and see how your premium stacks up.