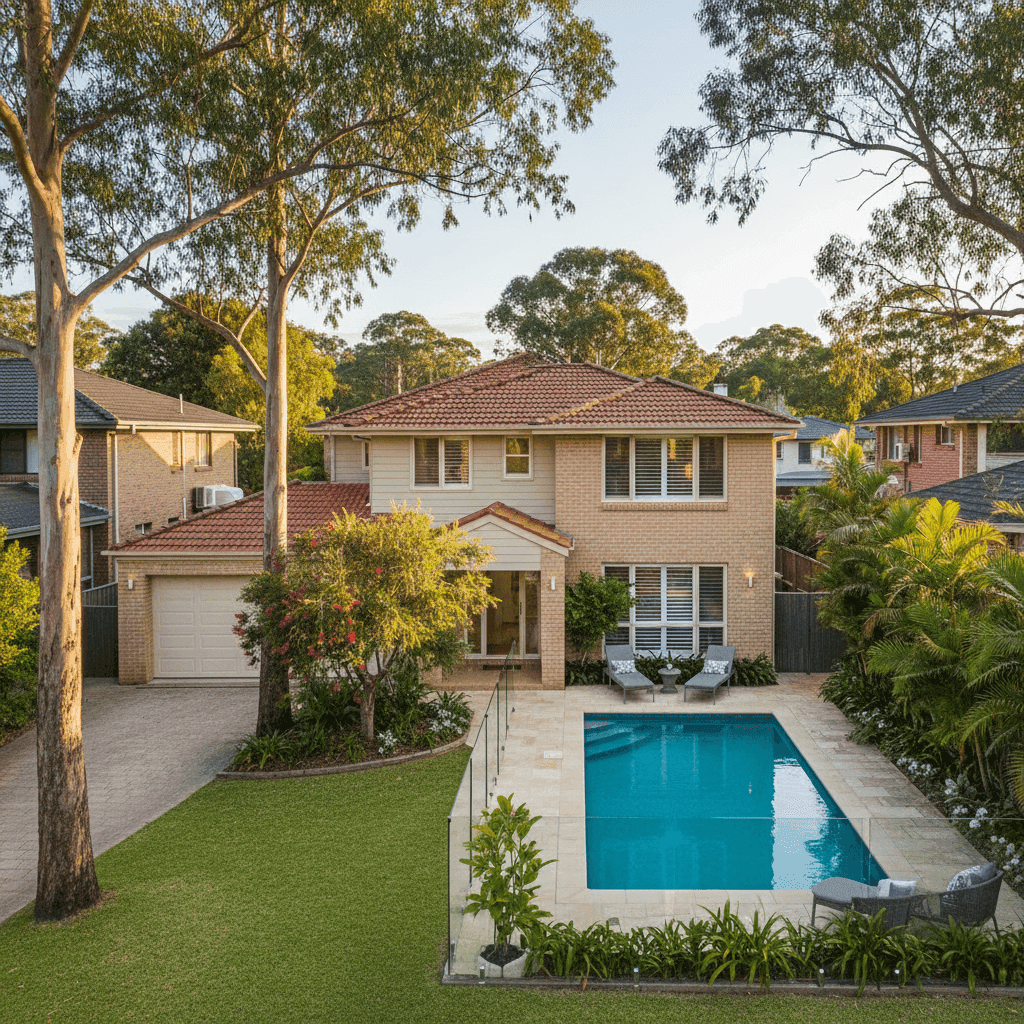

If you own a free standing home in Carina Heights, QLD 4152, you've probably wondered whether you're paying a fair price for home and contents insurance — or quietly overpaying year after year. This article breaks down a real insurance quote for a four-bedroom, three-bathroom home in the suburb, and puts the numbers into context using local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property comes in at $3,645 per year (or $349/month), covering both building and contents. The building is insured for $916,000, with $125,000 in contents cover. Both the building and contents excess are set at $500 each.

Our price rating for this quote is FAIR — Around Average, which is an honest and useful result. It means the premium isn't a bargain, but it's also not cause for alarm. The homeowner is sitting comfortably within the typical range for the area, which is reassuring given the size and age of the property.

That said, "fair" doesn't mean "the best available." There's always room to compare, and even a modest saving of a few hundred dollars per year adds up significantly over the life of a mortgage.

---

How Carina Heights Compares

To understand whether this quote represents good value, it helps to look at the broader picture. Here's how the $3,645 annual premium stacks up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $3,645/yr |

| Carina Heights Suburb Average | $3,218/yr |

| Carina Heights Suburb Median | $3,061/yr |

| Carina Heights 25th Percentile | $2,292/yr |

| Carina Heights 75th Percentile | $3,984/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| Brisbane LGA Average | $16,277/yr |

(Based on 26 quotes sampled for the Carina Heights area.)

A few things stand out here. First, this quote sits above the suburb average and median, but still below the 75th percentile for the area — meaning roughly three-quarters of comparable properties in Carina Heights are paying less, but a significant portion are paying more. The homeowner is in the upper-middle band for the suburb.

Second, when you zoom out to the state level, the picture looks far more favourable. Queensland's average premium is a striking $9,129 per year, heavily skewed by high-risk areas in regional and coastal QLD — think cyclone-prone Far North Queensland and flood-affected inland regions. The QLD state average reflects just how expensive insurance can be in parts of this state. Against that backdrop, $3,645 looks quite reasonable.

Similarly, the national average sits at $5,347, again pulled upward by high-risk postcodes across the country. At the national median of $2,764, this quote is above the midpoint — but the national median includes many lower-risk, lower-value properties that aren't directly comparable to a 235 sqm double brick home with a pool.

The Brisbane LGA average of $16,277 is a striking figure, but it's important to note this is heavily influenced by flood-affected suburbs within the LGA. Carina Heights, being a relatively elevated suburb, benefits from a more favourable risk profile compared to low-lying Brisbane areas. You can explore more local data on the Carina Heights suburb stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular home play a meaningful role in how the insurer has priced the risk.

Double Brick Construction Double brick walls are generally viewed favourably by insurers. They offer strong resistance to fire, impact, and weather events, which can reduce the likelihood of a major claim. This is a genuine asset when it comes to pricing.

Tiled Roof Terracotta or concrete tiles are a common roofing choice in Brisbane's older suburbs. They're durable and perform well in storms, though they can be susceptible to cracking under hail. Overall, a tiled roof on a well-maintained home tends to be neutral to slightly positive from an insurance perspective.

Slab Foundation A concrete slab foundation is generally considered low-risk. Unlike homes on stumps or piers, slabs offer little opportunity for subsidence or pest-related structural damage, which insurers appreciate.

Construction Year: 1979 At over 45 years old, this home is considered an established property. Older homes can attract slightly higher premiums due to ageing plumbing, wiring, and roofing materials, though double brick construction tends to age well. Keeping up with maintenance is key to managing this risk factor.

Swimming Pool A pool adds to the replacement cost of the property and introduces a degree of liability exposure. It's a contributing factor to the building sum insured and will have a modest upward effect on the premium.

Ducted Climate Control Ducted air conditioning is a meaningful inclusion in the building sum insured. These systems are expensive to replace and are factored into the $916,000 building valuation.

Building Size: 235 sqm At 235 sqm, this is a substantial family home. The building sum insured of $916,000 works out to roughly $3,898 per sqm — broadly in line with current construction costs in Brisbane for a quality double brick build with standard fittings.

---

Tips for Homeowners in Carina Heights

1. Review Your Building Sum Insured Regularly Construction costs in Brisbane have risen sharply over the past few years. If your sum insured hasn't been updated recently, you could be underinsured — meaning a total loss payout might not fully cover a rebuild. Use a building cost calculator or speak to a local builder to sense-check your figure annually.

2. Bundle Building and Contents for Potential Savings This quote already combines building and contents cover, which is a smart move. Many insurers offer discounts for combined policies. If you're currently holding separate policies, it's worth getting a bundled quote to see if consolidation saves you money.

3. Consider Your Excess Level Both excesses are set at $500, which is a standard starting point. Opting for a higher voluntary excess — say $1,000 or $1,500 — can meaningfully reduce your annual premium. If you're unlikely to make small claims, this trade-off often makes financial sense.

4. Compare at Renewal Time Loyalty doesn't always pay in insurance. Premiums can creep up at renewal without a corresponding improvement in cover. Set a reminder to compare quotes on CoverClub at least 30 days before your policy renews, giving yourself time to switch if a better deal is available.

---

Find a Better Deal on CoverClub

Whether you're renewing your existing policy or insuring a new purchase, it pays to compare. CoverClub makes it easy to see what other homeowners in Carina Heights are paying and to get quotes tailored to your specific property. Start your comparison today — it only takes a few minutes and could save you hundreds.