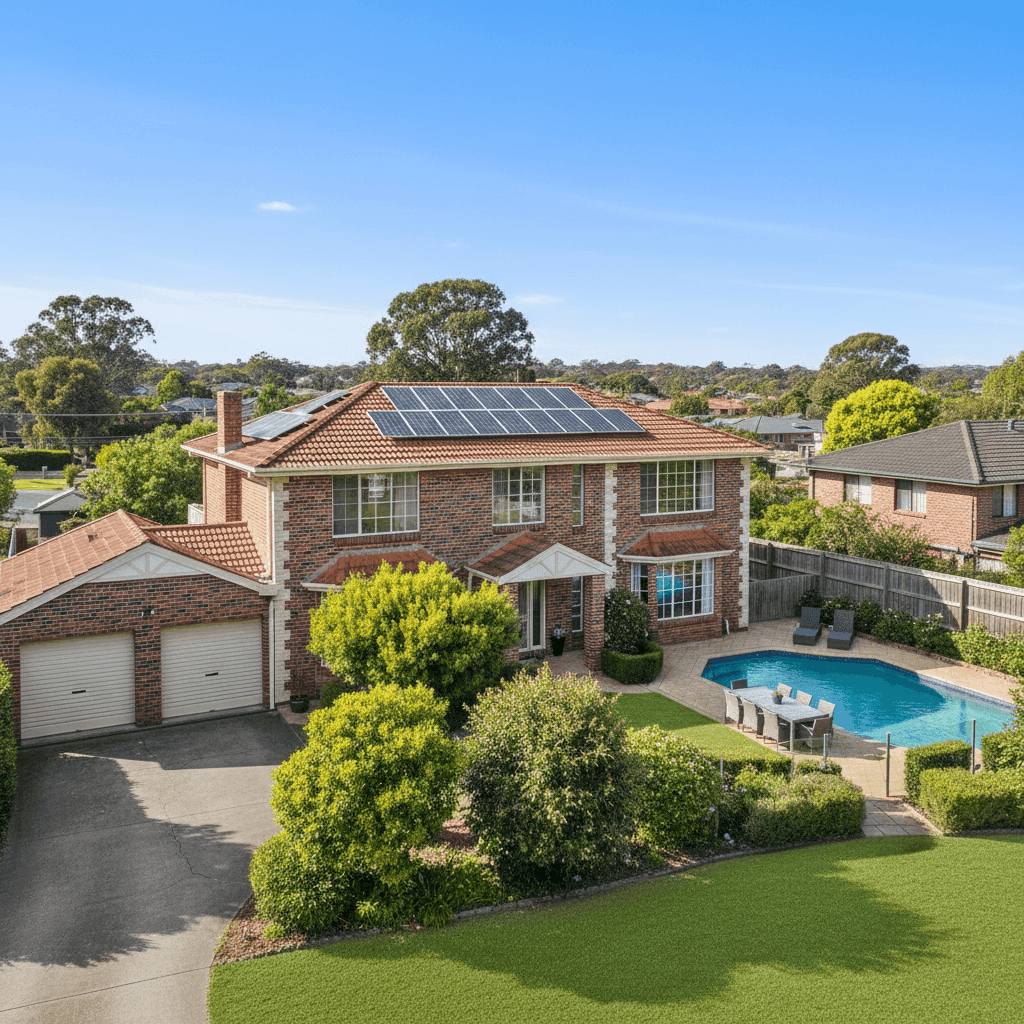

Carlingford is a well-established suburb in Sydney's north-west, sitting within the Hills District and known for its leafy streets, quality schools, and a strong mix of large family homes. This analysis looks at a home and contents insurance quote for a six-bedroom, three-bathroom free standing home in Carlingford, NSW 2118 — a substantial property that comes with a number of features that directly influence what insurers charge.

---

Is This Quote Fair?

The annual premium for this property came in at $3,796 per year (or $371 per month), covering both building and contents. Our price rating for this quote is Expensive — above average when benchmarked against comparable properties in the area.

To put that in context: the suburb average for Carlingford sits at just $1,571 per year, with a median of $1,464. This quote is more than double the local median — a significant gap that warrants a closer look.

That said, it's important not to compare apples with oranges. This is a very large home with a high building sum insured of $1,760,000, a pool, solar panels, and ducted climate control — all features that meaningfully increase replacement costs and, therefore, premiums. The contents cover of $70,000 also adds to the total. When you factor in those variables, the premium starts to make more sense, even if it still sits on the higher end.

The building excess and contents excess are both set at $5,000, which is relatively high. Choosing a higher excess is a common strategy to bring down premiums — so if this quote was generated with that trade-off in mind, the base rate before the excess adjustment could have been even higher.

---

How Carlingford Compares

Understanding where this quote sits relative to broader benchmarks helps frame whether it's competitive or whether there's room to shop around.

| Benchmark | Premium |

|---|---|

| This quote | $3,796/yr |

| Carlingford suburb average | $1,571/yr |

| Carlingford suburb median | $1,464/yr |

| LGA (The Hills) average | $2,440/yr |

| NSW state median | $3,770/yr |

| NSW state average | $9,528/yr |

| National median | $2,764/yr |

| National average | $5,347/yr |

Interestingly, this quote is very close to the NSW state median of $3,770 — which suggests that for a property of this size and value, the pricing is broadly in line with what larger or higher-risk properties across the state are paying. It also sits well below the national average of $5,347, which is heavily influenced by high-risk regions such as Far North Queensland and flood-prone inland areas.

The Carlingford suburb sample size used in this comparison is 20 quotes, which is a reasonable dataset but skewed toward more typical-sized homes. This property is notably larger than average, which explains much of the premium gap versus the suburb figures.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated by insurers. Here's how each one factors in:

Size and Sum Insured

At 447 sqm and a building sum insured of $1,760,000, this is a large home with a high replacement value. Building sum insured is one of the single biggest drivers of premium — the more it costs to rebuild, the more the insurer is on the hook for. Getting this figure right is critical; underinsurance is a common and costly mistake.

Construction: Double Brick Walls and Tiled Roof

Double brick construction is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well over time. A tiled roof similarly signals longevity and lower storm damage risk compared to, say, Colorbond or corrugated iron in certain conditions. These features can work in your favour when it comes to pricing.

Age of Construction (1976)

Built in 1976, this home is approaching 50 years old. Older homes can attract higher premiums due to the increased likelihood of aging plumbing, electrical wiring, and structural components needing attention. Insurers may factor in the cost of bringing materials up to current building codes if a claim requires partial or full reconstruction.

Slab Foundation and Timber/Laminate Flooring

A concrete slab foundation is standard for homes of this era in NSW and doesn't typically raise red flags. Timber and laminate flooring, while attractive, can be more expensive to replace than tiles, which may contribute marginally to the contents or building valuation.

Pool, Solar Panels, and Ducted Climate Control

Each of these extras adds replacement value and liability exposure. A swimming pool introduces public liability considerations — particularly relevant for families with visitors or tenants. Solar panels increase the rebuild cost and can be damaged by hail or storms. Ducted climate control systems are expensive to replace and are factored into the building sum insured. All three features are legitimate reasons for a premium to sit higher than a comparable home without them.

---

Tips for Homeowners in Carlingford

1. Review your building sum insured regularly Construction costs have risen sharply in recent years. If your sum insured hasn't been updated to reflect current rebuild costs per square metre in Sydney's north-west, you could be underinsured — or overpaying for a figure that's no longer accurate. Consider getting a professional building valuation every few years.

2. Consider the excess trade-off carefully This quote carries a $5,000 excess on both building and contents. While a higher excess reduces your premium, it also means you'll need to cover the first $5,000 of any claim out of pocket. Make sure this aligns with your financial buffer — and compare what a $1,000 or $2,500 excess would cost annually to see if the savings are worth it.

3. Bundle strategically, but still compare Many insurers offer discounts for combining home and contents cover under one policy. This quote does exactly that. However, bundling doesn't always guarantee the best deal — it's worth getting separate quotes as well to ensure you're not paying a premium for the convenience of a single policy.

4. Don't overlook pool and solar-specific cover Confirm that your policy explicitly covers the pool, solar panel system, and ducted air conditioning as part of the building sum insured. Some policies have sub-limits or exclusions for these items. Reading the Product Disclosure Statement (PDS) carefully — particularly the definitions of "building" — can save a nasty surprise at claim time.

---

Compare Your Options at CoverClub

Whether this quote looks right for your situation or you're wondering if there's a better deal out there, CoverClub makes it easy to see what the market looks like for your specific property. Get a home insurance quote today and compare options side by side — it only takes a few minutes and could save you hundreds. You can also explore Carlingford-specific insurance data to see how your premium stacks up against your neighbours.