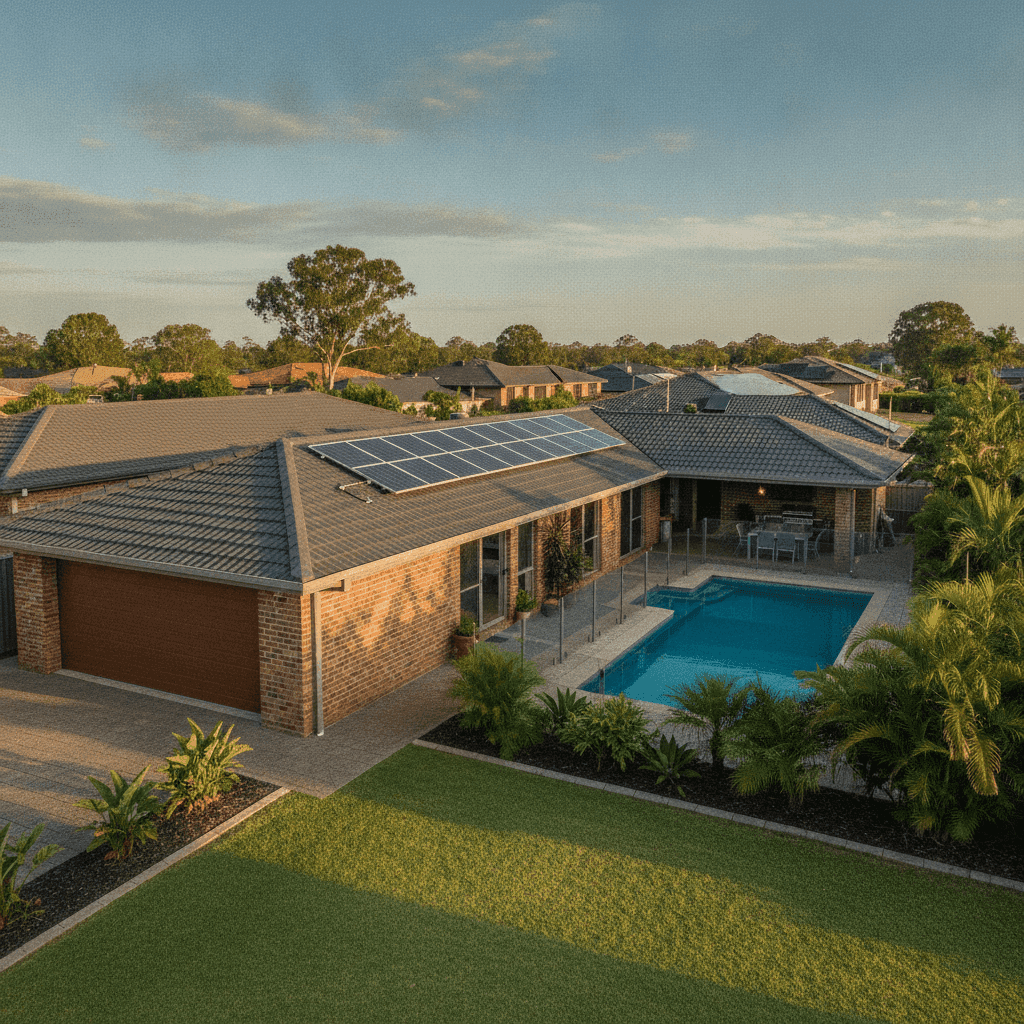

If you own a free standing home in Carrara, QLD 4211, you're sitting in one of Queensland's more sought-after pockets — a leafy suburb on the Gold Coast hinterland fringe, close to Robina Town Centre and the M1. But desirable real estate doesn't always mean affordable insurance. In this article, we break down a real home and contents insurance quote for a three-bedroom, two-bathroom brick veneer home in Carrara, and put the numbers in context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,521 per year (or $242/month) for combined home and contents cover, with a building sum insured of $675,000 and contents valued at $31,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is CHEAP — below average for the area. That's a meaningful result. Based on 37 quotes sampled for Carrara (postcode 4211), the suburb average premium sits at $4,550 per year, and the median is $3,759. This quote beats even the 25th percentile of $2,769 — meaning it's priced more competitively than at least 75% of quotes we've seen for comparable properties in the suburb.

For a property built in 1985 with a pool, solar panels, and ducted climate control — all features that can nudge premiums upward — landing below the suburb's lower quartile is a genuinely strong result.

---

How Carrara Compares

To appreciate just how competitive this quote is, it helps to zoom out and look at the broader pricing landscape.

| Benchmark | Premium |

|---|---|

| This quote | $2,521/yr |

| Carrara suburb average | $4,550/yr |

| Carrara suburb median | $3,759/yr |

| Carrara 25th percentile | $2,769/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| Scenic Rim LGA average | $8,744/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, Queensland's state average of $9,129 is extraordinarily high — driven by cyclone-prone northern and coastal regions where insurers price in significant catastrophe risk. Carrara, however, is not classified as a cyclone risk area, which is a major factor keeping local premiums more manageable.

Second, the national average of $5,347 is more than double this quote — though the national median of $2,764 is a closer comparison point and still slightly above what's been quoted here. The Scenic Rim LGA average of $8,744 is notably elevated, likely pulled up by rural and bushfire-exposed properties in that broader region, making Carrara's suburban profile a relative bright spot.

The takeaway: this is a well-priced quote by almost any measure.

---

Property Features That Affect Your Premium

Every insurer weighs up the specific characteristics of your home when calculating risk. Here's how the features of this particular property play into the pricing picture:

Brick veneer construction and tiled roof Brick veneer walls paired with a tile roof are generally viewed favourably by insurers. Both materials offer solid fire resistance and durability compared to, say, weatherboard or Colorbond. This combination tends to attract lower premiums than lightweight or older construction types.

Slab foundation A concrete slab foundation is standard for homes of this era in Queensland and doesn't introduce elevated risk the way a raised timber subfloor might (which can be more susceptible to moisture and pest damage).

Built in 1985 At around 40 years old, this home is at a point where some insurers start paying closer attention to the age of plumbing, electrical wiring, and roofing. That said, 1985-era brick veneer homes are well understood by the market and generally well-regarded — particularly if maintained in good condition.

Swimming pool A pool adds liability exposure and increases the replacement cost of the property, which can push premiums up modestly. It also adds to the overall sum insured calculation.

Solar panels Rooftop solar is increasingly common, but it does add to the insured value of the home. Panels can be damaged by hail, storms, or fire, and quality insurers will cover them under the building policy. It's worth confirming your policy explicitly includes solar panel cover.

Ducted climate control Ducted air conditioning is a significant fixed asset in the home and contributes to the building sum insured. It's a common feature in Gold Coast homes given the subtropical climate.

Standard fittings, carpet flooring Standard-quality fittings and carpet flooring keep the replacement cost estimate grounded — high-end finishes like stone benchtops or hardwood floors would increase the sum insured and, in turn, the premium.

169 sqm building size At 169 square metres, this is a comfortably sized family home. The building sum insured of $675,000 works out to roughly $3,994 per square metre — a reasonable figure for a brick veneer home with a pool and solar in the current construction cost environment.

---

Tips for Homeowners in Carrara

Whether you're reviewing an existing policy or shopping around for the first time, here are some practical steps worth taking:

1. Don't underinsure your building Construction costs have risen sharply across Australia in recent years. Make sure your sum insured reflects what it would actually cost to rebuild your home today — not what you paid for it or what it's worth on the market. Tools like the Cordell Sum Sure Calculator can help, and many insurers offer a building cost estimator at the point of quote.

2. Check your solar panels are explicitly covered Not all policies automatically include solar panels as part of the building cover. Review your Product Disclosure Statement (PDS) to confirm panels, inverters, and associated wiring are listed. If they're not, ask your insurer to add them.

3. Review your contents sum insured annually $31,000 in contents cover is on the lower side for a three-bedroom home. Do a room-by-room audit of your belongings — furniture, appliances, clothing, electronics, and white goods — to make sure you're not underinsured. Many Australians discover they're significantly short when they actually make a claim.

4. Compare quotes at renewal, not just when you first buy Insurance premiums can shift considerably from year to year. Even if you're happy with your current insurer, it pays to run a comparison before auto-renewing. The difference between the cheapest and most expensive quotes in Carrara spans more than $3,000 per year — that's a meaningful saving to leave on the table.

---

Find Out What You Should Be Paying

Whether this quote reflects your own situation or you're simply trying to benchmark what's reasonable for a home in Carrara, the best move is to compare. Premiums vary widely between insurers for the same property, and the only way to know you're getting a fair deal is to look at multiple options side by side.

Get a home insurance quote at CoverClub and see how your premium stacks up against real data from your suburb. It takes just a few minutes, and you might be surprised by what you find.