If you own a free standing home in Casino, NSW 2470, you're probably well aware that insurance costs in regional New South Wales can vary enormously — and not always in your favour. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom brick veneer home in Casino, comparing it against suburb, state, and national benchmarks to help you understand whether you're getting a fair deal.

---

Is This Quote Fair?

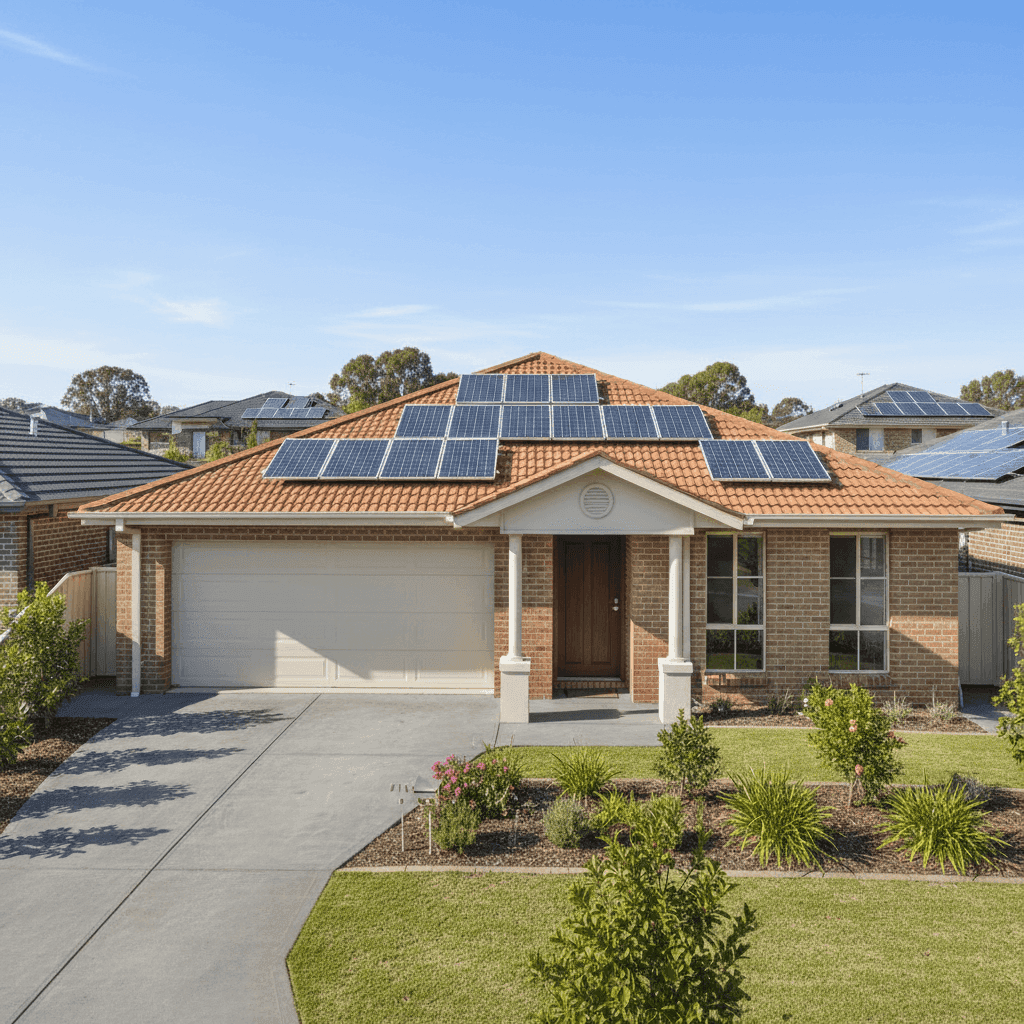

The quote in question comes in at $4,079 per year (or $391 per month) for combined home and contents cover, with a building sum insured of $963,000 and contents valued at $50,000. The building excess is $1,000 and the contents excess is $2,000.

Our price rating for this quote is FAIR — Around Average, which means it sits comfortably within the typical range for the area. Specifically, it falls just below the suburb's 75th percentile of $4,411/yr, meaning roughly three-quarters of comparable quotes in Casino come in at a similar price or lower. That's a reasonable position to be in — not the cheapest on the market, but far from the most expensive either.

Given the property's above-average fittings quality, 244 sqm of floor space, ducted climate control, and solar panels, a slightly elevated premium is to be expected. These features increase both the rebuild cost and the complexity of any claim, which insurers naturally price into their calculations.

---

How Casino Compares

To properly contextualise this quote, it helps to zoom out and look at the broader data. Based on quotes collected for Casino NSW 2470, the local figures tell an interesting story:

| Benchmark | Premium |

|---|---|

| Casino suburb average | $15,364/yr |

| Casino suburb median | $2,695/yr |

| Casino 25th percentile | $1,916/yr |

| Casino 75th percentile | $4,411/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Lismore LGA average | $18,453/yr |

A few things stand out immediately. The suburb average of $15,364/yr is dramatically higher than the median of $2,695/yr — a clear sign that the Casino market contains a wide spread of quotes, with some very high-cost properties pulling the average upward. This is a common pattern in flood-affected regions of northern NSW, where a subset of properties carries extreme risk and commands eye-watering premiums.

The quote at $4,079/yr sits well above the suburb median but below the 75th percentile, suggesting this property occupies a moderate risk tier — not among the cheapest to insure, but nowhere near the high-risk outliers inflating that average figure.

Compared to NSW state-wide data, this quote is slightly above the state median of $3,770/yr but well below the state average of $9,528/yr. Against national benchmarks, it's also above the national median of $2,764/yr but comfortably under the national average of $5,347/yr.

The Lismore LGA average of $18,453/yr is particularly striking, and reflects the significant flood risk that has reshaped the insurance landscape across this region following major flood events in recent years. That this property's quote sits far below the LGA average is a positive indicator.

---

Property Features That Affect Your Premium

Several characteristics of this home play a meaningful role in how insurers assess and price the risk:

Brick veneer construction with a tiled roof is generally viewed favourably by insurers. Brick veneer offers solid fire resistance and structural durability, while tiled roofs are considered more resilient than Colorbond or corrugated iron in many risk assessments. Together, these features can help moderate premiums compared to timber-framed or clad alternatives.

Slab foundation is standard for homes built in this era and region, and typically doesn't attract any additional loading. However, in areas with expansive clay soils — which are common across northern NSW — insurers may factor in some subsidence risk.

Solar panels add value to the property and increase the sum insured, which flows through to a higher premium. They also introduce a specific risk category (electrical faults, storm damage to panels) that some insurers price separately. It's worth checking whether your policy explicitly covers solar panel damage and at what limit.

Ducted climate control is another above-average fitting that contributes to the higher-than-median sum insured of $963,000. Systems like these are expensive to repair or replace, and their presence signals a well-appointed home that costs more to reinstate.

Above-average fittings quality broadly means the home features premium fixtures, finishes, and appliances. Insurers use this as a proxy for higher rebuild and replacement costs, which is reflected in both the sum insured and the premium.

The absence of a pool and the property being outside a designated cyclone risk zone are both modest premium positives — fewer liability exposures and no tropical weather loading.

---

Tips for Homeowners in Casino

1. Review your sum insured carefully — and regularly. A building sum insured of $963,000 for a 244 sqm home works out to roughly $3,946/sqm, which is on the higher end but may be justified given above-average fittings. Use a building cost calculator annually to make sure your cover keeps pace with construction cost inflation, which has been significant in recent years.

2. Understand your flood cover status. Casino and the broader Richmond Valley have experienced significant flood events. Before renewing, confirm explicitly whether your policy includes flood cover (not just storm or rainwater damage) and what the excess is for flood-related claims. These details can vary substantially between insurers.

3. Consider a higher excess to reduce your premium. The current building excess of $1,000 is relatively standard. If you have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim, opting for a $2,000 or $2,500 excess could meaningfully reduce your annual premium.

4. Don't let your contents cover fall short. A contents sum of $50,000 is modest for a four-bedroom home with above-average fittings. Take the time to do a room-by-room inventory — furniture, appliances, clothing, electronics, and valuables can add up quickly. Being underinsured on contents is one of the most common and costly mistakes homeowners make.

---

Compare Your Options with CoverClub

Whether this quote is the right one for you depends on more than just the price — policy inclusions, claim handling, and excess structures all matter. The best way to know you're getting genuine value is to compare. Head to CoverClub to run your own quote and see how your current premium stacks up against the market. It takes just a few minutes and could save you hundreds.