If you own a free standing home in Chadstone, VIC 3148, you've probably wondered whether you're paying too much — or too little — for home insurance. This article breaks down a real home and contents insurance quote for a four-bedroom property in the suburb, compares it against local, state, and national benchmarks, and offers practical advice to help you make a more informed decision at renewal time.

---

Is This Quote Fair?

The quote in question sits at $2,439 per year (or $229/month) for combined home and contents cover, with a building sum insured of $950,000 and contents valued at $140,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — Above Average.

To put that in perspective: the average home and contents premium in Chadstone is just $1,251 per year, with a median of $1,298. This quote comes in at roughly 95% above the suburb average — a significant gap that's worth investigating before simply accepting the renewal.

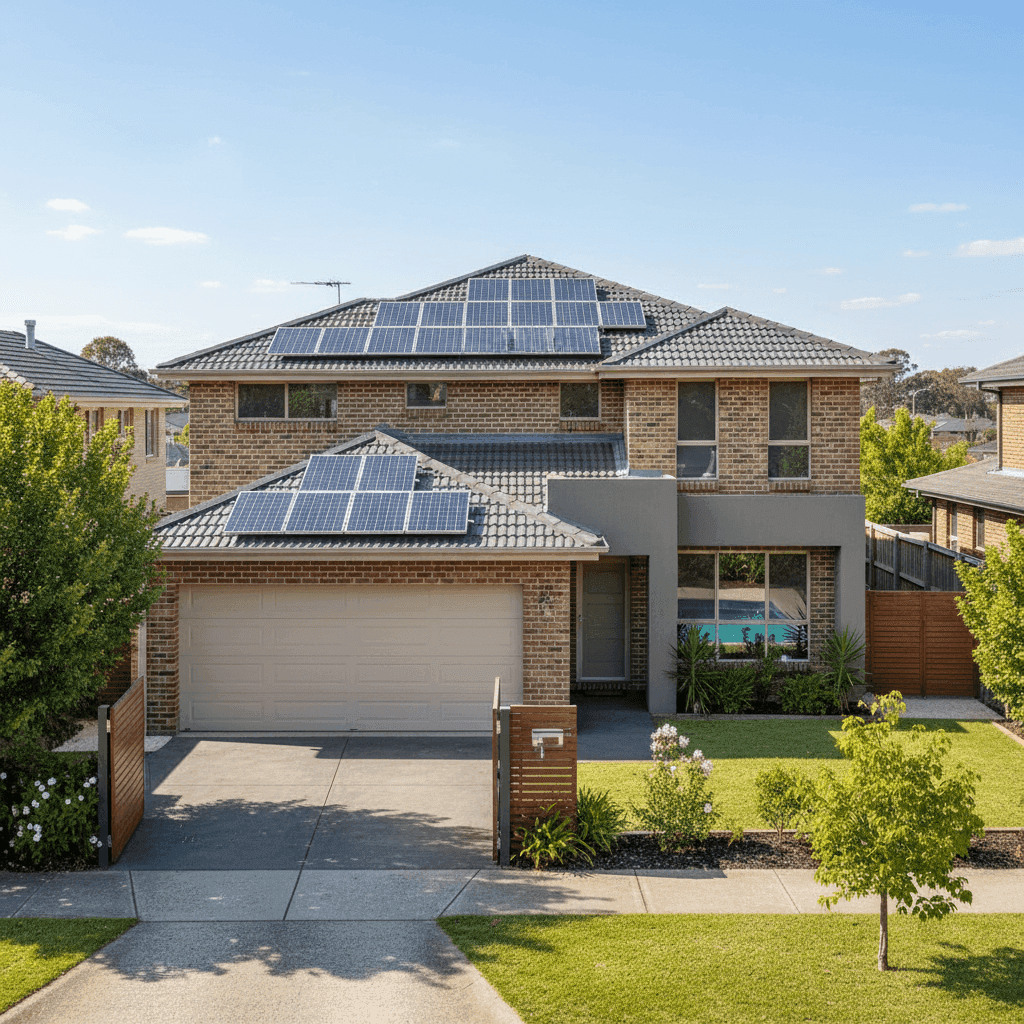

That said, context matters. The property is a well-appointed, 235 sqm brick veneer home built in 2007, featuring above-average fittings, a swimming pool, solar panels, and ducted climate control. Each of these features adds real replacement cost and, in turn, genuine insurance risk. A higher-than-average premium isn't automatically unjustified — but it does warrant scrutiny.

Explore the full Chadstone insurance statistics to see how this quote stacks up against others in the postcode.

---

How Chadstone Compares

Understanding where your premium sits relative to broader benchmarks is one of the most useful tools a homeowner has. Here's how the numbers line up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,439 |

| Chadstone Suburb Average | $1,251 |

| Chadstone Suburb Median | $1,298 |

| Chadstone 25th Percentile | $1,049 |

| Chadstone 75th Percentile | $1,347 |

| LGA (Monash) Average | $1,672 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. While this quote is well above the Chadstone suburb average, it actually sits below both the Victorian state average ($3,000) and the national median ($2,764). This tells a nuanced story: within the local suburb, the quote is on the expensive side, but zooming out to a state or national level, it's not unusual for a property of this size and value.

The Monash LGA average of $1,672 provides a useful middle ground — this quote is still about 46% above that figure, which reinforces that there may be room to shop around.

You can explore Victoria-wide insurance data and national home insurance benchmarks to dig deeper into how location shapes premiums across Australia.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them helps you have a more informed conversation with your insurer — or when comparing alternatives.

Building Size and Sum Insured

At 235 sqm with a building sum insured of $950,000, this is a substantial home. Rebuild costs in metropolitan Melbourne have climbed sharply in recent years due to labour shortages and rising material costs. A higher sum insured means higher premiums, but it's essential to ensure you're not underinsured — which can be far more costly in the event of a total loss.

Brick Veneer Walls and Tiled Roof

Brick veneer construction is generally viewed favourably by insurers — it offers solid fire resistance and durability compared to weatherboard or lightweight cladding. Combined with a tiled roof, this property sits in a lower-risk construction category, which can work in the homeowner's favour when negotiating premiums.

Stump Foundation and Timber/Laminate Flooring

Homes on stumps are more susceptible to certain types of damage — particularly subsidence, pest ingress, and moisture-related issues. Timber and laminate flooring can also be costly to repair or replace following water damage. These factors may contribute to a slightly elevated risk profile in the eyes of underwriters.

Swimming Pool

A pool adds both value and liability to a property. Insurers factor in the cost of pool equipment, surrounds, and fencing, as well as the increased liability risk associated with pool ownership. Ensuring your policy explicitly covers pool-related damage and liability is essential.

Solar Panels

Solar panel systems are increasingly common in Melbourne's southeast, and most modern policies do include them — but coverage limits and conditions vary widely. It's worth confirming whether your policy covers the panels for accidental damage, storm damage, and power surge, and whether the inverter is included.

Above-Average Fittings and Ducted Climate Control

Premium appliances, stone benchtops, high-end cabinetry, and whole-home climate control systems all increase the cost to rebuild or repair. Insurers use fittings quality as a key input when calculating replacement value, so "above average" fittings will always push premiums higher — and rightly so.

---

Tips for Homeowners in Chadstone

Whether you're reviewing your current policy or shopping for a new one, these practical steps can help you get better value without sacrificing coverage.

1. Shop Around at Renewal

Loyalty rarely pays in insurance. Many Australian insurers quietly increase premiums at renewal, banking on inertia. Using a comparison platform like CoverClub to run quotes from multiple insurers takes just a few minutes and can reveal meaningful savings — particularly given this quote is sitting well above the local suburb average.

2. Review Your Sum Insured Carefully

With a building sum insured of $950,000, it's worth verifying this figure against an independent rebuild cost estimate. Overinsuring inflates your premium unnecessarily, while underinsuring can leave you exposed. Many insurers offer online calculators, or you can engage a quantity surveyor for a more precise figure.

3. Check Pool and Solar Panel Coverage Explicitly

Don't assume these are covered — read the Product Disclosure Statement (PDS) carefully. Some policies cap solar panel cover at a low dollar figure, and pool equipment (pumps, filters, heating systems) may be excluded or subject to separate limits. Ask your insurer directly if you're unsure.

4. Consider Your Excess Strategy

Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess — say, $2,000 or $2,500 — can meaningfully reduce your annual premium. This is a sensible strategy if you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim.

---

Ready to Compare?

If this quote has you questioning whether you're getting the best deal, you're not alone. Home insurance pricing varies enormously between insurers — even for identical properties. At CoverClub, we make it easy to compare home and contents quotes side by side, so you can see exactly where your money is going.

Get a home insurance quote for your Chadstone property and find out whether you could be paying less for the same — or better — cover.