Chadstone, VIC 3148 — best known for its iconic shopping centre — is also home to a mix of well-established residential streets lined with quality family homes. This analysis takes a close look at a home and contents insurance quote for a four-bedroom, two-bathroom free-standing home in the suburb, breaking down whether the price stacks up and what factors are likely driving the premium.

---

Is This Quote Fair?

The quoted annual premium for this property comes in at $2,162 per year (or $211 per month), covering both building and contents. The building is insured for $1,060,000, with contents valued at $120,000, and both building and contents excesses are set at $2,000.

Based on CoverClub's pricing data, this quote is rated Expensive — Above Average for the area. To put that in perspective, the suburb average premium in Chadstone sits at just $1,251 per year, with a median of $1,298. That means this quote is running roughly 73% above the suburb average — a notable gap that warrants a closer look.

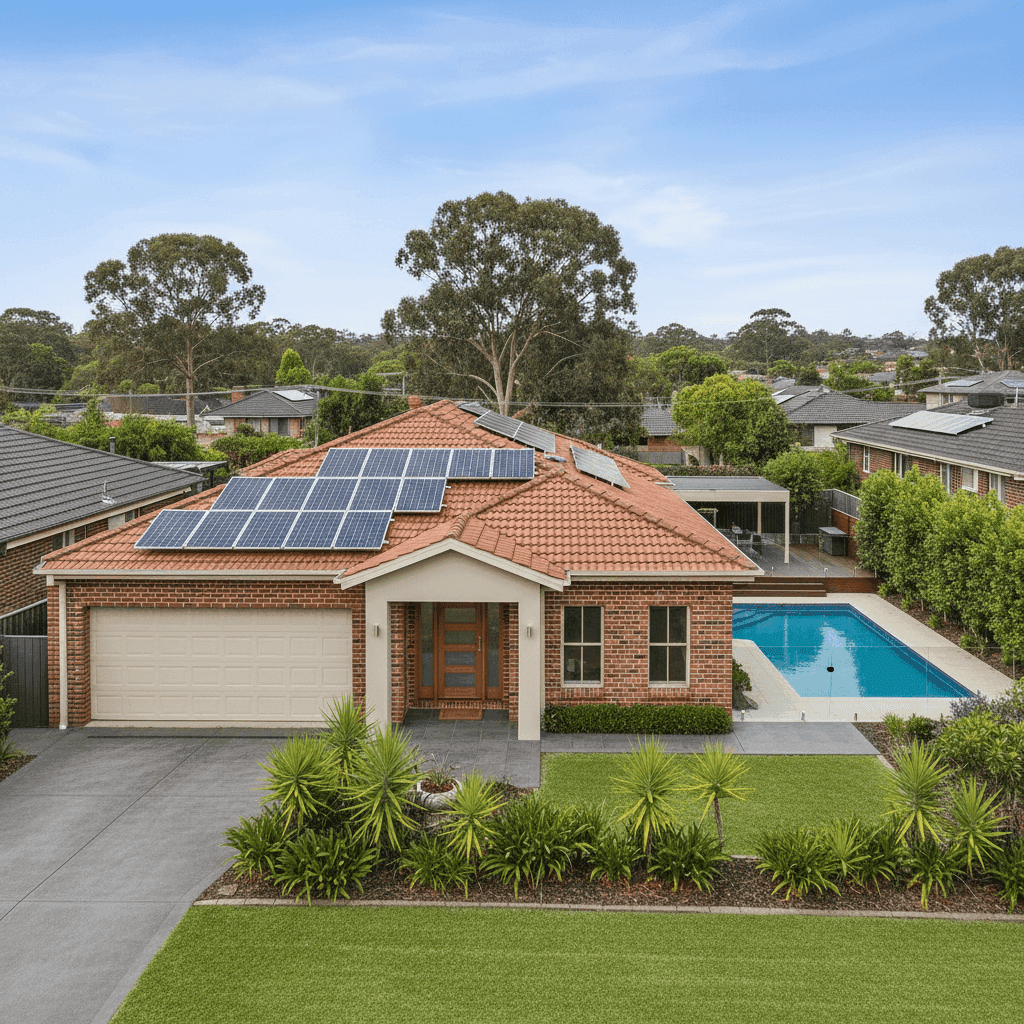

That said, "expensive" doesn't automatically mean "wrong." Several features of this particular property — including its above-average fittings, swimming pool, solar panels, and ducted climate control — can meaningfully push a premium higher than a more modest home nearby. The high building sum insured of $1,060,000 for a 235 sqm home also reflects the above-average construction and finish quality, and insurers price accordingly.

Still, if you haven't recently shopped around, it's well worth comparing quotes to ensure you're not overpaying for the same level of cover. You can see live Chadstone insurance stats and quotes here.

---

How Chadstone Compares

Understanding where your premium sits relative to broader benchmarks is key to assessing value. Here's how Chadstone stacks up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Chadstone (3148) | $1,251/yr | $1,298/yr |

| LGA (Monash) | $1,672/yr | — |

| Victoria | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. Chadstone's suburb-level premiums are significantly lower than the Victorian state average, which reflects the area's relatively low natural hazard risk profile — no cyclone exposure, manageable flood risk, and a well-serviced urban environment.

Compared to the national average of $5,347 per year, Chadstone homeowners are generally in a favourable position. Even this "expensive" quote at $2,162 sits well below the national average, which is skewed upward by high-risk regions in Queensland and Western Australia.

The LGA average for Monash ($1,672/yr) falls between the suburb figure and the state figure, suggesting that while Chadstone itself is relatively affordable to insure, some neighbouring suburbs in the Monash council area attract higher premiums.

Explore Victoria-wide home insurance data or national benchmarks to see how other areas compare.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to a premium above the suburb average. Here's what insurers are probably factoring in:

Above-Average Fittings Quality Kitchens with stone benchtops, premium appliances, quality bathroom fixtures, and high-end flooring all cost more to repair or replace. Insurers assess fittings quality when calculating rebuild costs, and above-average fittings can add a meaningful amount to the sum insured — and therefore the premium.

High Building Sum Insured ($1,060,000) For a 235 sqm home built in 2007 with quality finishes, a $1,060,000 building sum insured is substantial. This figure reflects the full cost to rebuild the home to the same standard — not its market value. Accurate sum insured figures are critical; being underinsured can leave you badly exposed at claim time.

Swimming Pool Pools add liability exposure and can be costly to repair or replace if damaged by an insured event. Most insurers include pool coverage but factor it into the overall premium.

Solar Panels Rooftop solar systems are increasingly common in Melbourne's south-east, but they do add to the replacement cost of the building. A quality system on a 235 sqm home can represent a significant asset that needs to be covered.

Ducted Climate Control Ducted heating and cooling systems are expensive to replace and are typically included in the building sum insured. Their presence contributes to a higher rebuild cost estimate.

Brick Veneer Walls & Tiled Roof These are generally considered low-to-moderate risk construction types in Victoria — brick veneer is resilient and widely used, while tiles are a standard, durable roofing material. These features are unlikely to be inflating the premium; if anything, they may be keeping it in check compared to homes with timber cladding or older roofing materials.

Stump Foundation & Timber/Laminate Flooring Homes on stumps can be more susceptible to certain types of movement or moisture damage, which some insurers may price into their risk assessment. Timber and laminate flooring, while premium in finish, can be costly to repair following water damage events.

---

Tips for Homeowners in Chadstone

1. Review Your Sum Insured Regularly Building costs have risen sharply in recent years. If your home was last valued for insurance purposes several years ago, it may be worth using an independent building calculator or speaking with a quantity surveyor to confirm your sum insured is still adequate. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Compare Quotes Before Renewal With this quote sitting above the suburb average, it's a strong reminder to shop around at renewal time. Premiums can vary significantly between insurers for the same property — sometimes by hundreds of dollars. Use a comparison tool like CoverClub to see multiple quotes side by side.

3. Consider Your Excess Level Both the building and contents excess on this policy are set at $2,000. Opting for a higher excess is one of the most straightforward ways to reduce your annual premium. If you have a financial buffer and are unlikely to make small claims, a higher excess can deliver meaningful savings over time.

4. Check What's Included for Your Pool and Solar Not all policies treat pools and solar panels the same way. Some include them automatically in the building sum insured; others require them to be specifically listed. Review your Product Disclosure Statement (PDS) carefully to confirm both are adequately covered — and that your sum insured accounts for their replacement cost.

---

Ready to Compare?

Whether you're renewing your existing policy or insuring a new home in Chadstone, it pays to know what others in your suburb are paying. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property — so you can make a confident, informed decision.