Chapel Hill is a leafy, elevated suburb in Brisbane's western corridor, popular with families drawn to its bushland setting, quality schools, and quintessentially Queensland character homes. If you own a free standing home here — particularly one of the older weatherboard Queenslanders on stumps — understanding what you should be paying for home and contents insurance is well worth your time.

This article breaks down a real insurance quote for a 4-bedroom, 3-bathroom free standing home in Chapel Hill (QLD 4069), compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $2,246 per year (or roughly $215/month) for combined home and contents cover, with a building sum insured of $572,000 and contents valued at $215,000. Both the building and contents excess are set at $5,000.

Our price rating for this quote is FAIR — Around Average.

That assessment is well-supported by the data. The suburb average for Chapel Hill sits at $3,463/yr, with a median of $3,052/yr. This quote lands below both figures, placing it comfortably in the lower half of the pricing range for the area. In fact, the suburb's 25th percentile — meaning 25% of quotes are cheaper — is $2,060/yr, so this quote is only marginally above the cheapest quarter of the market.

In other words, this homeowner is not overpaying. They're getting a competitive rate relative to their neighbours, while still sitting within a realistic range for a property with this profile.

---

How Chapel Hill Compares

To put this quote in proper context, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This Quote | $2,246/yr |

| Chapel Hill Suburb Average | $3,463/yr |

| Chapel Hill Suburb Median | $3,052/yr |

| Brisbane LGA Average | $16,277/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

The figures here tell an interesting story. The QLD state average of $9,129/yr is dramatically inflated by high-risk areas — think flood-prone regions, cyclone-affected coastal towns, and parts of Far North Queensland where premiums can be eye-watering. The Brisbane LGA average of $16,277/yr is similarly skewed by properties in flood corridors or with significant risk profiles.

Chapel Hill, by contrast, is a relatively low-risk suburb. It sits on elevated ground in Brisbane's western hills, is not classified as a cyclone risk area, and generally doesn't carry the same flood exposure as many riverside or low-lying Brisbane suburbs. This is reflected in the suburb's comparatively modest average premium.

Against the national median of $2,764/yr, this quote is actually slightly below — a solid outcome for a property of this size and specification.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on what insurers charge. Here's how they play out:

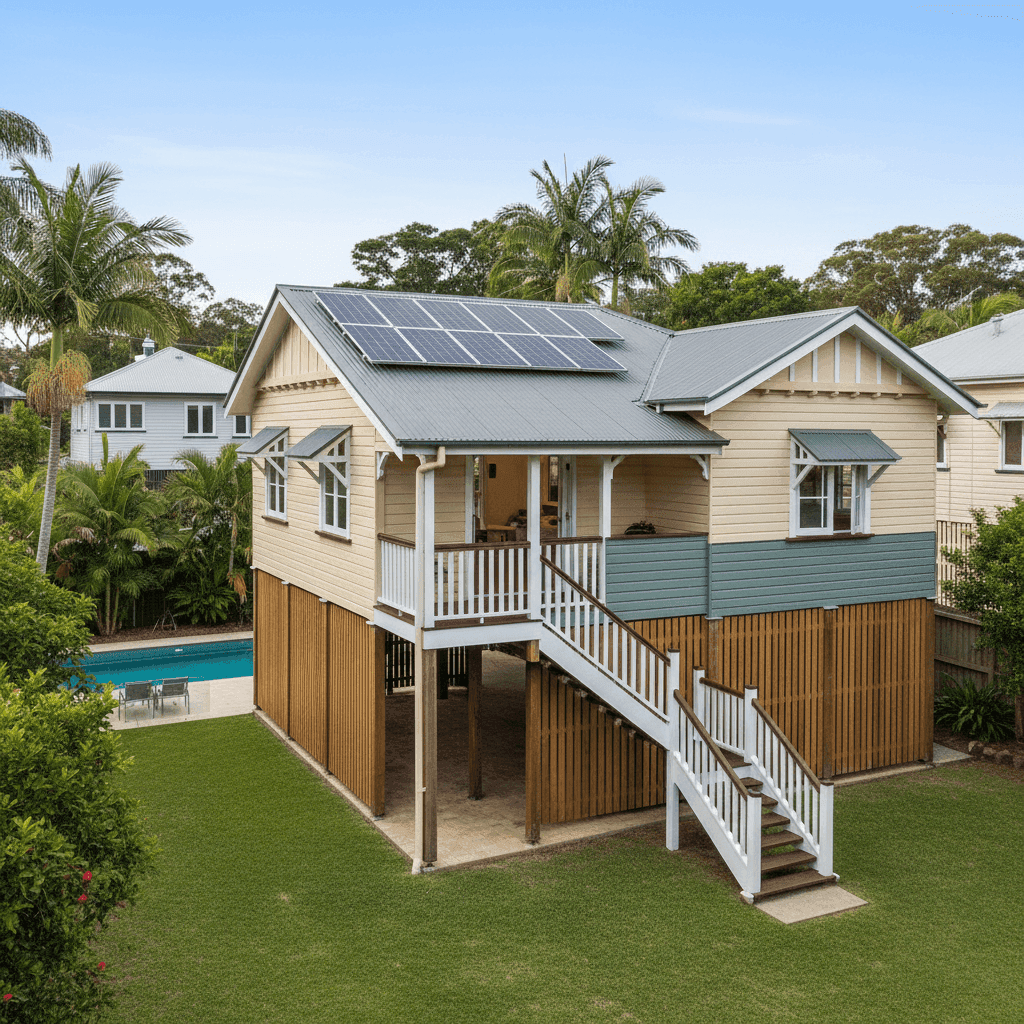

Weatherboard timber walls and timber flooring Weatherboard homes are a staple of Queensland's older suburbs, but timber construction is generally considered higher risk by insurers than brick or rendered masonry. Timber is more susceptible to fire, termite damage, and general wear — all factors that can push premiums upward. Similarly, timber and laminate flooring adds replacement cost to any contents or building claim.

Steel/Colorbond roof This is a positive for insurers. Colorbond roofing is durable, low-maintenance, and performs well in storms compared to terracotta tiles, which can crack or dislodge. It's a common roofing choice in Queensland and generally viewed favourably at assessment time.

Elevated on stumps (at least 1 metre) Being elevated is a double-edged sword. On one hand, it reduces flood risk significantly — water that might inundate a slab-on-ground home flows underneath an elevated Queenslander. On the other hand, stumped homes can be more expensive to repair after storm events, and the subfloor space introduces its own maintenance considerations. Overall, the flood risk reduction is typically a net positive for premiums in Brisbane.

Swimming pool Pools add to the insured value of the property and introduce some liability considerations. They're common in Chapel Hill, and most insurers factor them into building replacement cost calculations.

Solar panels Solar systems are a significant asset — often worth $8,000–$20,000 or more — and need to be properly covered under your building policy. It's worth confirming with your insurer that your panels are included in the sum insured and that the $572,000 building cover accounts for their replacement value.

Ducted climate control Ducted air conditioning is a premium fixture that adds to the cost of rebuilding or reinstating a home. It's a relevant factor in calculating an adequate sum insured.

Construction year: 1991 A home built in 1991 is over 30 years old. While it's not ancient, it may have ageing plumbing, electrical systems, or structural elements that some insurers price accordingly. Regular maintenance and updated systems can help manage this risk.

---

Tips for Homeowners in Chapel Hill

1. Review your sum insured annually With building costs rising sharply across Queensland in recent years, a sum insured set even two or three years ago may no longer reflect the true cost of rebuilding your home. Make sure your $572,000 figure accounts for current labour and materials costs, including your pool, solar system, and ducted air conditioning. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Consider your excess carefully A $5,000 excess on both building and contents is on the higher end. While a higher excess typically reduces your annual premium, it means you'll need to cover the first $5,000 of any claim out of pocket. Think about whether this aligns with your financial buffer, particularly for contents claims that might be smaller in value.

3. Shop the market at renewal time Even with a fair quote, it pays to compare. Insurers reprice risk constantly, and loyalty doesn't always translate to the best deal. Use CoverClub's free comparison tool at renewal time to see what else is available for your specific property.

4. Maintain your timber home proactively For weatherboard homes, regular maintenance — repainting, termite inspections, checking stumps and subfloor — not only protects your asset but can support your insurance position. Some insurers may reduce cover or apply exclusions for damage they deem the result of gradual deterioration or lack of maintenance.

---

Get a Quote for Your Chapel Hill Home

Whether you're renewing your existing policy or shopping around for the first time, CoverClub makes it easy to compare home and contents insurance quotes tailored to your property. See how your premium stacks up against the latest Chapel Hill suburb data and find cover that works for you.