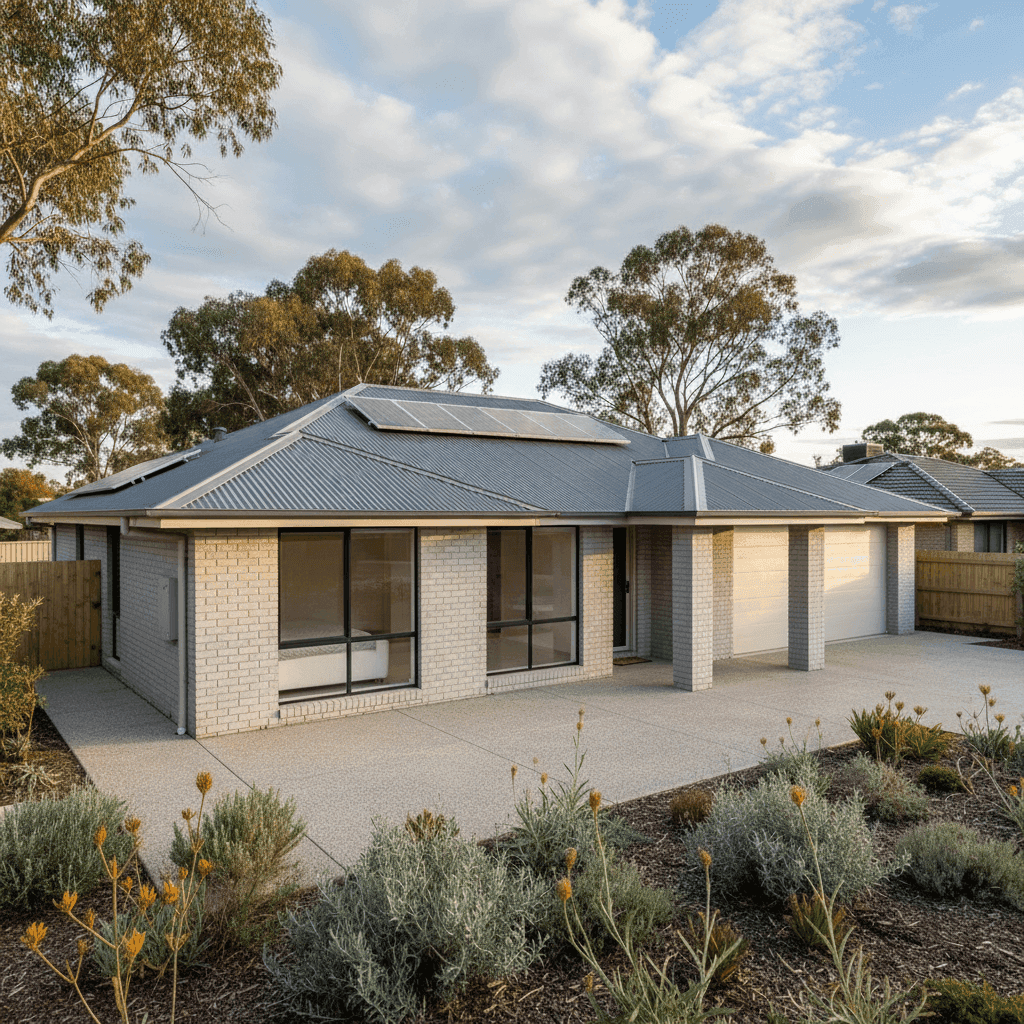

Home insurance costs can vary dramatically depending on where you live, what your home is made of, and how much cover you need. This article takes a close look at a real home and contents insurance quote for a four-bedroom, free standing home in Chiltern, VIC 3683 — a charming historic town in Victoria's Indigo Shire — and benchmarks it against local, state, and national data to help you understand whether the price stacks up.

---

Is This Quote Fair?

The quote in question comes in at $5,188 per year (or $497/month) for combined home and contents cover, with a building sum insured of $901,000 and contents valued at $30,000. The building excess is $2,000 and the contents excess is $1,000.

Based on available market data, this quote is rated Expensive — above average for the area. That doesn't necessarily mean it's wrong, but it does warrant a closer look before accepting it at face value.

The building sum insured of $901,000 is a significant figure and will naturally push the premium higher. For a 214 sqm home built in 2006 with standard fittings, this rebuild value reflects the genuine cost of construction in regional Victoria — materials, labour, and site costs don't come cheap, even outside metro areas. That said, it's always worth verifying your sum insured against an independent building cost estimate to ensure you're not over-insured, which could be quietly inflating your premium.

---

How Chiltern Compares

To put this quote in context, here's how it sits against the broader market:

| Benchmark | Annual Premium |

|---|---|

| This quote | $5,188 |

| Chiltern suburb average | $3,335 |

| Chiltern suburb median | $2,183 |

| Chiltern 75th percentile | $5,049 |

| LGA (Indigo) average | $3,278 |

| VIC state average | $3,000 |

| VIC state median | $2,718 |

| National average | $5,347 |

| National median | $2,764 |

Note: Chiltern suburb data is based on a sample of 16 quotes, so averages should be interpreted with some caution.

A few things stand out here. While this quote sits above the Chiltern suburb average of $3,335 and comfortably above the suburb median of $2,183, it actually falls below the national average of $5,347. Compared to the Victorian state average of $3,000, the quote is noticeably higher — but when you look at the national picture, it's sitting in a fairly typical range for a well-insured, larger home.

The 75th percentile for Chiltern is $5,049, meaning roughly 25% of quotes in the area are priced above that mark — and this quote, at $5,188, sits just above it. So while it's on the higher end locally, it's not wildly out of step with what some Chiltern homeowners are paying.

The key driver here is almost certainly the high building sum insured. A $901,000 rebuild value is substantial and will push any quote towards the upper end of the range, regardless of location.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the premium, both positively and negatively.

Brick Veneer Walls & Colorbond Roof

Brick veneer construction is generally viewed favourably by insurers — it's durable, fire-resistant, and relatively low maintenance. Combined with a steel Colorbond roof, this home has a solid, modern construction profile. Colorbond roofing is particularly well-regarded in regional Victoria for its resilience against hail, wind, and bushfire ember attack.

Concrete Slab Foundation

A slab-on-ground foundation is a common and stable choice for homes built in the 2000s. It reduces the risk of subsidence and structural movement compared to older pier-and-beam foundations, which can be a positive factor in premium calculations.

Solar Panels

This property has solar panels installed. While solar panels are a great investment for energy savings, they do add to the rebuild cost of the home and may increase the sum insured required to cover replacement. Some insurers specifically include or exclude solar panels under their building policies, so it's worth confirming your policy wording covers them.

Ducted Climate Control

Ducted heating and cooling systems add value to a home but also add to its insured replacement cost. A full ducted system can cost tens of thousands of dollars to replace, so having it reflected in your sum insured is important.

Tile Flooring

Tiled floors are a durable, low-risk flooring choice from an insurance perspective. They're resistant to water damage and easier to replace than timber or carpet in many scenarios.

No Pool, No Cyclone Risk

The absence of a swimming pool removes a common source of liability and structural claims. Chiltern is also outside designated cyclone risk zones, which keeps the premium from attracting the significant loadings seen in northern parts of Australia.

---

Tips for Homeowners in Chiltern

1. Review your building sum insured carefully At $901,000, the building sum insured is the single biggest driver of this premium. Use a quantity surveyor or online rebuild cost calculator to verify this figure. If your home can be rebuilt for less, reducing the sum insured (accurately) could meaningfully lower your annual cost.

2. Shop around — and use comparison tools With only 16 quotes in the local sample, the Chiltern market data is limited. Premiums can vary significantly between insurers for the same property. Get a quote at CoverClub to compare multiple options side by side and see whether a better deal is available for your specific circumstances.

3. Consider your excess settings The building excess on this policy is $2,000 and the contents excess is $1,000. Opting for a higher voluntary excess is one of the most straightforward ways to reduce your annual premium — just make sure you're comfortable covering that amount out of pocket in the event of a claim.

4. Check that your solar panels are explicitly covered Given the solar installation on this property, review your policy's product disclosure statement (PDS) to confirm panels are covered under the building section. Some policies treat them as an optional extra or have specific sub-limits. It's a small check that could save significant expense after a storm or fire.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new home, it pays to compare. CoverClub makes it easy for Australian homeowners to benchmark their premiums against real market data and find competitive quotes. Start your comparison today and make sure you're not paying more than you need to for quality home and contents cover.