Chinchilla is a regional Queensland town sitting in the heart of the Western Downs, known for its agricultural heritage and the famous Chinchilla Melon Festival. It's also a suburb where home insurance costs can vary dramatically — as this analysis of a recent quote for a four-bedroom, two-bathroom free standing home will show. If you own or are thinking of insuring a property in the area, understanding what's driving your premium is the first step to making sure you're not overpaying.

---

Is This Quote Fair?

The quote in question comes in at $2,552 per year (or $250 per month) for combined Home and Contents cover, with a building sum insured of $805,000 and contents valued at $70,000. The building excess sits at $2,000, and the contents excess at $1,000.

CoverClub's pricing engine rates this quote as FAIR — Around Average, and when you dig into the numbers, that assessment holds up well. The premium sits comfortably below both the suburb average and the state average, while tracking close to national benchmarks. For a property of this size and specification in regional Queensland, that's a reasonable result — though as we'll explore below, there's still room to potentially do better.

---

How Chinchilla Compares

Home insurance pricing in Chinchilla (postcode 4413) is notably wide-ranging, which is a pattern common in regional Queensland. Based on data from 92 quotes collected for this suburb, here's how the numbers break down:

| Benchmark | Premium |

|---|---|

| This quote | $2,552/yr |

| Suburb 25th percentile | $1,814/yr |

| Suburb median | $2,906/yr |

| Suburb 75th percentile | $13,365/yr |

| Suburb average | $9,328/yr |

| LGA (Western Downs) average | $5,223/yr |

| QLD state average | $4,547/yr |

| QLD state median | $3,931/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

A few things jump out immediately. The suburb average of $9,328 is dramatically higher than the median of $2,906 — a classic sign that a small number of very high premiums (likely properties with elevated flood or storm risk) are pulling the mean upward. This is why the median is often a more useful comparison point for typical homeowners.

At $2,552, this quote comes in below the suburb median, below the Queensland state average of $4,547, and also below the national average of $2,965. It does sit above the suburb's 25th percentile of $1,814, which means roughly a quarter of comparable quotes in the area are cheaper — so there's a possibility a more competitive rate exists, but this one is broadly reasonable for the coverage on offer.

---

Property Features That Affect Your Premium

Insurers don't price every home the same way. The specific characteristics of this property play a meaningful role in where the premium lands.

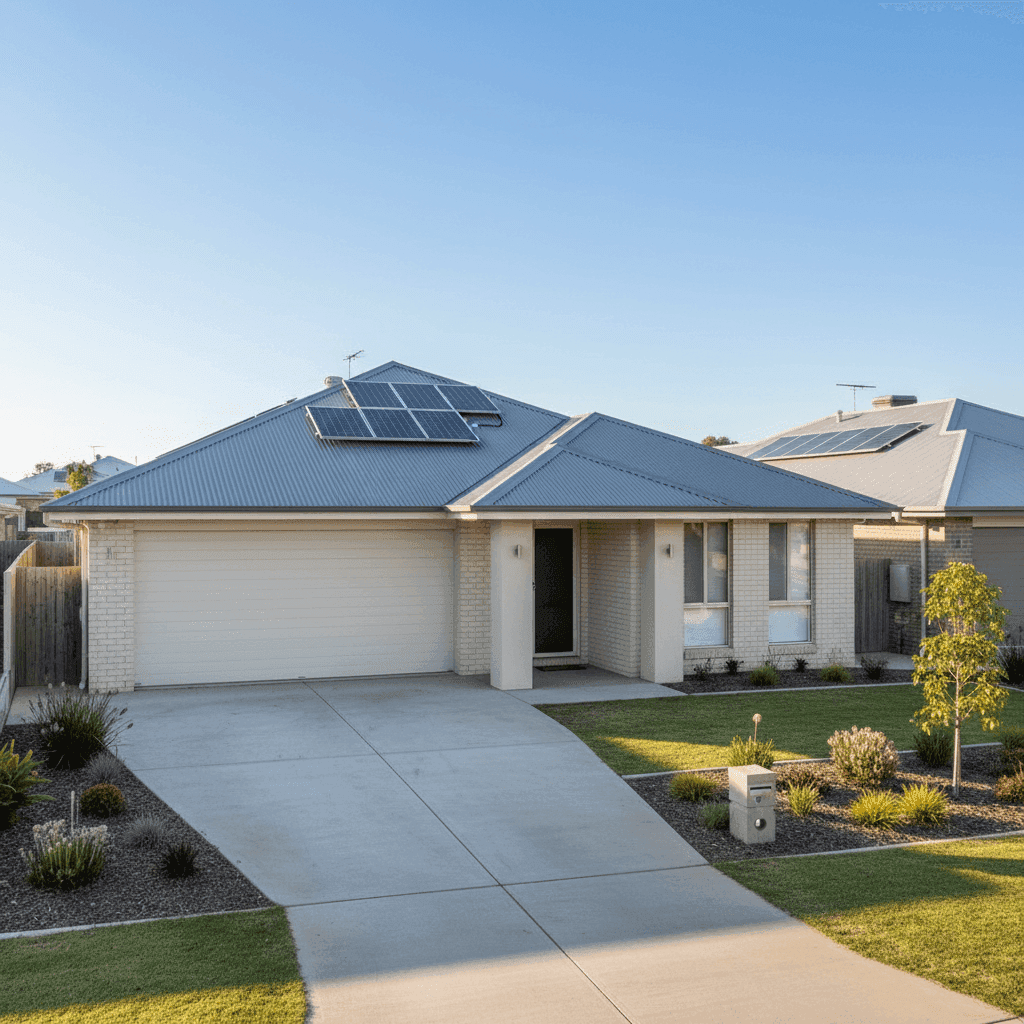

Brick Veneer Walls & Colorbond Roof This combination is generally well-regarded by insurers. Brick veneer offers solid fire resistance and structural durability, while Colorbond steel roofing is lightweight, long-lasting, and performs well in high-wind and hail events. Both materials tend to attract more favourable pricing compared to older or more vulnerable alternatives like weatherboard or terracotta tile.

Slab Foundation A concrete slab is a stable, low-maintenance foundation type that insurers typically view positively. It reduces the risk of subsidence-related claims and is less susceptible to pest damage than elevated timber stumps.

Built in 2015 A relatively modern construction year works in the homeowner's favour. Homes built after significant updates to the Queensland Development Code benefit from improved cyclone and storm engineering standards, better waterproofing, and more compliant electrical systems — all of which reduce claim likelihood.

Solar Panels The property includes rooftop solar, which adds a layer of complexity to building cover. Solar panels increase the replacement value of the home (reflected in the $805,000 sum insured) and can be a source of claims if damaged by hail or storm. It's worth confirming with your insurer that panels are explicitly covered under your building policy.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and is generally covered under building insurance rather than contents. Again, worth verifying the specifics of your policy wording.

Tile Flooring & Standard Fittings Tiled floors are durable and relatively inexpensive to replace, which can moderate contents and building claims. Standard-quality fittings mean the rebuild cost estimate is more predictable, reducing the risk of being underinsured.

No Pool, Not a Cyclone Risk Zone The absence of a pool removes a source of liability and maintenance-related claims. And while Chinchilla sits in inland Queensland, it's not classified as a cyclone risk area — which is a meaningful premium advantage compared to coastal Queensland properties.

---

Tips for Homeowners in Chinchilla

1. Don't rely on the suburb average as your benchmark As the data shows, the Chinchilla average premium of $9,328 is heavily skewed by outlier properties. Your relevant comparison point is the median ($2,906) and your own property's risk profile — not the mean.

2. Review your sum insured annually With a building sum insured of $805,000, it's important to ensure this reflects current rebuild costs — not market value. Construction costs in regional Queensland have risen significantly in recent years. An underinsured property can leave you badly exposed after a major claim.

3. Confirm solar panel and ducted system coverage These are often overlooked in policy reviews. Check whether your solar system is covered for accidental damage, storm damage, and electrical faults — and that your ducted air conditioning is listed as a fixed building fixture.

4. Compare before you renew Insurance loyalty rarely pays off. Premiums can shift significantly year to year, and the spread of quotes in Chinchilla (from $1,814 to $13,365+) shows just how much variation exists. Running a fresh comparison at renewal time is one of the simplest ways to avoid overpaying.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for cover on a new property, CoverClub makes it easy to see how your quote stacks up. Get a home insurance quote now and compare your premium against real data from your suburb, your state, and across Australia — so you can make a genuinely informed decision.