Nestled in the heart of Tasmania's Meander Valley, Chudleigh (TAS 7304) is a quiet rural township known for its heritage character and lush green surrounds. If you own a free standing home here — particularly one of the older weatherboard properties that give the area so much of its charm — understanding what you should be paying for home and contents insurance is well worth your time. This article breaks down a real quote for a 3-bedroom home in Chudleigh and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The short answer: yes — and then some. The quote analysed here comes in at $1,297 per year (or roughly $131 per month), covering both building (sum insured: $400,000) and contents ($20,000). Based on our pricing data, this sits firmly in the "Cheap" category, meaning it is well below the average for comparable homes in the area.

To put that in perspective, the suburb average for Chudleigh is $2,637 per year, and the median sits even higher at $2,726. That means this quote is roughly 51% below the suburb average — a significant saving of over $1,300 annually. Even compared to the 25th percentile of local quotes (i.e., the cheapest quarter of premiums in the area), which sits at $2,214/yr, this quote still undercuts the market considerably.

For a property with a $2,000 building excess and a $600 contents excess, this represents strong value. The higher building excess does play a role in keeping the premium down — you're essentially agreeing to absorb more of any building claim yourself — but even accounting for that, the overall price is notably competitive.

---

How Chudleigh Compares

Understanding your premium means looking beyond just your postcode. Here's how Chudleigh stacks up against broader benchmarks:

| Benchmark | Average Premium |

|---|---|

| Chudleigh (7304) | $2,637/yr |

| Tasmania (TAS) | $2,458/yr |

| National Average | $2,965/yr |

| LGA (West Tamar) | $2,006/yr |

A few things stand out here. Chudleigh's suburb average of $2,637 is actually above the Tasmanian state average of $2,458, suggesting that local risk factors — likely a combination of property age, construction type, and bushfire or flood exposure in the region — push premiums slightly higher than the state norm. Nationally, Tasmanian premiums still come in well below the $2,965 Australian average, which reflects the relatively lower catastrophe risk compared to states like Queensland or Western Australia.

The LGA average for West Tamar ($2,006/yr) is notably lower than Chudleigh's suburb figure, which may indicate that Chudleigh's older housing stock or specific geographic risk profile is nudging local premiums upward within the broader council area.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are worth understanding from an insurance perspective.

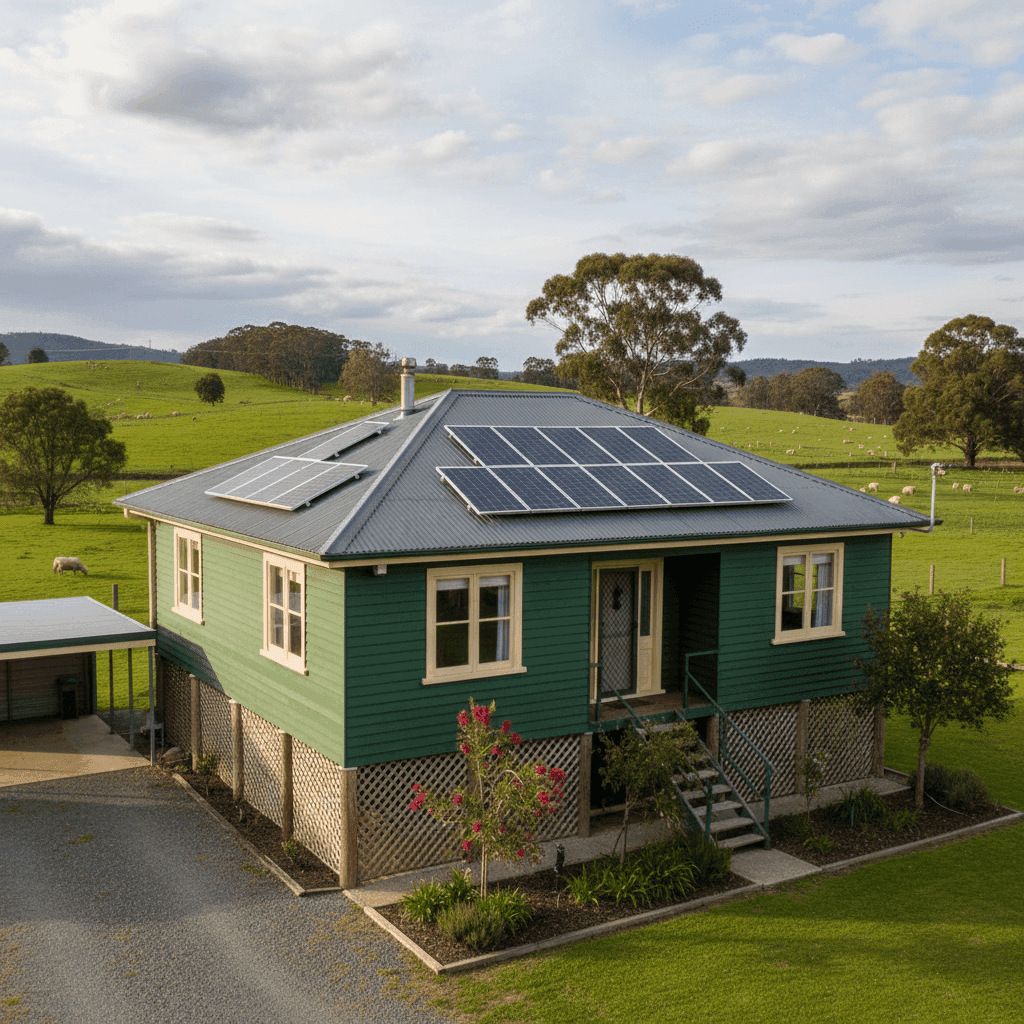

Age and construction (built 1890, weatherboard walls) This is one of the most significant premium drivers for this home. Properties built before Federation are classified as high-risk by most insurers due to the likelihood of outdated wiring, plumbing, and structural wear. Weatherboard timber cladding is also considered more susceptible to fire, rot, and storm damage compared to brick or rendered masonry. Together, these factors would typically push a premium up — making the competitive price here all the more notable.

Roof type: Steel/Colorbond A Colorbond steel roof is generally viewed favourably by insurers. It's durable, low-maintenance, and performs well in high-wind and hail events. This is likely a replacement or upgrade from the original roofing material, and it's a genuine positive for insurability.

Foundation: Stumps Homes on stumps (also called timber piers or posts) are common in older Tasmanian properties. While they allow for good ventilation and can be easier to inspect, they can be more vulnerable to subsidence and pest damage over time. Insurers factor this in when assessing structural risk.

Flooring: Timber/Laminate Timber flooring in an older home adds to the fire risk profile but is also a key indicator of the property's heritage character and replacement value. Ensuring your sum insured accurately reflects the cost to rebuild with comparable materials is important.

Solar panels The presence of solar panels on the roof is worth noting. Most home insurance policies will cover rooftop solar as part of the building, but it's always worth confirming this with your insurer — particularly for an older home where the roof structure may have needed reinforcement to support the panels.

No pool, no ducted climate control These omissions simplify the risk profile and help keep the premium lean. Pools and ducted HVAC systems both add complexity and replacement cost to a property.

---

Tips for Homeowners in Chudleigh

1. Review your sum insured regularly With a building sum insured of $400,000 for a 130 sqm heritage weatherboard home, it's worth checking whether this figure reflects current rebuild costs. Construction costs have risen sharply in recent years, and heritage properties often cost significantly more per square metre to rebuild than modern homes. Being underinsured can leave you seriously out of pocket after a major claim.

2. Understand your excess trade-off The $2,000 building excess on this policy is on the higher side. While it's helped reduce the annual premium, make sure you're comfortable covering that amount out of pocket if you need to make a claim. If your savings buffer is limited, it may be worth comparing policies with a lower excess — even if the annual cost is slightly higher.

3. Protect your home against bushfire and ember attack Chudleigh and the broader Meander Valley region can be exposed to bushfire risk during dry Tasmanian summers. Simple steps like clearing gutters, maintaining a defensible space around the home, and using ember-resistant mesh on vents can reduce both your risk and potentially your premium over time.

4. Check your contents cover is adequate At $20,000, the contents sum insured is relatively modest. Take a moment to walk through your home and tally up the replacement value of your furniture, appliances, clothing, and valuables. Many homeowners are surprised to find their contents are worth considerably more than their current cover suggests.

---

Compare Your Own Quote

Whether you're a long-time Chudleigh local or considering a move to this part of Tasmania, it pays to shop around. The quote featured here is a great example of what's possible when you compare multiple insurers side by side. Get a home insurance quote at CoverClub and see how your premium stacks up against the suburb, state, and national benchmarks — it only takes a few minutes and could save you hundreds of dollars a year.