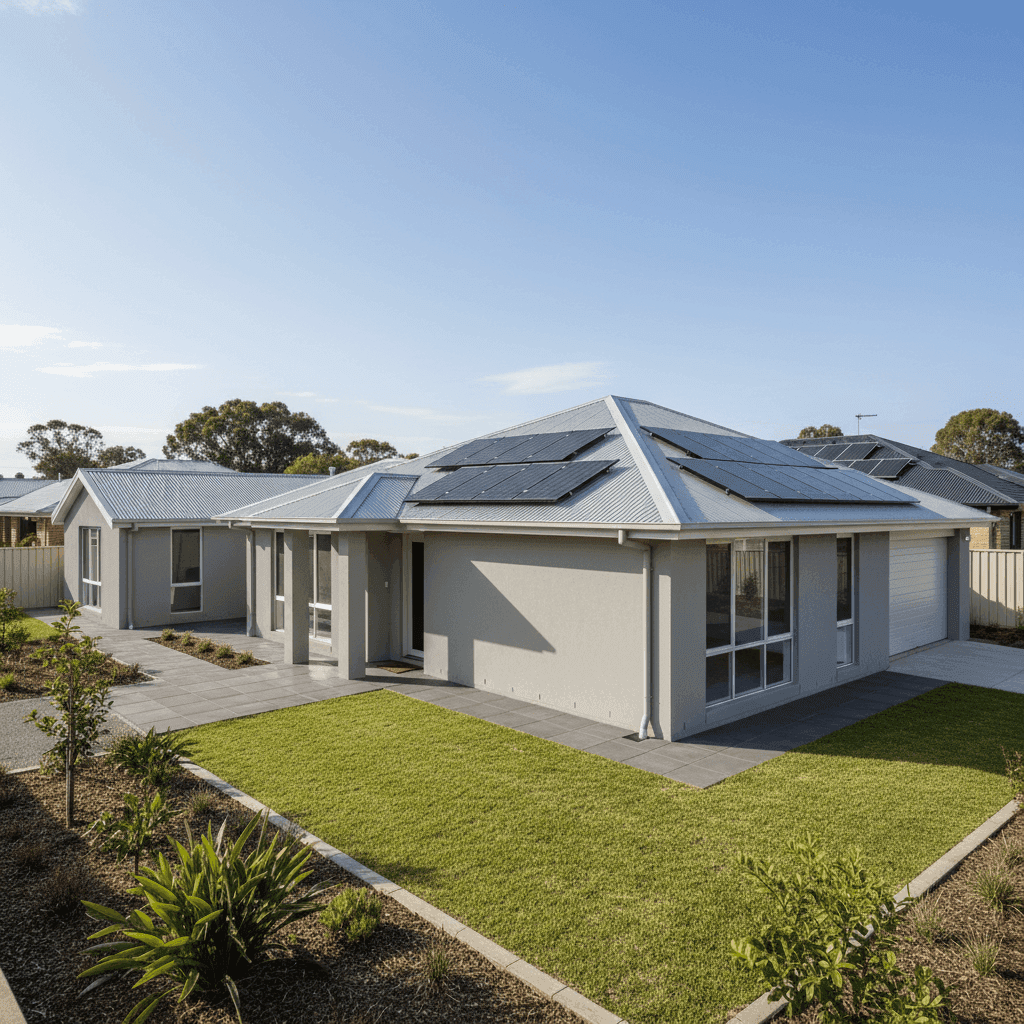

If you own a free standing home in Claymore, NSW 2559, you've probably noticed that home insurance premiums can vary wildly depending on who you ask. This article breaks down a real building insurance quote for a large, modern five-bedroom home in the suburb — and helps you understand whether the price stacks up against what others in the area, across New South Wales, and nationally are paying.

---

Is This Quote Fair?

The quote in question comes in at $2,372 per year (or $227/month) for building-only cover on a five-bedroom, four-bathroom free standing home, with a sum insured of $1,000,000 and a $1,000 building excess.

Our price rating for this quote is Expensive — Above Average.

To put that in perspective, the suburb average for Claymore sits at just $1,165/year, with a median of $1,175/year. That means this quote is more than double what most Claymore homeowners are paying for building cover. Even the 75th percentile — the top quarter of premiums in the suburb — only reaches $1,351/year, still well below this figure.

So what's driving the price up? The answer lies largely in the property itself. This is a brand-new (2025-built), large-format home with premium features — and insurers price accordingly. That said, it's worth shopping around, because the gap between this quote and the suburb benchmark is significant enough to warrant comparison.

---

How Claymore Compares

Understanding where Claymore sits in the broader insurance landscape is useful context for any homeowner evaluating their options.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Claymore (suburb) | $1,165/yr | $1,175/yr |

| Campbelltown LGA | $1,893/yr | — |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

(Based on CoverClub quote data. Suburb sample size: 5 quotes.)

A few things stand out here. First, Claymore is actually a very affordable suburb by both state and national standards. The NSW state average of $9,528/year is heavily skewed by high-risk coastal and flood-prone areas — the median of $3,770/year is a more realistic benchmark for typical NSW homeowners. Even so, Claymore's median of $1,175/year sits well below that figure, suggesting the suburb carries relatively low risk in the eyes of insurers.

Compared to the national median of $2,764/year, Claymore homeowners are generally getting a good deal — which makes this particular quote stand out even more. At $2,372/year, it's approaching the national median despite being located in an otherwise affordable suburb.

It's worth noting that the Campbelltown LGA average of $1,893/year is closer to this quote's ballpark, suggesting that larger or higher-value homes in the area do attract higher premiums — but there's still a meaningful gap to bridge.

---

Property Features That Affect Your Premium

Several characteristics of this property help explain why the quote lands where it does.

Size and specification: A five-bedroom, four-bathroom home is a substantial dwelling. With a $1,000,000 sum insured, the rebuild cost alone signals to insurers that this is a high-value asset. Larger homes simply cost more to insure — more square metres, more fixtures, more risk exposure.

Brand-new construction (2025): Newly built homes can cut both ways on premiums. On one hand, modern construction meets current building codes, which can reduce risk. On the other, a new home typically carries a higher replacement value, which pushes the sum insured — and therefore the premium — upward.

Hebel external walls: Hebel (autoclaved aerated concrete) panels are increasingly popular in new builds for their thermal efficiency and fire resistance. Insurers generally view Hebel favourably, as it performs well in fire scenarios — though it can be more expensive to repair or replace than traditional brick, which may temper any discount.

Steel/Colorbond roof: Colorbond roofing is a durable, low-maintenance option that insurers tend to rate well. It's resistant to fire, wind, and corrosion, which can positively influence your premium compared to, say, terracotta tiles.

Slab foundation: Concrete slab construction is standard in modern NSW homes and is generally considered a stable, low-risk foundation type.

Solar panels: Solar systems add value to the property and can increase the sum insured needed to cover them adequately. Depending on the policy, solar panels may or may not be included under standard building cover — always check the Product Disclosure Statement (PDS).

Ducted climate control: Ducted air conditioning is a significant fixed asset that forms part of the building's value. It contributes to the overall rebuild cost and is typically covered under building insurance.

Granny flat: The presence of a secondary dwelling on the property is a meaningful factor. A granny flat adds to the total insurable value and increases the complexity of the risk — more structures, more potential claims exposure.

No pool, no cyclone risk zone: The absence of a swimming pool removes one common source of liability claims, and Claymore's location outside designated cyclone risk areas keeps wind-related loading off the premium.

---

Tips for Homeowners in Claymore

1. Compare multiple quotes before renewing The gap between this quote and the suburb average is a reminder that insurers assess risk very differently. Using a comparison platform like CoverClub lets you see a range of quotes side by side, so you're not leaving money on the table at renewal time.

2. Review your sum insured carefully A $1,000,000 sum insured is substantial. Make sure it reflects the actual cost to rebuild your home — not its market value. Overinsuring means you're paying more in premiums than necessary; underinsuring can leave you exposed at claim time. Tools like the Cordell Sum Sure calculator (available through many insurers) can help you arrive at a realistic figure.

3. Check what's covered under building vs. contents With solar panels, ducted air conditioning, and a granny flat, it's important to confirm exactly what falls under your building policy. Some insurers treat solar systems as contents, others as building fixtures. Getting clarity upfront avoids nasty surprises at claim time.

4. Ask about discounts for security and safety features New homes often come with modern security systems, smoke alarms, and quality deadbolts — all of which some insurers reward with premium discounts. It's always worth asking your insurer what safety features they factor into their pricing.

---

Ready to Find a Better Deal?

Whether this quote is the right fit or you're just starting your search, comparing your options is the smartest move you can make. CoverClub makes it easy to see what home insurance actually costs for properties like yours in Claymore and across NSW — with real data, not estimates.

Get a quote and compare today at CoverClub →

You can also explore Claymore suburb insurance stats, NSW state benchmarks, and national averages to arm yourself with the knowledge you need before you commit to a policy.