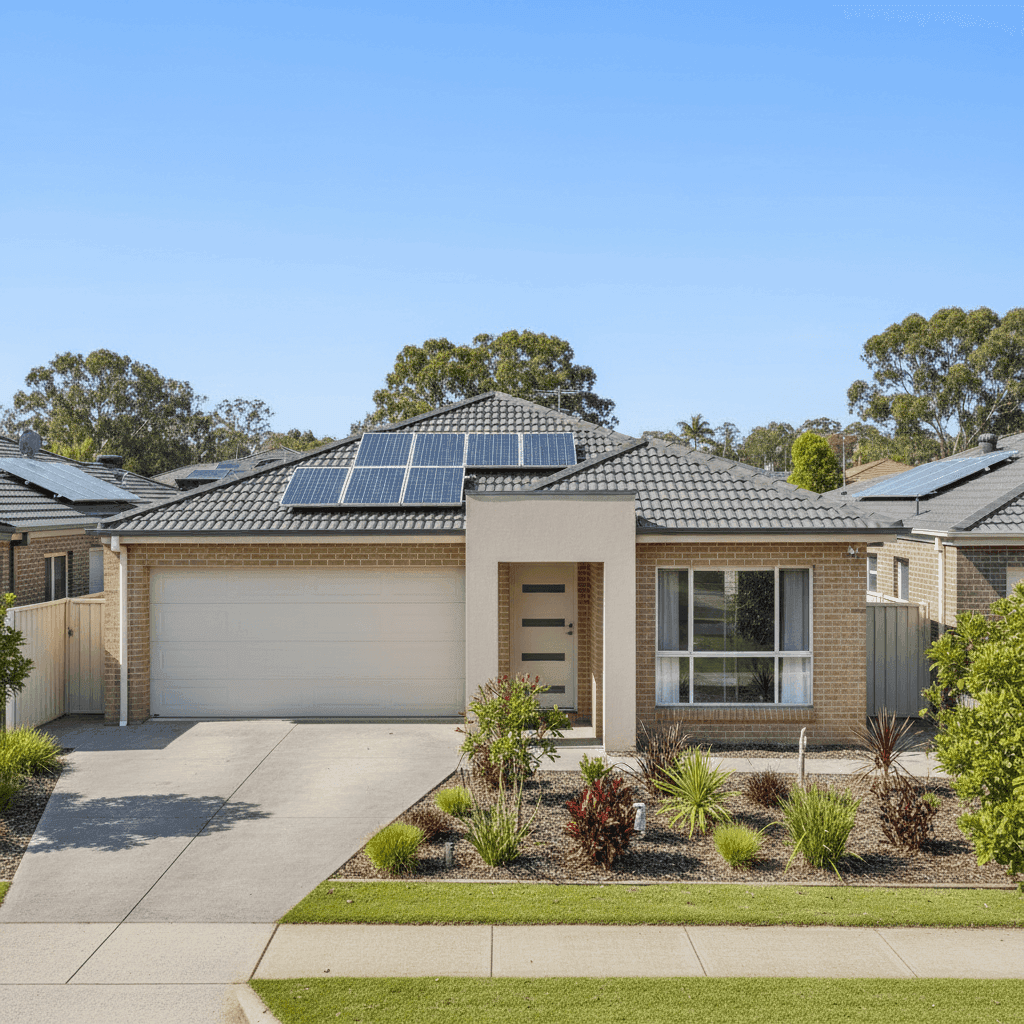

Cleveland, in Queensland's Redland City, is a well-established bayside suburb that combines coastal lifestyle with suburban convenience. For owners of a four-bedroom, free-standing home in postcode 4163, understanding what you should be paying for home and contents insurance — and why — can make a real difference to your household budget. This article breaks down a recent quote of $1,717 per year (or $165 per month) for a brick veneer home in Cleveland, putting it under the microscope against local, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: yes — and then some. This quote has been rated CHEAP, meaning it sits well below the average for the area. At $1,717 annually, it falls significantly under the Cleveland suburb average of $4,686 per year and even well below the suburb's 25th percentile of $2,383 per year. In plain terms, this premium is cheaper than at least 75% of comparable quotes gathered in the same postcode.

For a policy covering $400,000 in building sum insured and $40,000 in contents, with a $1,000 excess on both building and contents, this represents strong value. The coverage amounts are meaningful — $400,000 for the building alone is a realistic figure for a 214 sqm home built in 2006 — and the premium reflects a well-priced policy rather than one that's skimped on cover.

It's worth noting that "cheap" doesn't mean inadequate. The key is ensuring the sum insured genuinely reflects the cost to rebuild your home from scratch, including demolition, materials, and labour at today's prices. At $400,000 for a 214 sqm property, that works out to roughly $1,869 per square metre — a reasonable benchmark for a standard-quality brick veneer build in South East Queensland.

---

How Cleveland Compares

To put this quote in proper context, here's how Cleveland's insurance market stacks up against broader benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $1,717/yr |

| Cleveland Suburb Average | $4,686/yr |

| Cleveland Suburb Median | $3,540/yr |

| Cleveland 25th Percentile | $2,383/yr |

| Redland LGA Average | $3,178/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

(Based on 60 quotes collected for postcode 4163. [View full Cleveland suburb stats](https://coverclub.com.au/stats/QLD/4163/cleveland).)

A few things stand out here. Queensland's state average of $9,129 is extraordinarily high — more than 70% above the national average of $5,347. This is largely driven by North Queensland postcodes with severe cyclone exposure, which skew the state-wide figures dramatically. Explore QLD insurance data to see how dramatically premiums vary across the state.

Cleveland itself sits in a more favourable position. As a non-cyclone-rated area in South East Queensland, it avoids the extreme premiums seen in Cairns or Townsville. The suburb median of $3,540 is still above the national median of $2,764, reflecting Queensland's generally elevated flood and storm risk — but it's far more manageable than the state average might suggest.

This quote, at $1,717, comfortably undercuts every single benchmark in the table above.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour when it comes to pricing:

Brick Veneer Construction Brick veneer is widely regarded by insurers as a lower-risk wall type compared to timber or lightweight cladding. It offers solid fire resistance and structural durability, which typically translates to more competitive premiums.

Tiled Roof Concrete or terracotta tiles are considered a robust roofing material in insurance terms. They perform well in hail events and have a long lifespan, reducing the likelihood of weather-related claims compared to older Colourbond or asbestos-era roofing.

Slab Foundation A concrete slab foundation is generally viewed favourably by underwriters. It offers stability and is less susceptible to termite damage or subsidence compared to older stumped or pier-and-beam foundations common in pre-1980s Queensland homes.

Built in 2006 A construction year of 2006 means this home was built to modern building codes, including improved cyclone and storm standards introduced in Queensland following the 1990s and early 2000s reviews. Newer builds tend to attract lower premiums than ageing stock.

Solar Panels Solar panels do add a modest element of risk — they can be damaged by hail or severe storms — but most insurers now include them as standard under building cover. It's worth confirming with your insurer that the panels and inverter are explicitly covered under your policy.

Ducted Climate Control Ducted air conditioning systems are a fixed installation and typically covered under building insurance. Their inclusion in the sum insured is important; if the system needs replacing after a covered event, you want to know it's factored into your $400,000 building cover.

No Pool The absence of a pool removes a common source of liability exposure and maintenance-related claims, which can quietly push premiums upward for properties that have one.

---

Tips for Homeowners in Cleveland

1. Review your sum insured annually Building costs in South East Queensland have risen sharply since 2020. A sum insured that was accurate two years ago may now fall short of actual rebuild costs. Use a quantity surveyor estimate or your insurer's rebuild calculator to sense-check your $400,000 figure each renewal.

2. Confirm solar panel coverage explicitly Ask your insurer in writing whether your solar panels, inverter, and mounting hardware are covered under the building policy — and up to what value. Some policies cap solar cover or treat it as an optional endorsement.

3. Don't assume flood cover is included Cleveland's bayside location and proximity to Moreton Bay means some areas can be affected by storm surge or heavy rainfall events. Check whether your policy includes flood cover (defined as inundation from a natural watercourse) as distinct from storm damage. These are separate perils under many Australian policies.

4. Compare at renewal, not just at purchase The insurance market shifts every year. A premium that was competitive when you first took out your policy may not be the best available at renewal. Shopping around — particularly through a comparison platform — takes minutes and can save hundreds of dollars annually.

---

Compare Your Own Quote

Whether you're a Cleveland local or looking at a property in the area, it pays to see what the market is offering before you commit. CoverClub makes it easy to compare home and contents insurance quotes from multiple insurers in one place. Get a quote now and find out whether your current premium is as competitive as this one — or whether there's room to do better.